Despite posting higher losses that grew by over five-fold year-over-year in the first quarter, Tilray’s (NASDAQ:TLRY) stock is still attracting buyers. If the cannabis supplier’s revenue is growing rapidly but it’s losing more money, why should any investor own TLRY stock?

Tilray’s Q1 Losses Didn’t Stop Its Stock

Tilray lost $4.1 million in Q1 despite its annualized cost savings of around $40 million. Brendan Kennedy, Tilray’s CEO, said that “while the positive impact of these actions are not fully reflected in this quarter’s results, they will become more clearly evident over the course of this year.”

Though Tilray’s cannabis sales grew 126.2% to $52.1 million, not all of its businesses expanded. For example, its bulk sales fell, although the drop was offset by the inclusion of Manitoba Harvest, a company that Tilray had previously acquired.

The company’s total cannabis kilogram equivalents sold rose by 92.4% YOY to 5,794 kilograms. But its average cannabis net selling price per gram fell from $5.60 last year to $5.28. The latter decline was due to unfavorable product shifts.

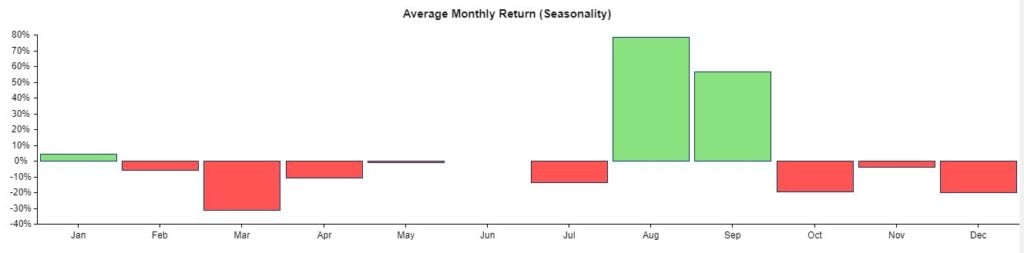

As you can see from the chart below, the company’s seasonal strength begins in August:

The company’s gross margin fell two percentage points to 21% due to inventory valuation adjustments. Looking ahead, lower inventories that are better aligned with demand should boost its margins in future quarters.

Tilray attributed its $1.73 per share loss to a change in the fair value of its warrants held by investors.

Bright Spots

The 23% YOY growth of Tilray’s recreational sales was a positive development. Its CEO, Kennedy, said that the growth of its flower revenue was the main reason that its overall sales increased. Edibles and vapes also helped its results.

COVID-19 had minimal impact on the company’s sales. In March, its sales increased slightly. And in April, its revenue was higher than in January and February.

Canada’s decision to double the number of stores that sell cannabis should boost Tilray’s sales. Last year, the slow pace of store openings in Canada hurt the overall cannabis market and probably gave the illicit market a competitive edge.

But as the country permits more legal stores to open, the demand shift away from the illegal market will benefit all cannabis suppliers.

The medical cannabis market is another potential bright spot for Tilray. Kennedy said on the conference call that “the next milestone that I’m paying attention to is at some point over the next three or four quarters our revenue internationally will exceed our revenue in Canada and that will be important milestone for us as a company.”

The Bottom Line on TLRY Stock

Most Wall Street analysts have a “hold” rating on Tilray, according to Tipranks. So, until an acceleration of the company’s revenue offsets its losses, few analysts will be upbeat about TLRY stock. The shares’ fair value (based on its enterprise value / sales ratio) is around $10, according to Stock Rover.

Investors have plenty of beaten up cannabis stocks to choose from. The list includes Aurora Cannabis (NYSE:ACB), Cronos Group (NASDAQ:CRON), and Canopy Growth (NYSE:CGC). All of those stocks are speculative investments.

But Canopy and Cronos have big backers that will minimize their solvency risks. Tilray is one of the smaller players by market capitalization and revenue. Plus, unless it carefully manage its cash levels, it will have to sell more stock, diluting its shareholders and hurting its share price.

Investors have better choices than TLRY stock. If its cannabis sales continue to rebound while weaker firms exit the market, investors may consider obtaining a small position in Tilray.