Canada updated its quarterly sales numbers for the nationwide cannabis industry on Sep. 4. During the second quarter, which lasted from April to June, household spending on unlicensed cannabis totaled 785 million Canadian dollars and was down 4.7% from the previous quarter. This number has declined in every period since the recreational market opened in Canada on October 17, 2018. In the legal market, CA$648 million was spent on recreational pot and CA$155 million was spent on medicinal marijuana, combining for a total of CA$803 million.

At first glance, this sounds huge for Canadian cannabis companies. It's the first time the legal marijuana market has come out ahead of the illicit market in terms of sales. But the win is coming at a cost: Much lower margins. Here's a look at why, despite a shrinking black market for marijuana, things may not get better for Canadian pot stocks.

Companies Are Focusing On Value brands

The legal market's win in Q2 is proof that Canadian cannabis companies' focus --lowering prices for consumers -- is working. Original Stash is a value brand that pot producer HEXO (NYSE: HEXO) launched last October, specifically targeting the black market and boosting licit sales by offering goods at prices as low as CA$4.49 per gram, including tax. In January, Statistics Canada estimated the average price of illegal cannabis to be CA$5.73 per gram.

In HEXO's most recent quarterly results, released on June 11 for the period ended April 30, its gross revenue of CA$30.9 million was nearly double the CA$15.9 million it brought in during the same period last year. But despite the significant increase in revenue, HEXO only generated an extra CA$2.4 million in gross margin (before adjustments for fair value). After subtracting excise taxes and costs of goods sold, just 28.5% of the top line remained, compared to 40.3% a year ago.

Excise taxes are relevant here, since the calculation assumes a flat-rate duty -- so a low-priced product could generate a higher excise cost per gram. Unsurprisingly, HEXO noted that the key driver in the company's increase in sales for the quarter was its value brand, Original Stash.

Investors saw similar trends when rival Aurora Cannabis (NYSE: ACB) released its most recent results. On May 14, the company released its third-quarter report for the period ended March 31, in which its gross sales rose by 19% year over year. And once again, by the time that revenue got to the gross profit line before fair value adjustments, there was a story to tell. The company's gross margin of CA$31.9 million declined by 12% from the prior-year period. Aurora Cannabis credits "a significant shift in our product mix toward our new Daily Special value brand" as a key driver of strong quarterly numbers.

In Q3, the company said that excise taxes negatively impacted Aurora's gross margin by 5%. A year earlier, the percentage was just 4%. The average net selling price of consumer cannabis in Q3 was just CA$4.33, down 21% from CA$5.48 a year ago.

Why This Could Hurt Pot Stock Pickers

Lower prices and slimmer margins are going to make it challenging for cannabis companies to reach their profitability goals. In a June 23 update, Aurora Cannabis said that it was still on track for its goal of reaching positive adjusted earnings before interest, taxes, depreciation, and amortization (EBITDA) number by the first quarter of fiscal 2021.

But that's an ambitious target given that in Q3 that number was a negative CA$50.9 million. A year earlier, the company was actually closer to breakeven with an adjusted EBITDA loss of CA$36.6 million. If the company continues to push its value brand, then margins may continue to erode, meaning it'll take even more revenue to breakeven. If that sales growth can't keep up with shrinking margins, investors can expect share prices to nosedive.

Key Takeaways For Investors

Hitting this milestone was important for the Canadian cannabis industry in order to show that it can compete with the illicit market. But for this pattern to continue, companies like Aurora and HEXO will need to continue being as competitive as the black market, or even more so, in order to retain market share. But lower prices may be doing more harm than good, especially if it reduces profits and cash flow -- two traits investors will undoubtedly look for.

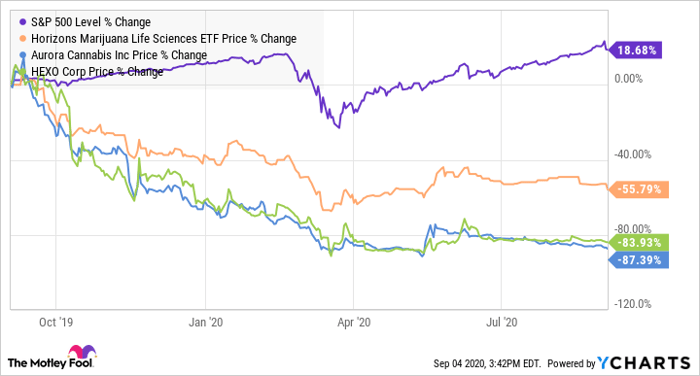

In February, Ello Capital speculated that Aurora had just a few months of liquidity left. That definitely didn't help its stock, and over the past year both Aurora and HEXO shareholders have suffered significant losses:

It's going to take more than just sales growth to win investors back, especially if higher revenue numbers don't lead to a stronger bottom line. That's why, although hitting the milestone was great for the Canadian cannabis industry, it may not be a good sign for pot stocks in Canada overall. If selling prices continue to drop, this could be one crowded race to the bottom.