Dividend Kings was founded under the principles of quality first, valuation second and proper risk management always. That includes avoiding dangerous bubbles as MLPs were in back in 2015, and from which one of the most epic industry bear markets commenced.

Mind you, quality MLPs like Enterprise Products Partners (EPD), Energy Transfer (ET) and MPLX (MPLX), have all made their unitholders money over the last seven years. The same can't be said of MLPs in general, which is why Dividend Kings only recommends 18 safe midstream corporations/MLPs to our members.

EPD, MPLX, and ET are among those 18, and Dividend Kings' owns all of them across our four model portfolios, High-Yield Blue Chip, Deep Value Blue Chip, Fortress and $1 Million Retirement.

What explains the recent freakish crash in MLPs? Well, Dividend Kings members know that over the long-term only fundamentals such as dividends, earnings and cash flow determine stock prices.

One of Seeking Alpha's leading MLP experts, Hinds Howard, recently explained the reason for the current MLP crash.

It was another week when it felt like midstream can only capture downside in the market. Oil prices up, stock market up on less concerns of global growth, but midstream sells off, because reasons that change from week to week... This was the 7th negative week for the MLP Index IN A ROW, which only happened one other time in 24 years (March/April 2012 was the last time). Also, this will be 14th negative week of last 17, just three positive weeks in four months! Never before have MLPs been negative 14 of 17 weeks... this prolonged and ongoing midstream weakness is due to a brutal combination of technical and fundamental forces. Technical headwinds (as discussed here ad nauseam) from big slow institutional capital exiting MLPs while retail investors are throwing in the towel and selling to lock in tax losses after one more distribution payment. Fundamental headwinds from (investor-imposed) producer discipline driving down outlooks for those less diverse and more upstream-oriented midstream operators." -Hind Howard (emphasis added)

But long-time readers and Dividend Kings members know that the best way to enjoy mouth-watering safe yields, as well as eye-popping short-term returns, is to "be greedy when others are fearful."

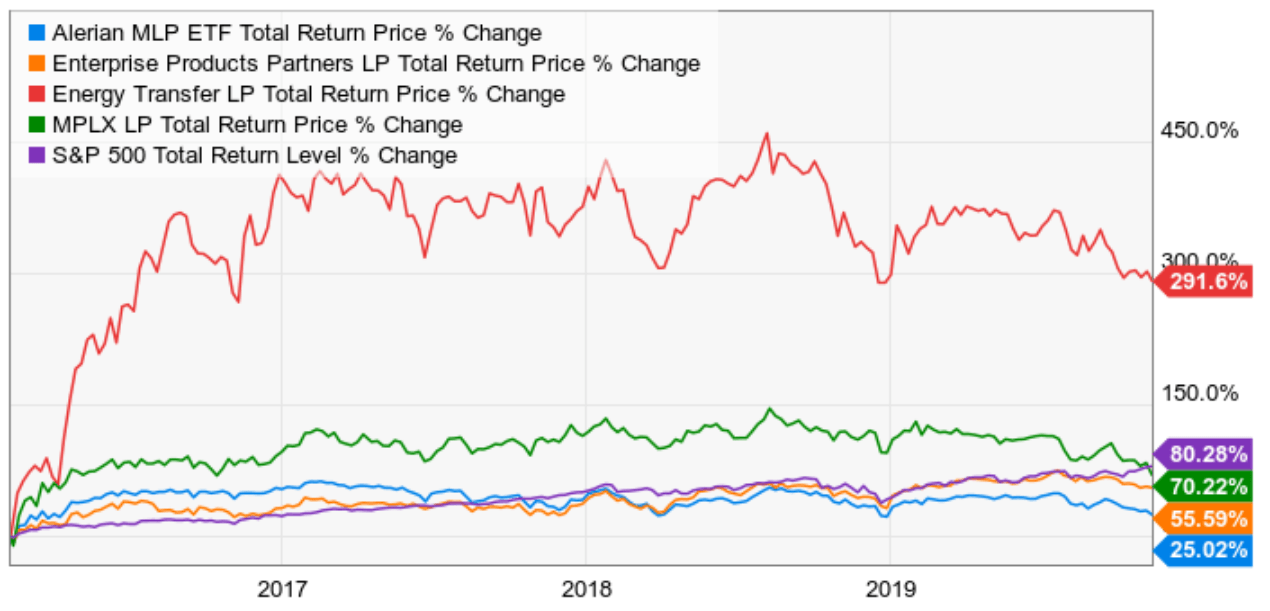

MLP Total Returns Since 2016 Oil Crash Lows

As Mr. Howard points out,

This week the MLP Index was down more than 1% each day for three straight days this week, which was the first time since January that has happened. It has only happened 18 other times in the last 10 years, 15 of those 18 times (or 83%), the AMZ was positive 30 days later. In those 15 times when AMZ was positive, the average return was 8.6%. Overall average return across all 18 times has been 6.6%. Based on that very small sample size, chances are MLPs trade better at some point in the next 30 days." - Hinds Howard (emphasis added)

Neither I nor Mr. Howard are market timers. We can't guarantee that MLPs won't keep crashing to even more absurd levels. What I can tell you is that Wall Street is dead wrong about quality MLPs like Enterprise, Energy Transfer and MPLX, which now represent once in a generation opportunities to lock in generous, safe and growing yield, as well as market-smashing future return potentials.

These three MLPs are 22% to 60% undervalued, yielding 6.7% to 11.3%, and can realistically deliver 20+% CAGR total returns over the next five years.

Why Wall Street Is Dead Wrong About Enterprise Products Partners

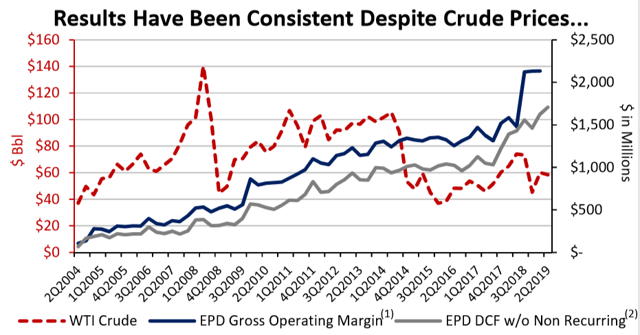

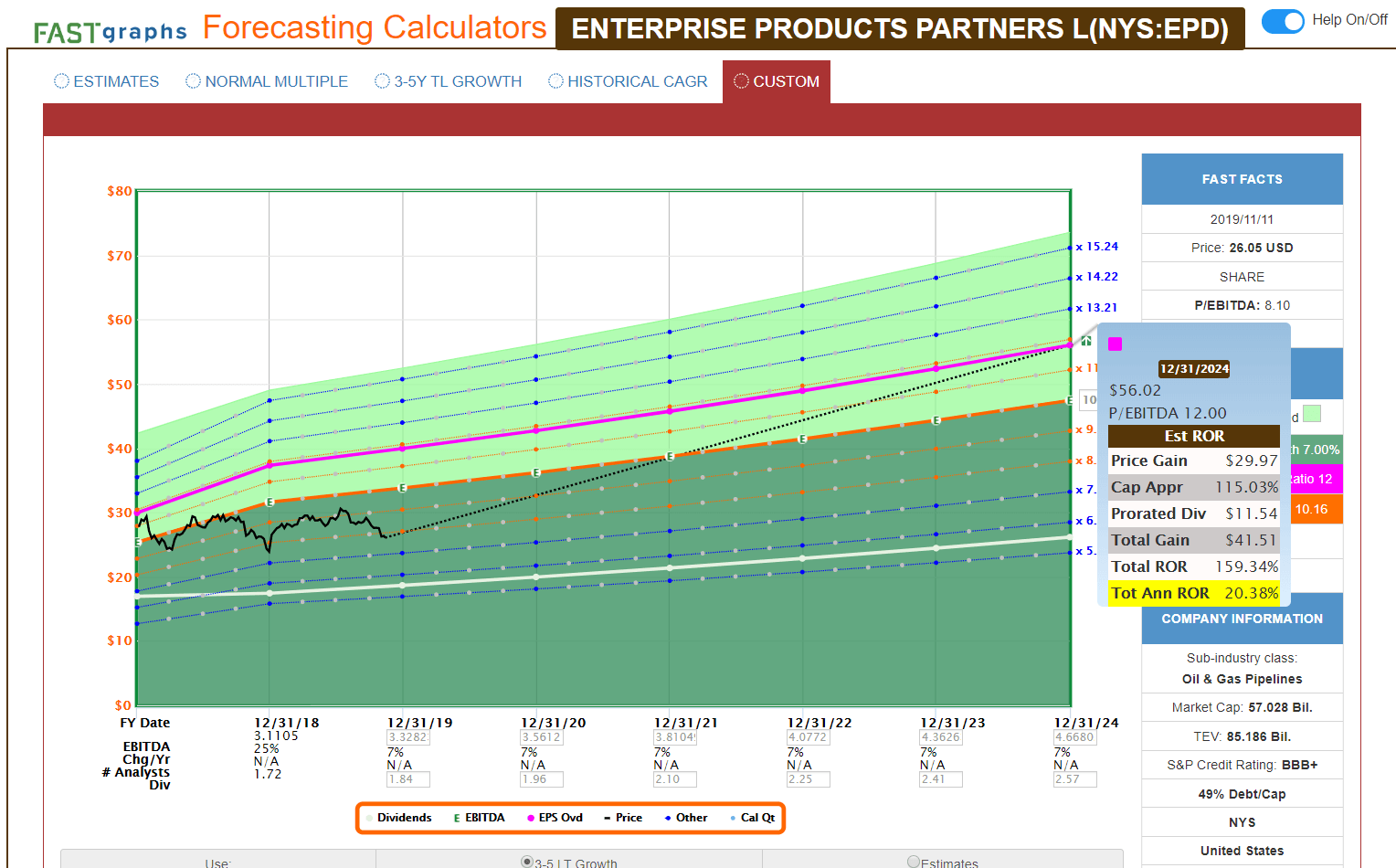

Enterprise is now trading at 7.2 times EBITDA/unit, the lowest valuation in 8 years. Only during the Financial Crisis did it trade at more attractive cash flow multiples, when credit markets were frozen and its yield peaked at 12.86%.

During the darkest days of the oil crash of 2014 to 2016, when crude bottomed at $26 (it's $57 today) EPD hit a peak yield of 6.6%. Today EPD is offering a very safe 6.7% yield and its distribution has literally never been safer.

One look at its latest earnings shows that the market's pessimism is 100% objectively wrong.

- adjusted EBITDA: +6.4% YOY

- distributable cash flow +4.7% YOY

- distribution coverage: 1.7 (1.2 or higher is safe for self-funding MLPs)

- debt/EBITDA: 3.3 (5.0 or less is safe according to credit rating agencies)

- interest coverage: 6.8 vs 2.5 safe limit for the industry

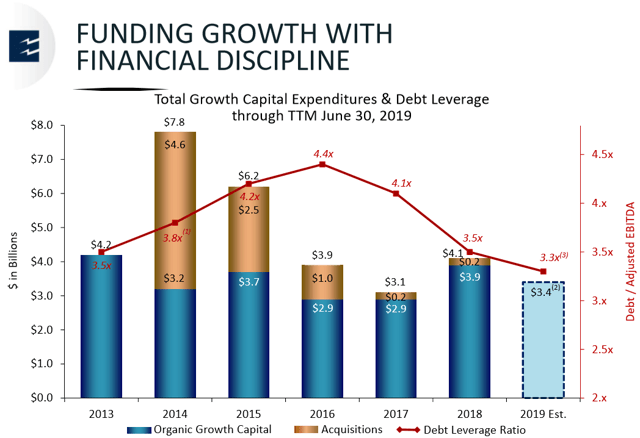

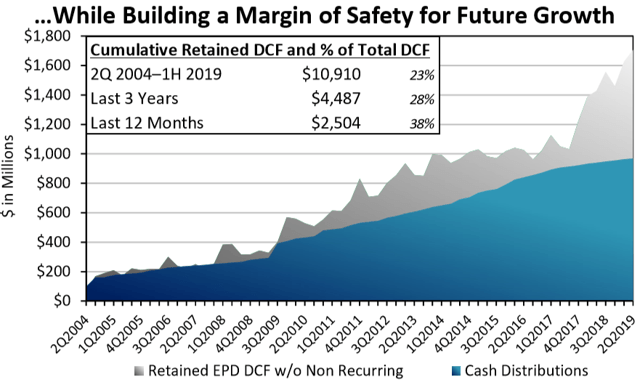

- annualized retained cash flow (DCF minus distributions): $2.8 billion

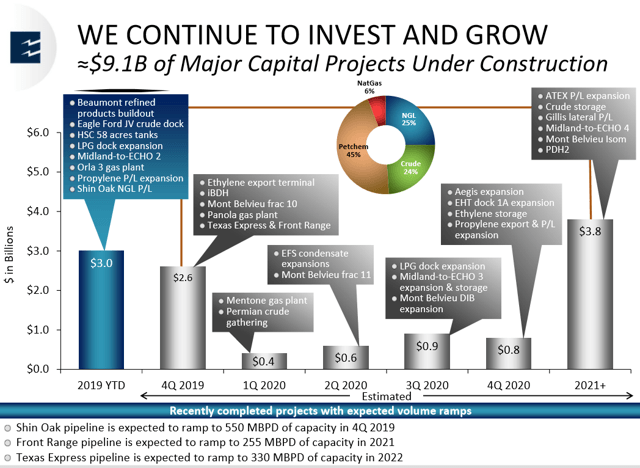

- growth projects added to the backlog in Q3 alone: $3.6 billion

- total growth backlog (through 2023): $9.1 billion

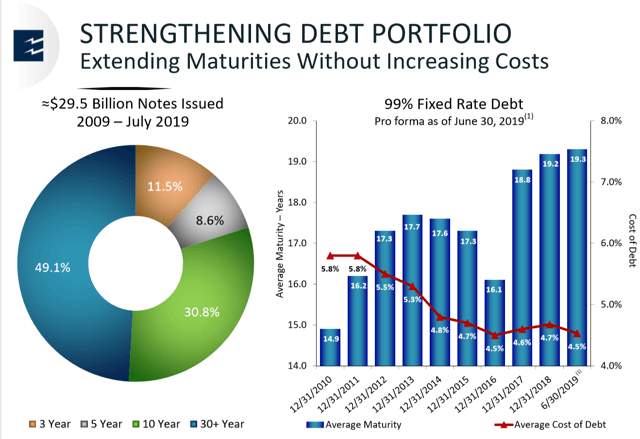

Enterprise has a BBB+ credit rating, tied for the strongest in the industry with other blue chips like TRP, ENB, and MMP.

99% of its debt is fixed-rate, with half of that being 30-year bonds. Its weighted duration on debt is a record high at 19.3 years, which is the longest of any midstream operator.

Even when the rest of the midstream industry was going nuts with leverage as high as eight or nine, EPD's conservative management team (hands down the best in the industry) kept leverage at safe levels, peaking at 4.4.

Similarly, Enterprise has always retained a lot of cash flow, even before the industry adopted self-funding as the low-risk gold standard.

EPD is now funding 80% of its growth with retained cash flow and the rest with some of the longest duration and lowest cost fixed-rate debt in the industry. It has $6.2 billion in liquidity, including $1.2 billion in unrestricted cash on the balance sheet.

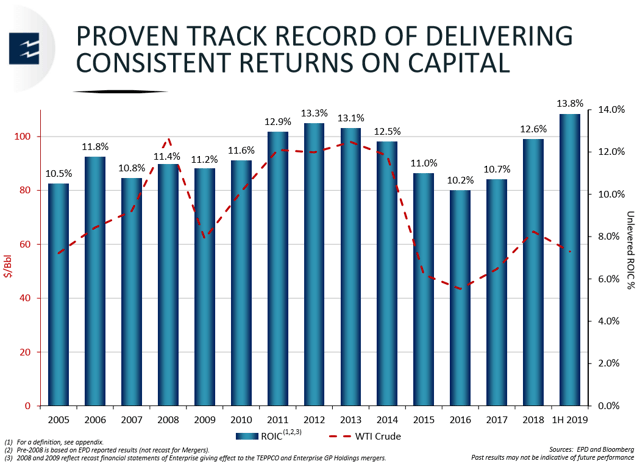

And bond investors trust this Super SWAN enough to recently lend it $2.5 billion in bonds at a weighted maturity of 20 years and an average interest rate of 3.6%. In other words, EPD's average borrowing costs are still falling, and its profitability on new investments is expected to average 13% over the next decade according to analysts like Morningstar's Stephen Ellis.

Over the past decade, EPD's returns on invested capital have averaged 12%, never falling lower than 10.2% even when the shale industry was facing its existential threat from $26 crude.

Management, led by industry legends CEO Jim Teague (over 40 years of experience), and Chairwomen Randa Duncan Williams (daughter of the MLP's founder) continues to find new lucrative investments to grow the MLP's long-term and super stable cash flow.

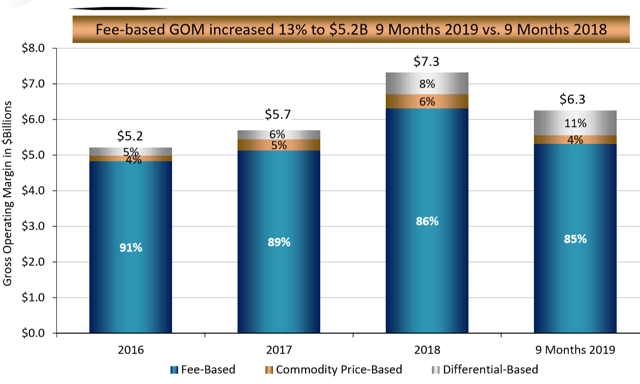

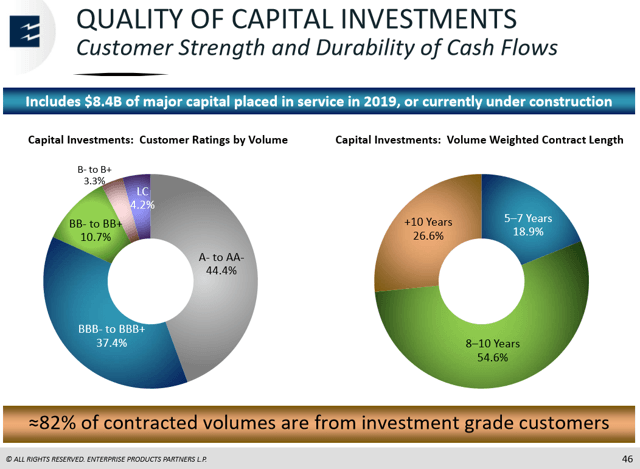

85% of EPD's cash flow is under long-term, fixed-rate and volume committed contracts. How strong are those counterparties?

82% of its hundreds of customers are investment grade and 44% are A-rated by S&P. The $3.6 billion in new projects it just commissioned, are similarly backed by 100% capacity contracts, with minimum volume commitments and weighted duration of 14 years.

Approximately, 77% of the contracted volumes associated with these projects under construction are with investment-grade customers and 70% of the volume-weighted contract links are 14 years or more." - CFO Randy Fowler, Q3 conference call

Thus its no surprise that EPD's distributable cash flow is recession-resistant and impervious to even a 77% decline in oil prices.

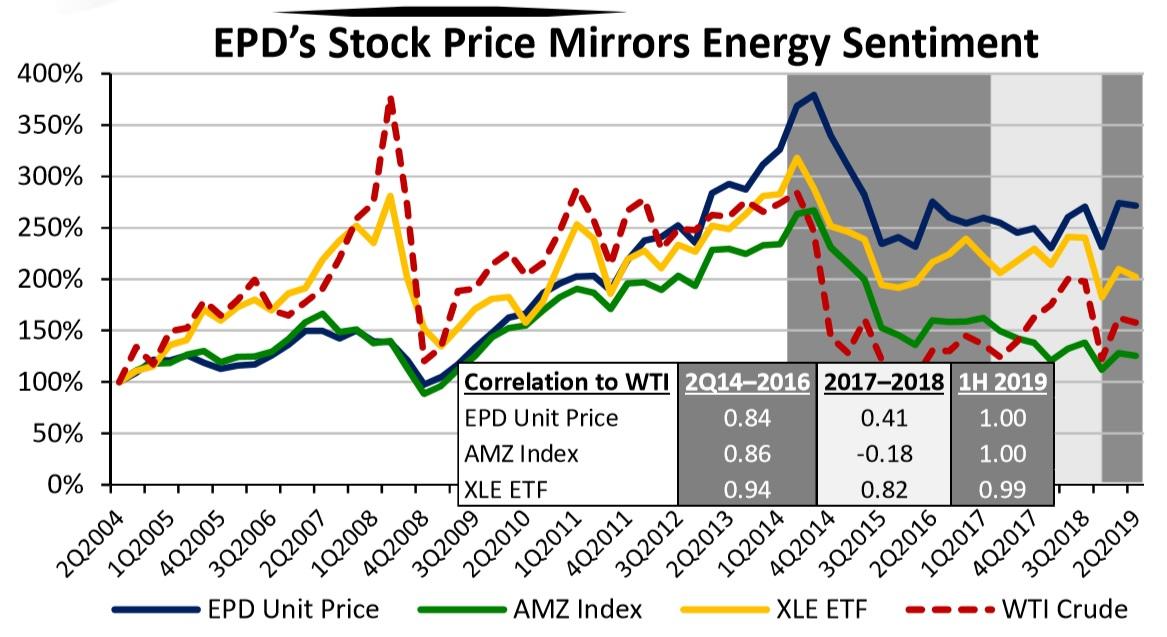

Does EPD's stock price track oil prices? Often it does. Does it's cash flow fluctuate as wildly? No, it does not.

Whenever stock prices become disconnected from fundamentals (cash flow and distributions) that is always an opportunity for smart and long-term bargain hunting.

Enterprise has raised its payout 71 times since its IPO including 61 consecutive quarterly hikes (15 straight years and counting). EPD has raised its payout to retail investors for 20 consecutive years, though its streak is actually 22 years, including before its IPO.

With our upcoming distribution payment in November, we began our 22nd year of consecutive distribution growth. We continue to get closer to the 25-year Dividend Aristocrat benchmark, which is a select group of stocks with over 25 years of consecutive dividend increases, sort of, the best of the best of dividend growth -- in best of the best of dividend growth stocks." - CEO Jim Teague

The market is partially upset with Enterprise because rather than buyback stock at 14% EBITDA yields (nearly as profitable as growth projects), management continues to add to its backlog.

But guess what? Enterprise has become a legend and generated 17% CAGR total returns for two decades, disproving the flawed concept that "MLPs are a broken business model" precisely because of management's long-term focus on growing its business.

Enterprise Products Partners Total Returns Since 1999

Even with its current bear market, which is 100% not supported by its objectively very strong fundamentals, EPD has been a great long-term investment. It's been less volatile than the broader market, delivered generous, very safe and steadily rising income, and nearly tripled the S&P 500's returns...for 20 years.

That's what Super SWANs tend to do, and why Dividend Kings owns Enterprise in three of our four model portfolios, all of which are beating their benchmarks since we launched 17 weeks ago.

But the real reason I wrote this article is to point out the true bargain Enterprise has become.

Enterprise is not just the quintessential Buffett "wonderful company at a fair price" it's now a wonderful company at a wonderful price.

Enterprise is not just the quintessential Buffett "wonderful company at a fair price" it's now a wonderful company at a wonderful price.

The way I value companies is not by guessing but by looking at the average multiples real investors have paid for dividends, earnings, and cash flow. I then apply the consensus estimates from FactSet (analyst consensus) to any given year's results to estimate fair value based on that metric.

The range of fair value estimates likely includes the intrinsic value of a stock and the average is my reasonable estimate for what its fundamentals are worth in any given year.

| Metric | Market-Determined Fair Value | 2019 Fair Value | 2020 Fair Value | 2021 Fair Value |

| 5-Year Average Yield | 6.06% | $29 | $30 | $31 |

| 13-Year Median Yield | 5.75% | $31 | $32 | $33 |

| 20-Year Average Yield | 6.46% | $27 | $28 | $29 |

| P/OCF | 11.3 | $34 | $37 | $39 |

| P/EBITDA Per Unit | 10.1 | $38 | $39 | $40 |

| P/EBIT | 14.4 | $41 | $42 | $44 |

| P to EV/EBITDA per unit | 10.1 | $38 | $39 | $40 |

| Average | $34 | $35 | $37 |

Enterprise is worth about $34 in 2019, $35 in 2020 and $37 in 2021. In other words that's the value of its cash flow and the distributions they are generating.

Today Enterprise is trading at $26.44, a 22%, 24%, and 29% discount to its 2019, 2020 and 2021 approximate fair values, respectively.

| Classification | Margin Of Safety Required For 11/11 Quality Super SWAN | 2019 Price | 2020 Price | 2021 Price |

| Reasonable Buy | 0% | $34 | $35 | $37 |

| Good Buy | 0% | $34 | $35 | $37 |

| Strong Buy | 10% | $31 | $32 | $33 |

| Very Strong Buy | 20% | $27 | $28 | $30 |

Reasonable buys are any quality company trading at fair value. For stronger conviction recommendations I use a margin of safety based on the quality of the firm and its risk profile.

EPD as the highest quality MLP in the world rarely trades at a 20% discount to fair value. Here's what that kind of margin of safety can buy patient long-term high-yield investors.

- FactSet long-term growth consensus: 4.0% CAGR

- Reuters' 5-year CAGR growth consensus: 10.9% CAGR (tad optimistic)

- Ycharts long-term growth consensus: 6.0% CAGR

- historical growth rate: 9.9% CAGR over 20 years

- realistic growth range: 3% to 7% CAGR

- historical fair value range: 9 to 12 times EBITDA

Enterprise's nearly $3 billion in annual retained cash flow means it could repurchase up to 5% of units per year, driving 5% annual cash flow/unit growth if it wanted to. That would also allow it to raise its payout by that amount if it ran out of profitable growth projects to build.

But let's see what happens if EPD grows 1% slower than any analyst consensus estimates.

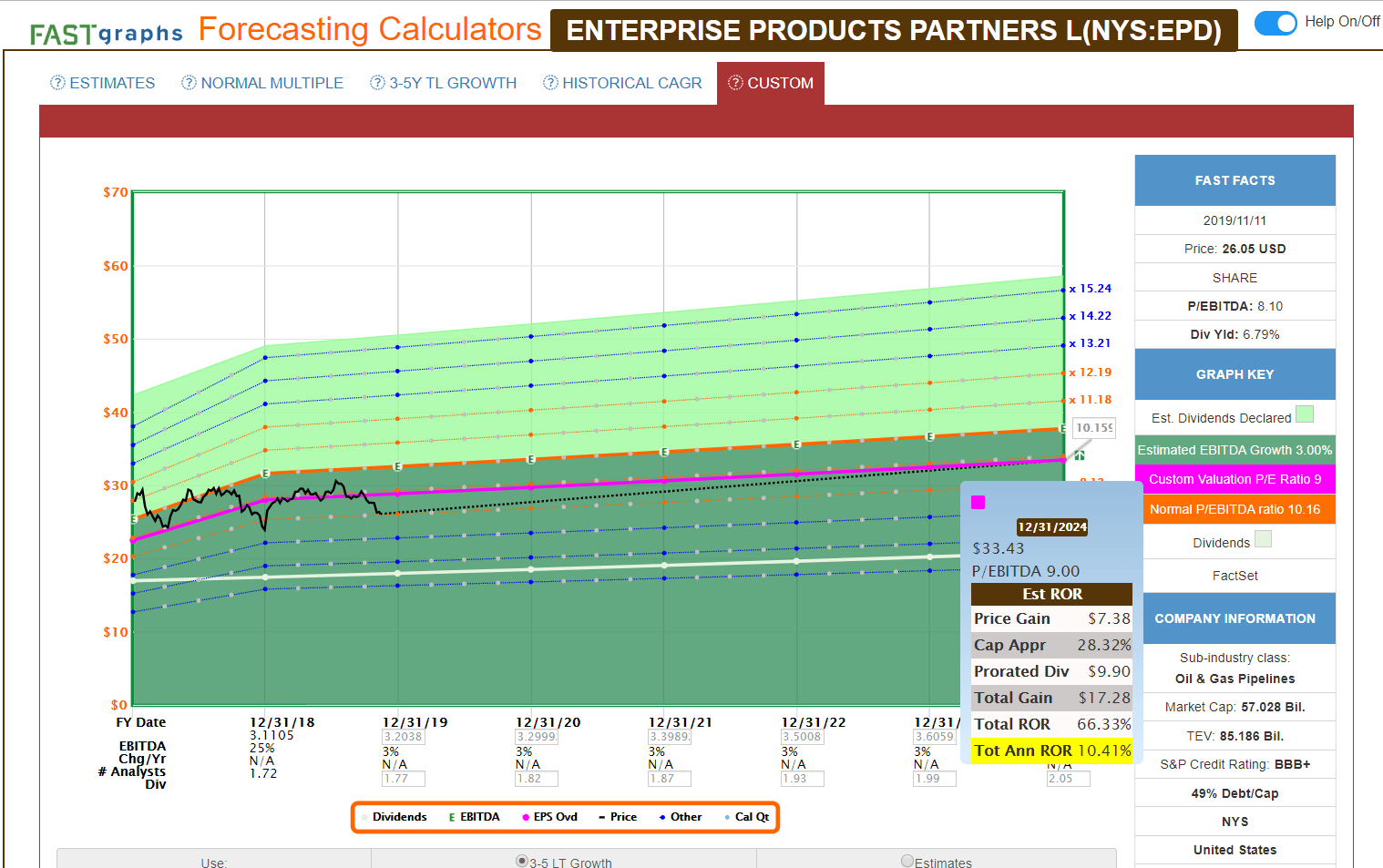

The Ben Graham fair value formula built into F.A.S.T Graphs estimates that EPD growing at 3% is worth 10.2 times EBITDA. Dividend Kings models just 9, since that is the low end of its own historical fair value range.

Yet thanks to a very safe 6.7% yield, EPD growing at a slow utility rate is still able to deliver double-digit total returns that will likely put the S&P 500 to shame over the coming seven to 15 years.

What if Enterprise grows slightly faster, as is our base case?

What if Enterprise grows slightly faster, as is our base case?

Using the 4% FactSet consensus forecast and the mid-range 10.5 historical P/EBITDA per unit multiple we see that EPD can realistically double your investment over the next five years.

The upper end of our total return range is created by Morningstar's bullish forecast for the MLP.

We expect EBITDA to increase about 7% annually over the next five years and distributions about 7% annually on average over the same time frame, though the growth is weighted more toward the tail end of our forecast period." - Morningstar's Stephen Ellis

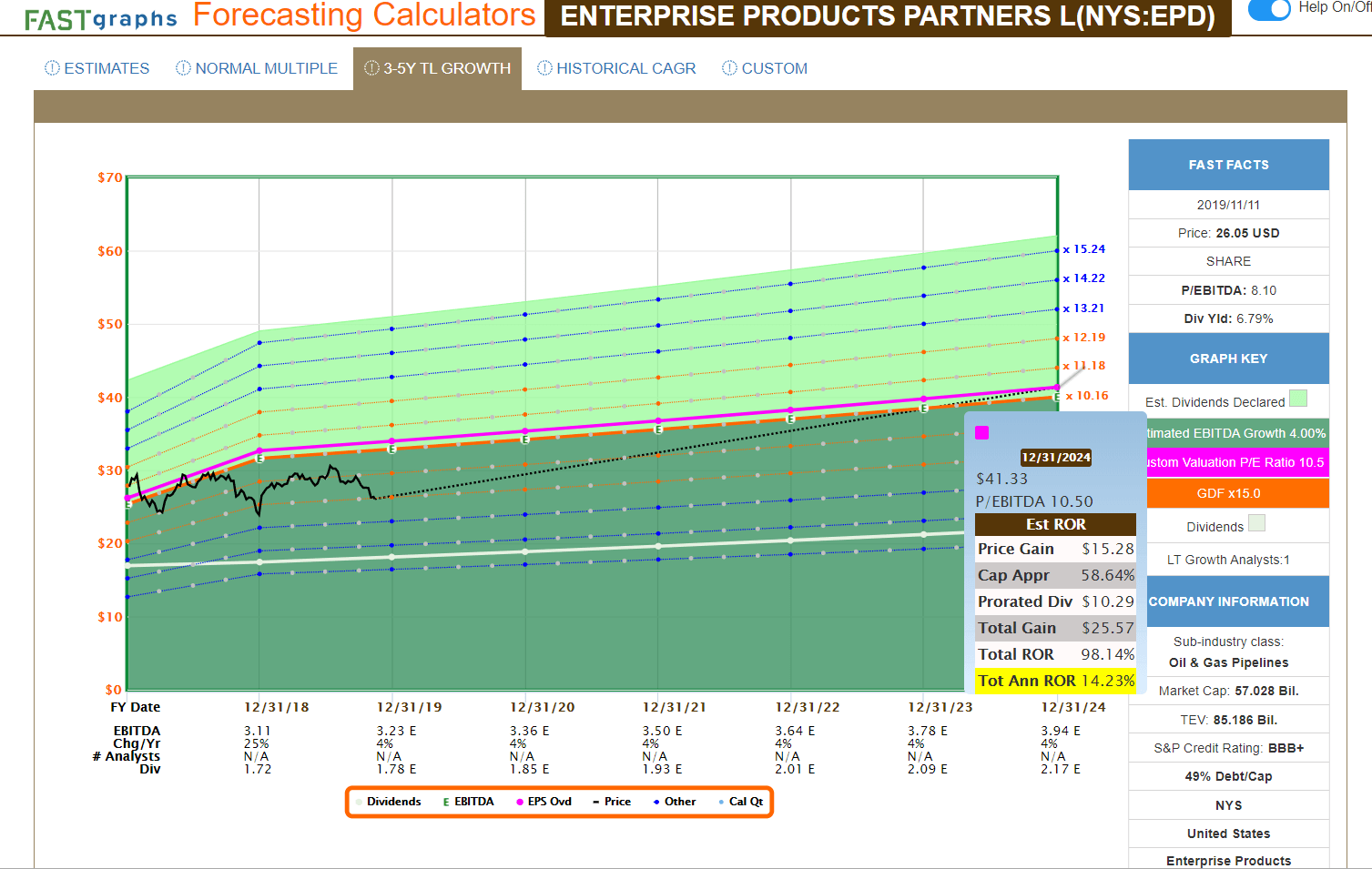

Morningstar's fair value estimate for EPD ($35.5) is based on a 13 times EBITDA multiple and Dividend Kings' only models as high as 12, the upper end of what investors have been willing to pay for it outside of periods of overvaluation.

Yet these reasonable estimates, which are far from outlandish, and well within management's ability to realistically deliver, shows that EPD could potentially deliver 20% CAGR total returns through 2024.

That's more than double the S&P 500's historical 9.1% CAGR total returns, and potentially as much as three to ten times what asset managers expect the broader market to deliver.

It's also in-line with EPD's historical returns over the last 20 years which is why today is literally the best time in eight years to buy a piece of this best in breed blue-chip MLP.

Why Wall Street Is Dead Wrong About Energy Transfer

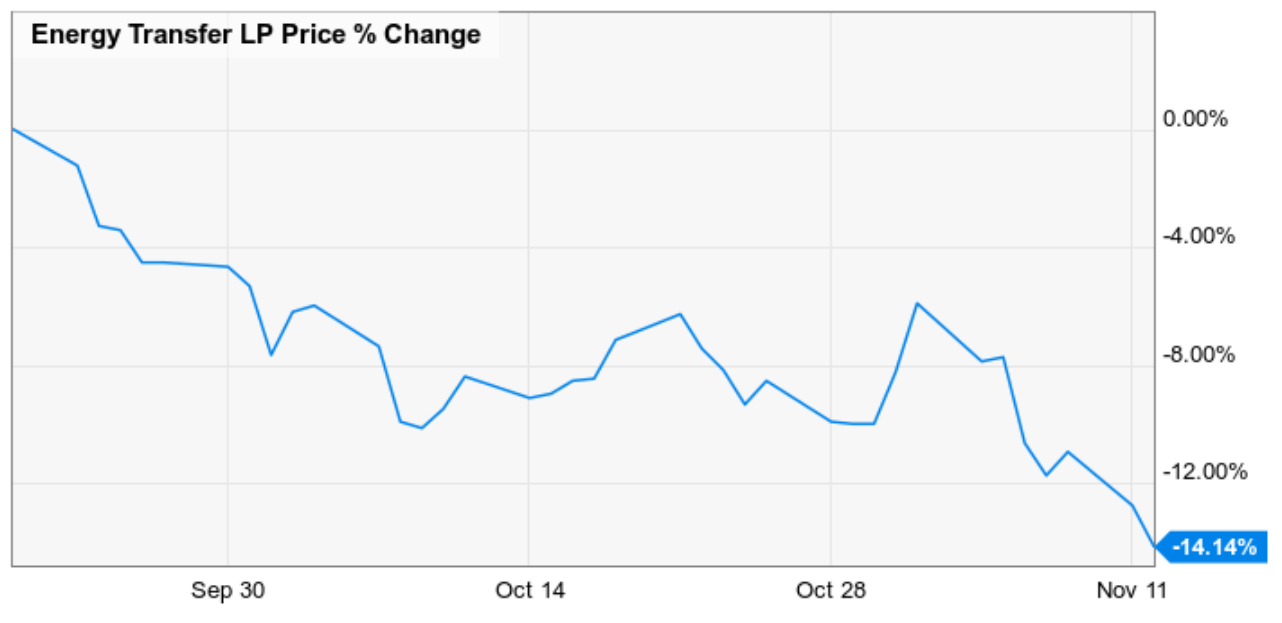

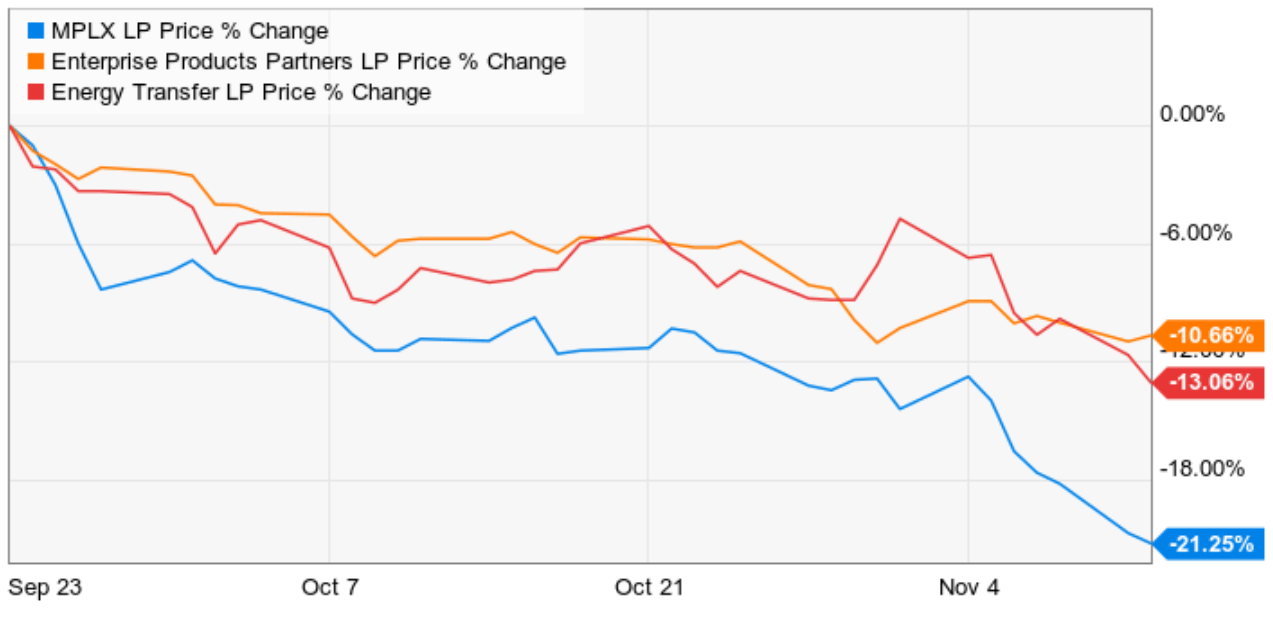

I've gotten a lot of questions about Energy Transfer, including why it's been so brutalized by the market over the past two months.

Rest assured it's not due to its strong fundamentals. Cash flow, which ultimately generates all intrinsic value and pays the mouth-watering and safe yield, has been rising steadily.

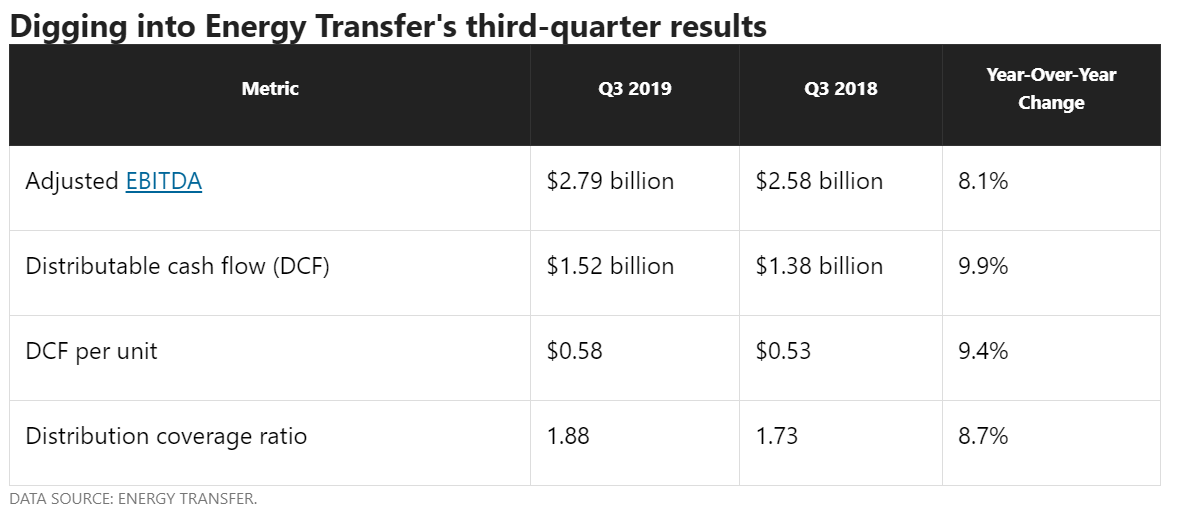

Coverage has been climbing, hitting 1.88 in Q3, and 1.98 YTD. Energy Transfer isn't just pursuing self-funding for its organic growth projects, it is retaining half its cash flow, one of the highest amounts of any midstream.

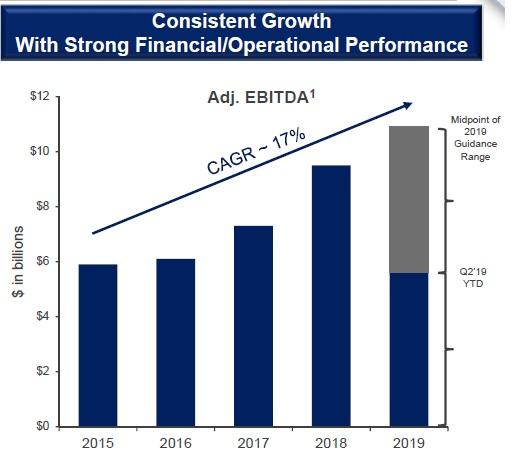

Leverage, what management has been working to bring down to a 4.0 to 4.5 range, hit 4.2 in Q2, and annualized retained cash flow hit $3.1 billion, with management raising full-year EBITDA guidance for the second time this year, to $11 to $11.1 billion.

Liquidity stands at $3.5 billion including $200 million in cash on the balance sheet. So is Energy Transfer running out of new growth opportunities?

For the full year 2019 as mentioned we have lowered our growth CapEx forecast to approximately $4 billion.

And for full-year 2020 we expect to spend approximately $4 billion excluding expenditures related to the SemGroup assets primarily in our NGL & Refined Products and midstream segments. Post 2020 the backlog of approved growth capital projects is approximately $1.5 billion. We will expect additional projects to be added to this backlog." - Thomas Long CFO, Q3 conference call

Actually no, ET has $9.5 billion in growth projects remaining on which its expecting to earn 10% to 20% EBITDA yields.

What most likely caused ET's acute weakness is fears over customers going bankrupt and breaking its long-term contracts, including volume commitments that will now underpin 90% of cash flow.

Or more specifically the market is worried about one company, in particular, US gas giant Chesapeake Energy (CHK).

SunTrust analyst Neal Dingmann explained in a Barron's article that

CHK’s credit facility contains a leverage covenant that begins at 5.5x for allowable leverage, and ramps down quarter beginning in 4Q19 by 25 basis points each quarter. On a total asset basis, we estimate that the company could brush up against this covenant in 3Q20 with our estimated net debt to LTM EBITDA of ~4.5x in 3Q20 vs. covenant restriction of 4.5x, after which we forecast the company to be out of compliance with the covenant...We believe the company will explore all options for asset monetization and additional strategies for leverage reduction given the ongoing concerns with debt levels, difficult high-yield markets, and decreasing covenant restrictions.” -SunTrust (emphasis added)

In 2015 at the peak of the oil crash 67 oil & gas companies went under, a 379% spike in bankruptcies.

How much did Energy Transfer's cash flow crash as a result?

It didn't, it actually went up modestly and has been growing at one of the industry's fastest rates ever since thanks to merging with ETP.

Ok, so that was then, but what about ET's exposure to CHK today?

Energy Transfer (ET), Kinder Morgan (KMI) and Plains All American Pipeline (PAA) also have exposure to Chesapeake, Smith and Van Everen write, though it is much smaller." - Barrons

How much is "much smaller"? ET doesn't disclose cash flow from any individual customer, but here is what management had to say to Goldman's question about contract exposure during its conference call.

It might be helpful for me to kind of start off with a higher level look but I will say that over 80% of our just normal credit exposure etc. when you look at it is all at large investment-grade companies. And then when you get into the rest of them there's no single one that even rises to a 1% type level. It makes up hundreds of counterparties." - Thomas Long, CFO

CHK is a B+ junk bond rated company meaning that ET's cash flow exposure to it is less than 1%.

For an MLP with a 1.98 coverage ratio a 1% hit to cash flow, and only in a worst-case scenario, is not a risk worth losing sleepover. It certainly doesn't justify the recent crash in the stock price. So let's talk about valuation, which for ET has truly become absurd.

Energy Transfer Fair Value

| Metric | Market-Determined Fair Value Multiple | 2019 Fair Value | 2020 Fair Value | 2021 Fair Value |

| 5-Year Average Yield | 6.94% | $18 | $18 | $18 |

| 13-Year Median Yield | 6.14% | $20 | $20 | $20 |

| 14-Year Average Yield | 6.06% | $20 | $20 | $20 |

| P/OCF | 7.1 | $39 | $44 | $46 |

| P/EBITDA Per Unit | 4.8 | $37 | $37 | $38 |

| P/EBIT | 7.6 | $38 | $40 | $41 |

| P to EV/EBITDA per unit | 4.8 | $37 | $37 | $38 |

| Average | $30 | $31 | $32 |

| Classification | Margin Of Safety Required For 8/11 Above-Average Quality Company | 2019 Price | 2020 Price | 2021 Price |

| Reasonable Buy | 0% | $30 | $31 | $32 |

| Good Buy | 15% | $26 | $26 | $27 |

| Strong Buy | 25% | $23 | $23 | $24 |

| Very Strong Buy | 35% | $20 | $20 | $21 |

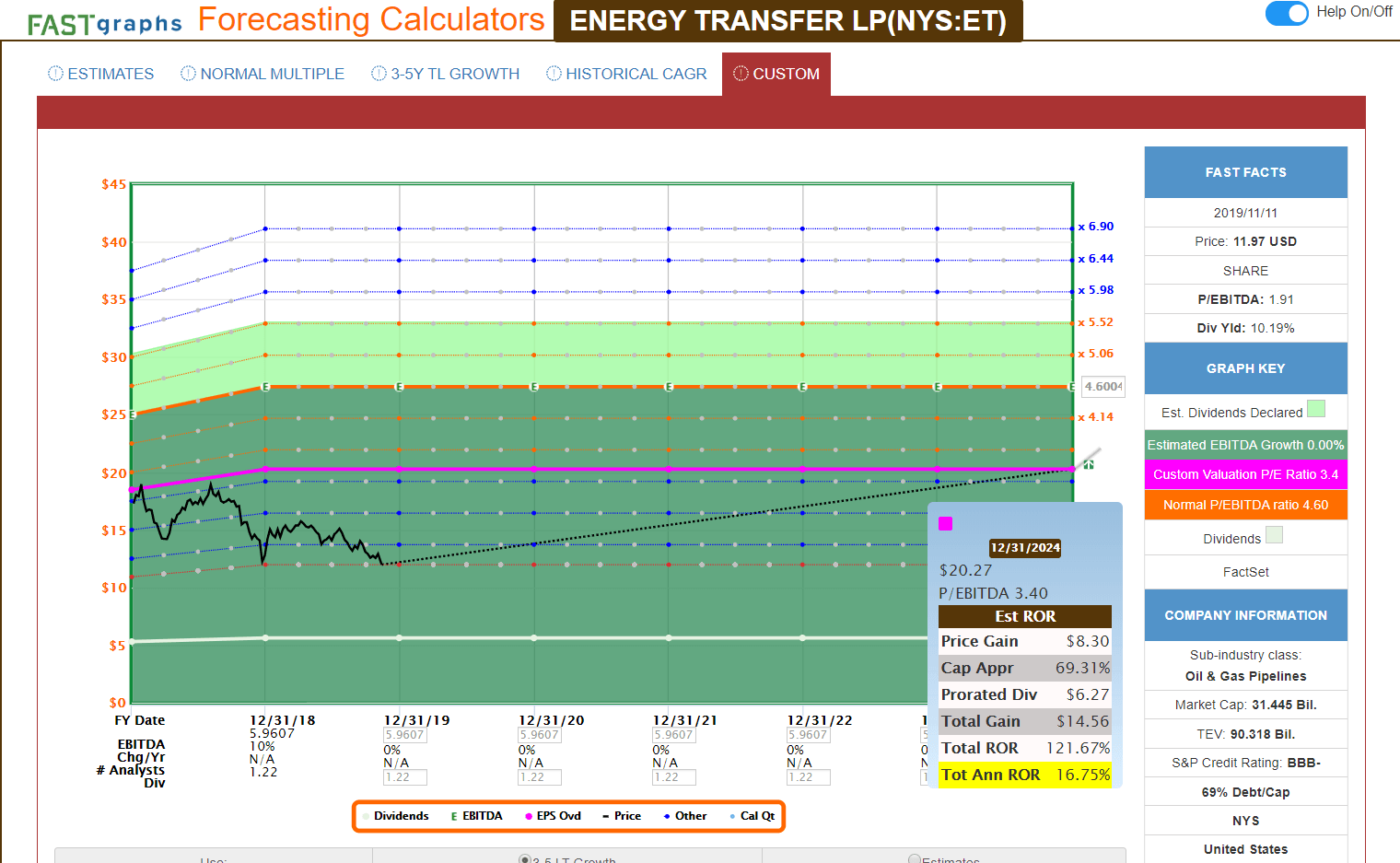

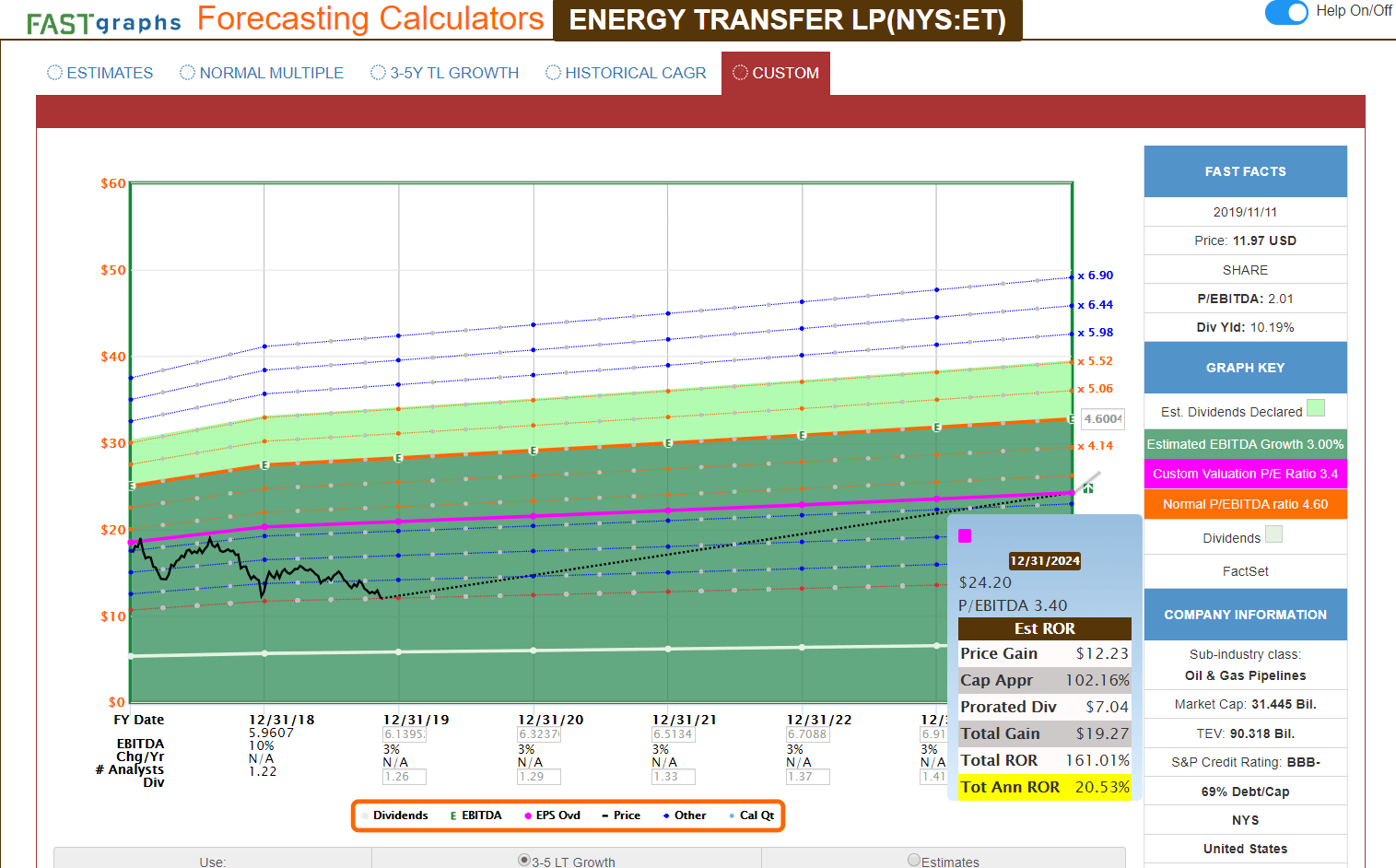

Energy Transfer at $12 is one of my highest conviction "very strong buys" because it's trading at a 60%, 61%, and 63% discount to 2019, 2020 and 2021 fair value. In six years as an analyst, I've literally never seen any company so undervalued.

Energy Transfer is an "anti-bubble" stock. That's something that Rob Arnott, Bradford Cornell and Shane Shepherd at US asset manager Research Affiliates determined in their study “Bubble, Bubble, Toil, and Trouble”. It “requires implausibly pessimistic assumptions in order to fail to deliver a solid risk premium”.

How can you tell if a company is in an anti-bubble? If you can earn double-digit total returns over time with zero growth, that's an anti-bubble stock.

The Ben Graham fair value formula baked into F.A.S.T Graphs estimates that even if ET were to grow at zero, it would be worth 4.6 times EBITDA per unit.

But just to be exceptionally conservative, let's assume that the MLP's 3.4 bear market multiple persists forever. Thank's to its truly irrational current valuation ET would still see strong multiple expansion and could deliver almost 17% CAGR total returns over the next five years.

If it languished at its current insane, depression-era multiple forever AND never grew at all? Then you'd earn a 10.2% CAGR total return purely from the safe and well-covered distribution. However, Energy Transfer isn't likely to not grow at all, in fact, its growth profile is highly attractive.

- FactSet long-term growth consensus: 6.0% CAGR

- Reuters' 5-year CAGR growth consensus: 16.5% CAGR (almost certainly too bullish)

- Ycharts long-term growth consensus: 6.0% CAGR

- historical growth rates: 15.0% CAGR over 14 years

- realistic growth range: 3% to 7% CAGR

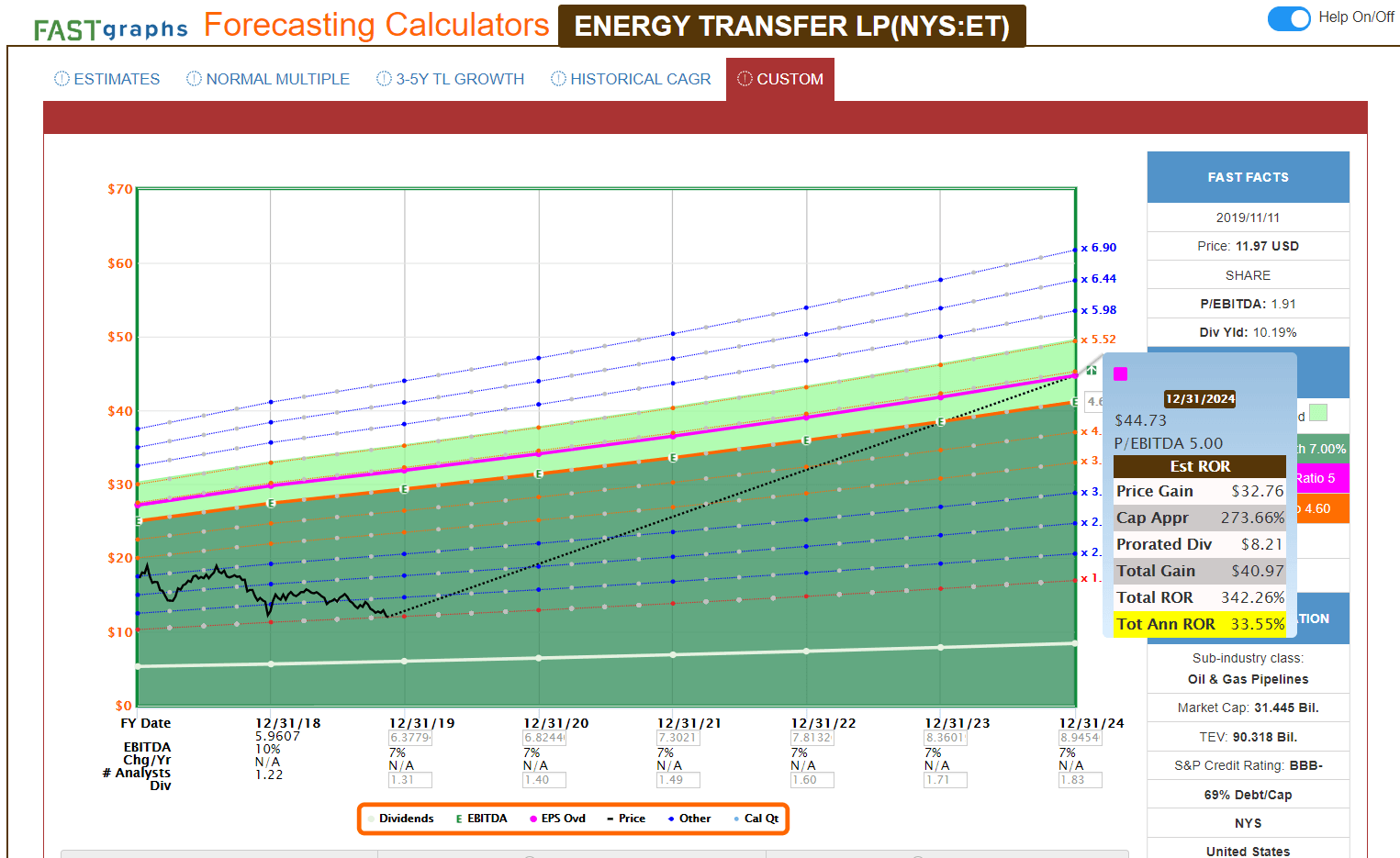

- historical fair value range: four to five times EBITDA/unit (3.4 bear market average)

So let's see what kind of returns investors buying ET, a $30 stock, for $12 can realistically expect.

Using super conservative assumptions, of 3% organic growth, achieved by the low end of management's capex growth guidance, the low end of EBITDA yields on new projects, zero highly accretive buybacks, and still using that 3.4 bear market EBITDA/unit multiple, ET appears capable of over 20% CAGR total returns.

If it grows at the upper end of its growth range, 7% (8% is possible if all it did was buy back stock with retained cash flow) and returns to the upper end of fair value, a five EBITDA/unit multiple, then over 300% total returns are possibly over the next five years.

Note that we're not even modeling Reuter's highly optimistic 16.5% CAGR growth consensus since that requires a large amount of stock-based M&A that is too speculative for our taste.

Purely organic growth that ET can achieve via growth projects and or buybacks and a return to its own historical valuation multiples is all that's needed for this safe 10% yielding anti-bubble stock to generate market smashing returns.

Why Wall Street Is Dead Wrong About MPLX

Of these three MLPs, MPLX has been hammered the most from the market's irrational panic selling.

What's more, MPLX's likely biggest catalyst for its recent fall is the silliest of all.

Elliot Management, an activist investor, has succeeded in getting Marathon Petroleum (MPC), who is MPLX's sponsor and owns 63% of its units, to force out CEO Gary Heminger and agree to spin off Speedway.

MPLX has also conceded to a "special committee" that will "continue to evaluate alternatives to enhance value across its midstream business." That includes Elliott's demand to spin-off MPLX and convert it into a c-Corp.

As I warned about in this article, Elliott's demands are not in the best interest of dividend-focused investors, just those looking for short-term capital gains.

Marathon losing Speedway's stable cash flows has resulted in Moody's changing MPC's and MPLX's credit outlook to Baa2 negative (BBB equivalent).

MPC's negative outlook reflects the company's decision to separate its more stable Speedway company-owned retail store operations into a newly independent, publicly traded company, as well as potential changes in the structural and organizational relationship with MPLX... Moody's regards the relative stability of the unlevered EBITDA generated by Speedway's motor fuels and convenience store sales as an important counter balance to the inherent volatility in refining, and the higher leverage at MPLX...While implications of the Speedway spin and a reevaluation of MPLX's relationship with MPC relative to MPC's balance sheet capitalization are undefined at this point, Moody's sees little risk of a non-investment grade outcome at either rated entity. MPC's outlook could be restored to stable depending on the extent to which Speedway separation proceeds are used for debt reduction at MPC." - Moody's

Worst case MPC ends up with a BBB- stable credit rating, but as Moody's says, paying down debt with the Speedway proceeds would likely cause it and MPLX to retain their BBB equivalent credit ratings.

What about new management? Heminger is being replaced by new MPLX CEO Michael Hennigan, who has 38 years of industry experience and plans to continue the current growth plan.

What about the possibility that MPLX converts into a c-Corp? While this might cause some investors to winch at the thought of "being Kindered" in reality conversion to a c-Corp does NOT mean MPLX's payout is at risk.

It means you might have a one-time tax liability but the only thing that determines the safety of the distribution is the fundamentals.

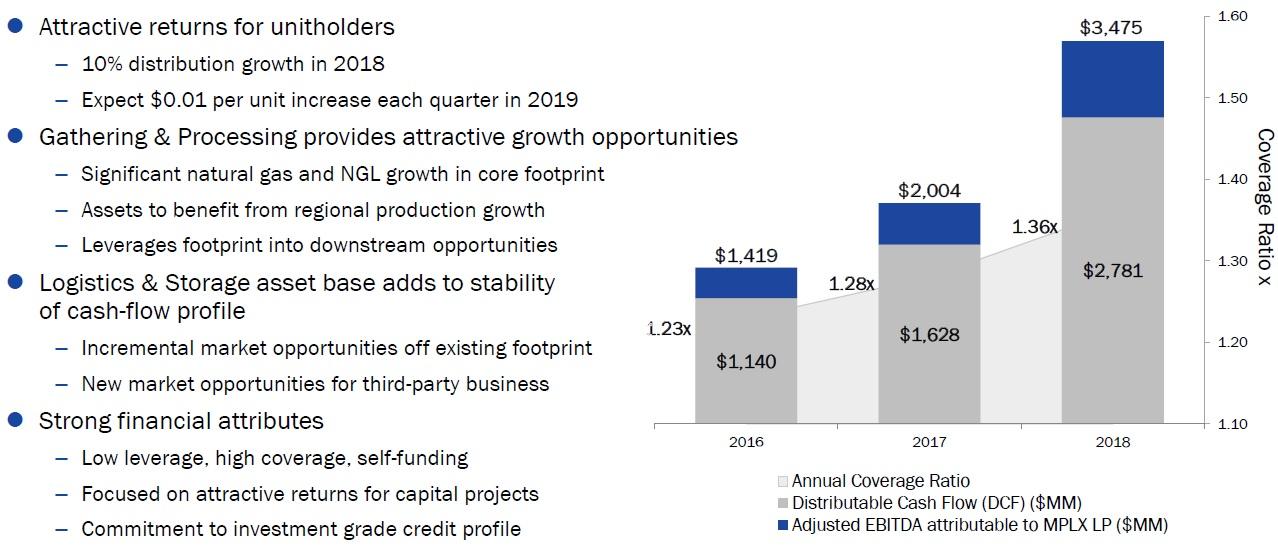

MPLX's distribution coverage ratio, despite 27 consecutive quarterly payout increases, has been steadily rising over time.

In Q3 it rose from 1.36 to 1.42, and on a YTD basis, it hit a record high of 1.54 vs 1.38 for YTD 2018.

Leverage came in at management's long-term target of 4.0 or less, which again, is very safe for a midstream. What about MPLX running out of growth projects?

For 2020, we are targeting growth CapEx of approximately $2 billion. This is approximately $600 million less than what the two prior midstream companies had projected in total. Virtually, all of the reduced spending is in the G&P segment of our business. In doing so, we believe we have selected the highest return projects available to us, which will best position us to deliver long-term value to our unitholders." - Michael Hennigan, new CEO, Q3 conference call

In 2019 MPLX will spend $2 billion on growth capex, and $2 billion more in 2020. It's focusing 75% of its spending on logistics and support assets, not gas gathering (in the Marcellus and Utica shale).

Not that MPLX's MarkWest assets are falling off a cliff. Far from it. YOY volume growth was 12% for gas gathering and 13% for processing, and the new ANDX assets saw even stronger growth.

Our target to spend approximately 75% of growth CapEx in the L&S segment continues to shift in our strategic direction over the last couple of years. At the same time, our G&P business remains an important part of our portfolio. Slowing Northeast growth allows our portfolio of premier G&P assets in the region to deliver positive cash flow, which can be deployed to our strategic investments, especially in the Permian." - MPLX CEO (emphasis added)

MPLX's gas gathering and processing segment makes up 34% of cash flow and is still growing. But due to uncertainties surrounding 2020 gas drilling, it's focusing its growth on the mighty Permian basin.

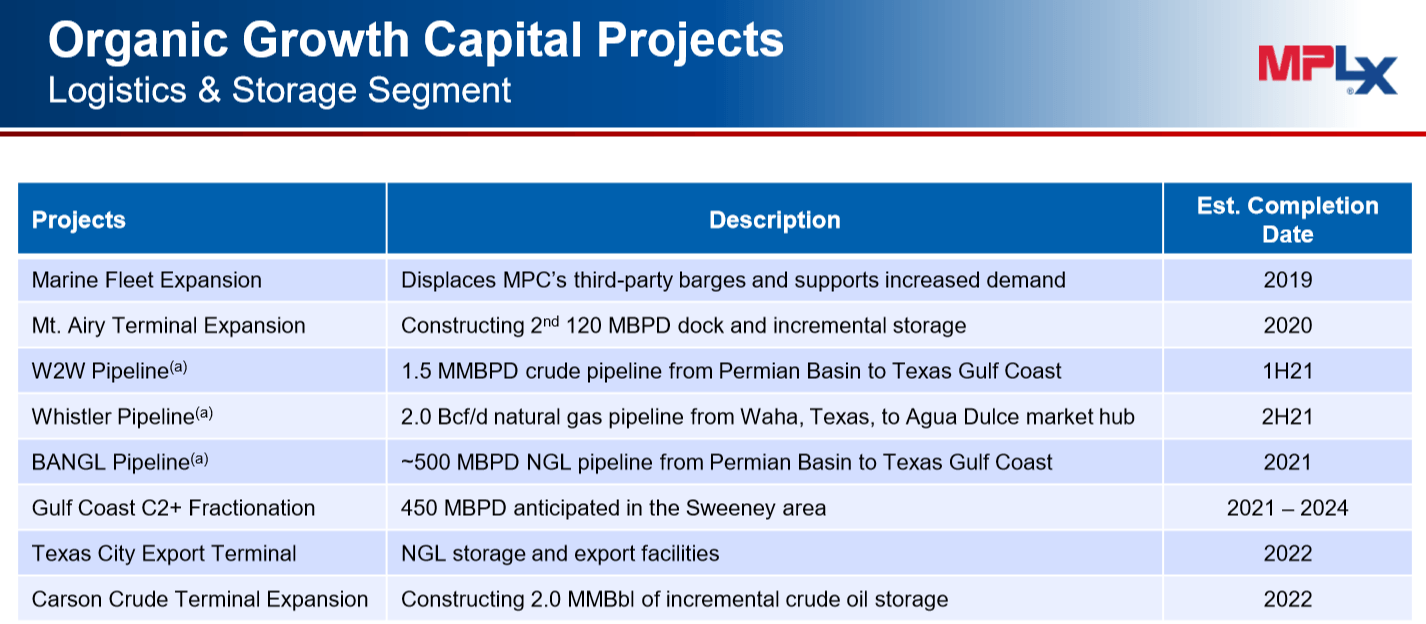

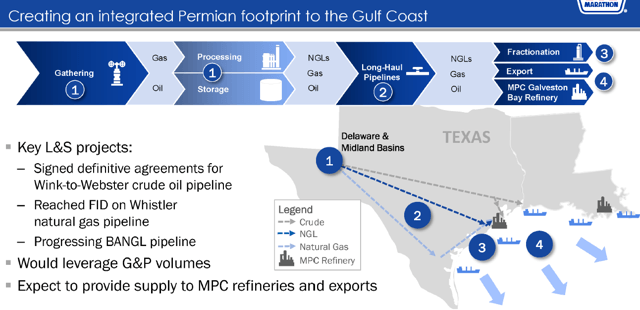

MPLX is building several gas pipelines in the Permian, as well as crude pipelines and expanding its new oil export terminal on the Texas Gulf Coast.

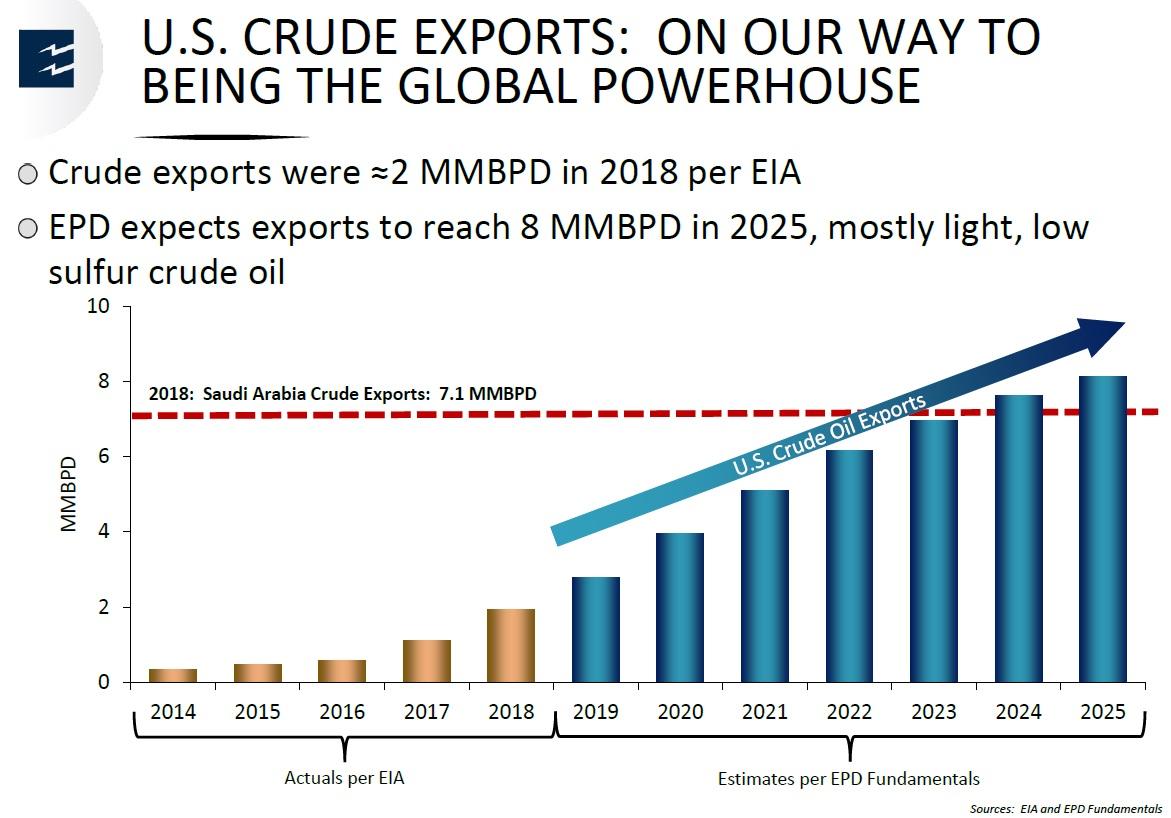

The US is poised to soon overtake Saudi Arabia as the world's largest oil exporter and gas production from the Permian is precisely what's causing Marcellus and Utica focused gas producers such angst right now. MPLX plans to profit from both secular energy trends.

It's true that Utica shale doesn't come with much minimum volume commitments.

Only in the Marcellus are gas giants like EQT (EQT) and Antero Resources (AR) locked in under "take-or-pay" contracts. However, all its gas gathering contracts are long-term, 10 to 15 years in duration and Permian gas volumes are exploding, because producers are bringing up gas as a by-product of oil production.

Only in the Marcellus are gas giants like EQT (EQT) and Antero Resources (AR) locked in under "take-or-pay" contracts. However, all its gas gathering contracts are long-term, 10 to 15 years in duration and Permian gas volumes are exploding, because producers are bringing up gas as a by-product of oil production.

In other words, Permian gas volumes are not at high risk of declining due to low gas prices. Meanwhile, 60% of cash flow is for MPC's midstream assets, which all come with 100% volume commitments from Marathon. Those have about 10 years remaining on them and without those assets, Marathon couldn't run its refining business (so they will be renewed when they expire).

In other words, I'm not worried about MPLX, an MLP with a 1.42 coverage ratio and $1.4 billion in annualized retained cash flow, having to cut its payout, even if things get rougher for Marcellus and Utica shale producers.

Is MPLX without risk? No, there is no risk-free stock. But the valuation is now so low that investors are being more than adequately compensated for what risks it does realistically have.

| Metric | Market-Determined Fair Value Multiple | 2019 Fair Value | 2020 Fair Value | 2021 Fair Value |

| 5-Year Average Yield | 6.48% | $41 | $44 | $46 |

| 7-Year Median Yield | 5.74% | $47 | $49 | $52 |

| 7-Year Average Yield | 5.21% | $52 | $55 | $57 |

| P/OCF | 9.8 | $44 | $55 | $59 |

| P/EBITDA Per Unit | 9.6 | $54 | $68 | $70 |

| P/EBIT | 13.4 | $56 | $68 | $73 |

| P to EV/EBITDA per unit | 9.6 | $54 | $68 | $70 |

| Average | $50 | $58 | $61 |

| Classification | Margin Of Safety Required For 8/11 Above-Average Quality Company | 2019 Price | 2020 Price | 2021 Price |

| Reasonable Buy | 0% | $50 | $58 | $61 |

| Good Buy | 15% | $43 | $49 | $52 |

| Strong Buy | 25% | $38 | $44 | $46 |

| Very Strong Buy | 35% | $33 | $38 | $40 |

MPLX at $24 is 51%, 59% and 61% undervalued for 2019, 2020 and 2021, respectively. It's also an anti-bubble stock that, barring an unlikely and complete collapse of its business model will deliver double-digit returns from its safe and growing distribution alone.

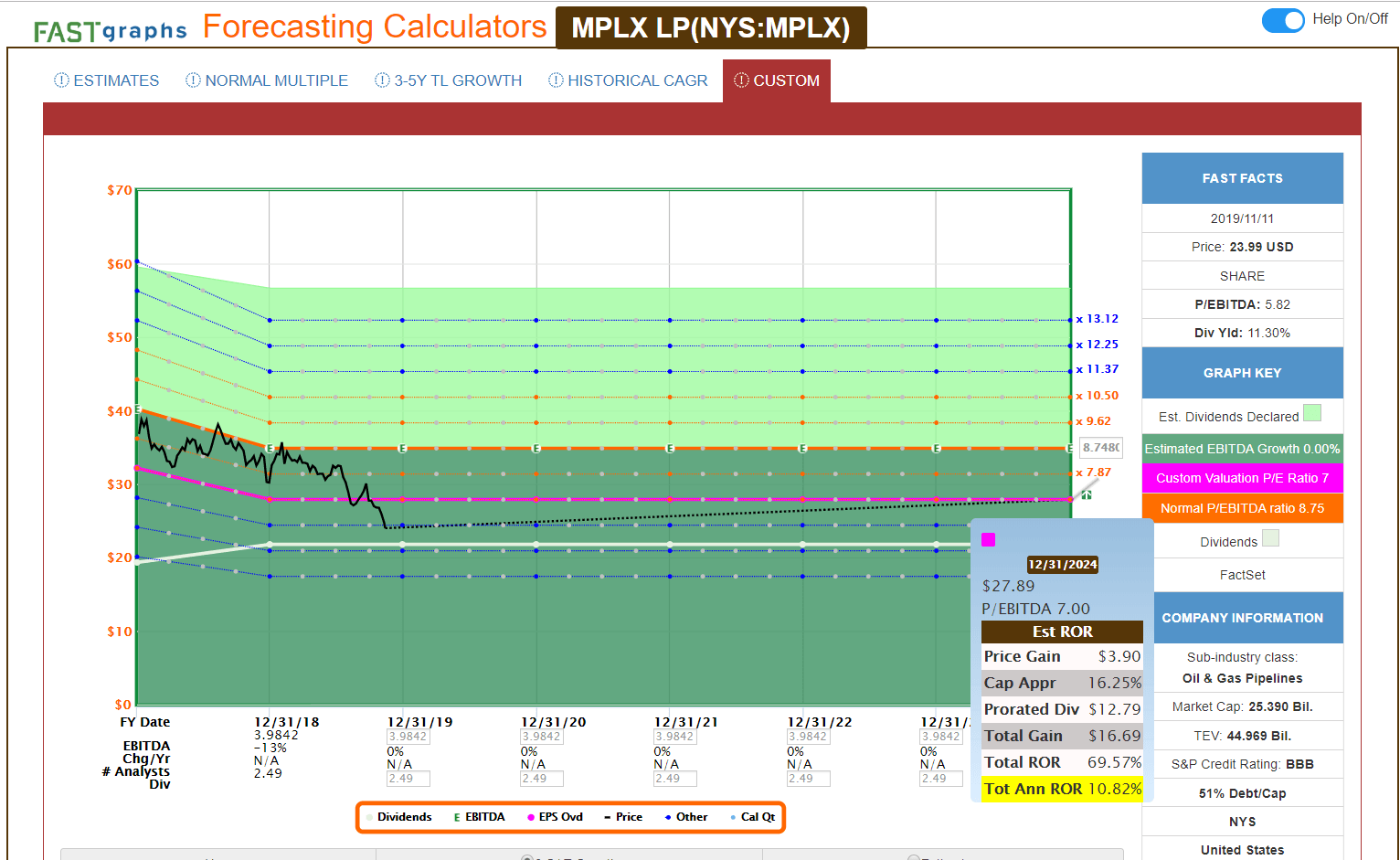

Using the Graham Formula, F.A.S.T Graphs estimates that MPLX growing at zero forever is worth 8.8 times EBITDA per unit. Even if we use the lower end of its bear market valuation range and model 7 times EBITDA, we still get double-digit returns, all from its safe distribution.

But like all these MLPs I'm highlighting today, MPLX is thriving, not stagnant.

- FactSet long-term growth consensus: 4.0% CAGR

- Reuters' 5-year CAGR growth consensus: 5.1% CAGR

- Ycharts long-term growth consensus: 4.0% CAGR

- historical growth rates: 12.6% CAGR since IPO (due to dropdowns)

- realistic growth range: 3% to 5% CAGR

- historical fair value range: seven to nine times EBITDA/unit (including during this bear market)

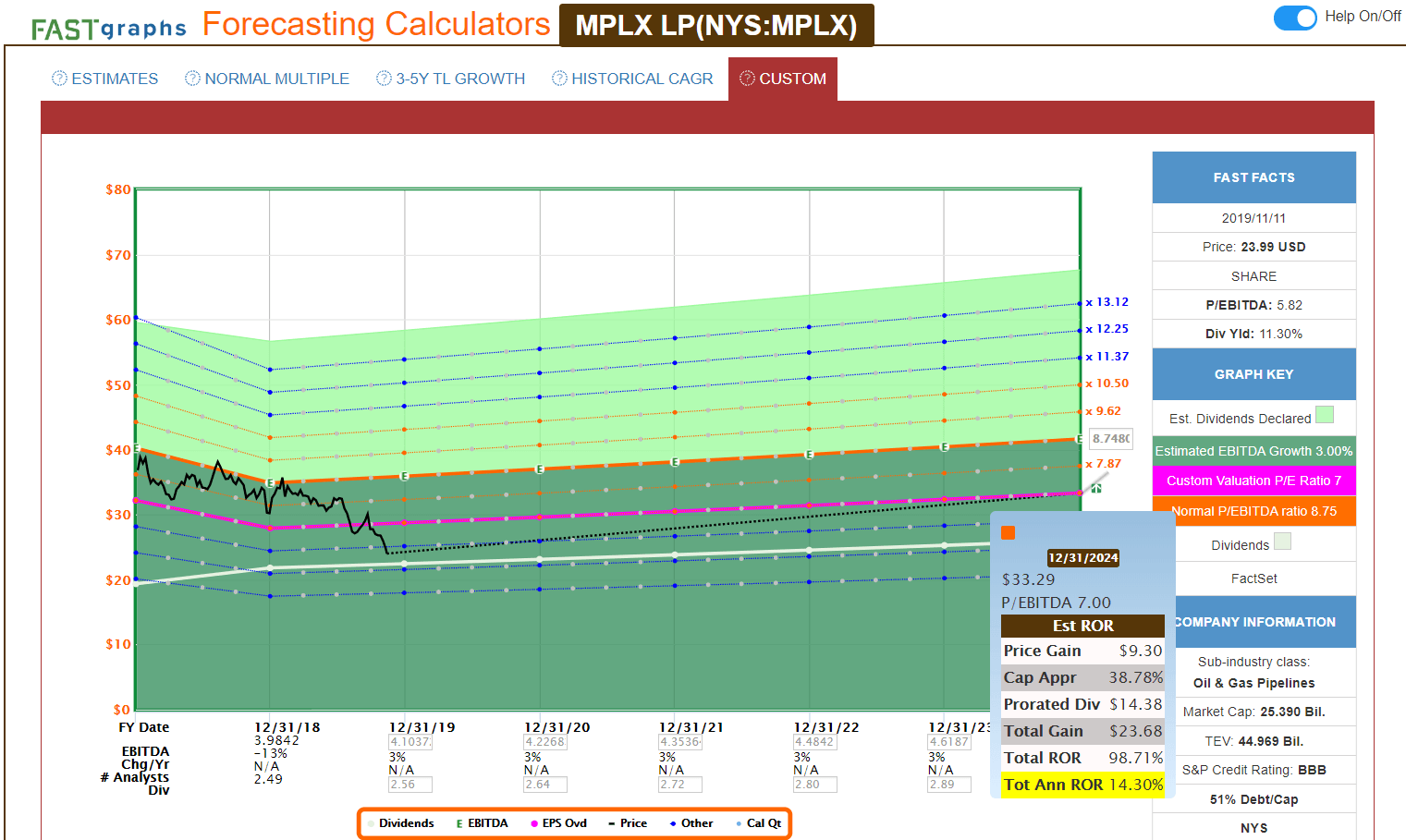

MPLX growing slower than all analysts expect and returning just to the low end of its bear market historical multiple can realistically double your investment over the next five years.

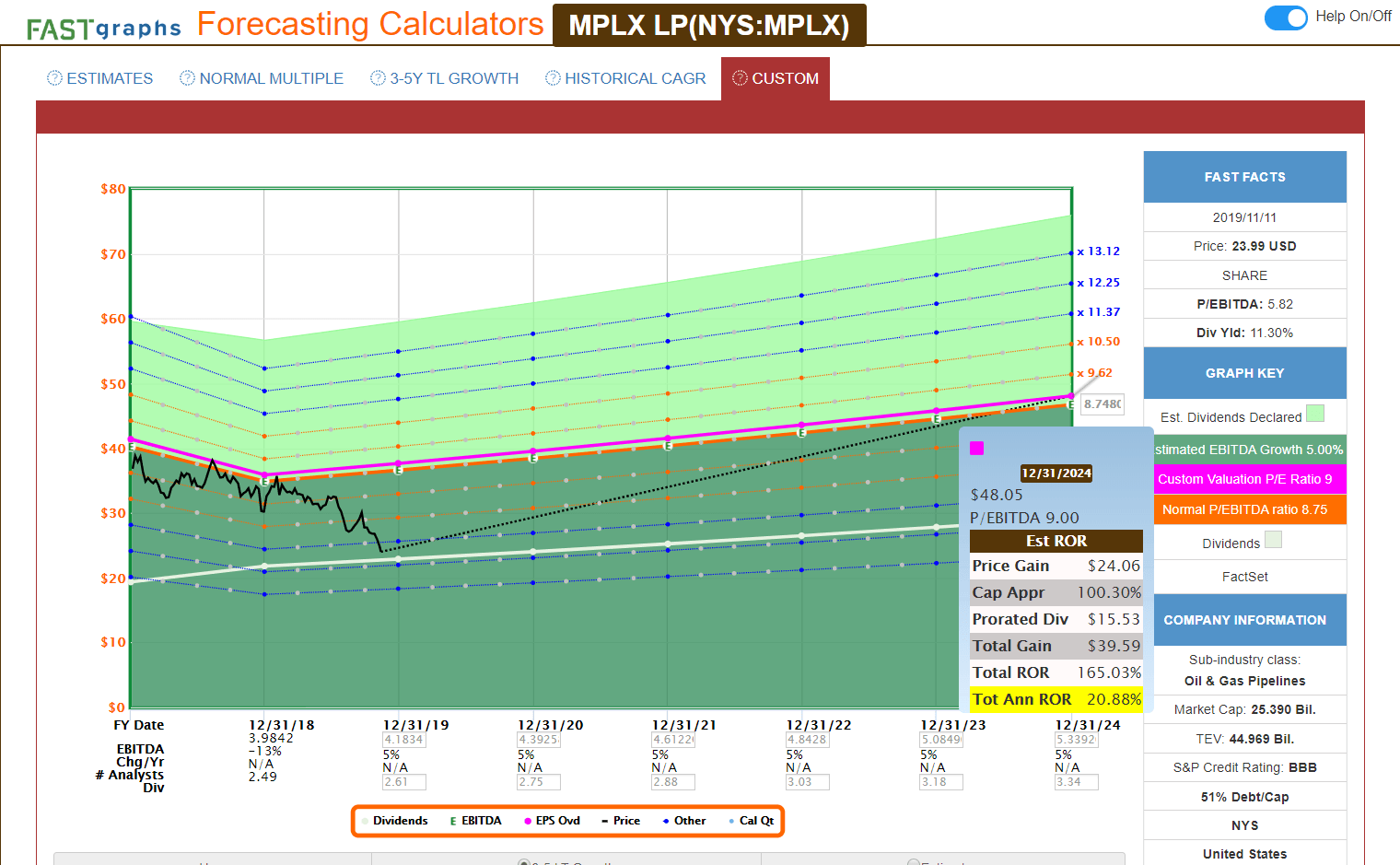

If MPLX cranks up the buybacks in the future and grows at 5%, and merely returns to a P/EBITDA per unit of nine, it could deliver 21% CAGR total returns.

THAT is the power of a safe 11% yield and anti-bubble valuations.

Risks To Consider

Fundamental risks for all MLPs include execution risk on projects, including costly delays in which environmentalists block major projects, sometimes requiring them to be canceled.

Fundamental risks for all MLPs include execution risk on projects, including costly delays in which environmentalists block major projects, sometimes requiring them to be canceled.

Energy Transfer has had a fair share of execution issues from 2015 to 2017, though its restructuring of project teams appears to have been a success. That's not to say it will never face mishaps again, but it appears that a stronger focus on simpler projects, rather than multi-state or transnational pipelines should result in less fundamental angst for ET investors in the future.

MPLX and EPD are similarly stocking to more regionally located projects, in energy-friendly states with less legal/regulatory risk.

The long-term risk, which isn't really a risk but merely a fundamental fact, is that one-day midstream's infrastructure will not be needed. We can't know when that day will come, but it's likely several decades away.

The earliest estimates I've seen for when oil & gas will make up less than 50% of the world's energy mix is from BP, and that's 2035.

Here's what McKinsey's 2050 Energy Outlook report concluded

Fossil fuels will dominate energy use through 2050. This is because of the massive investments that have already been made and because of the superior energy intensity and reliability of fossil fuels. The mix, however, will change. Gas will continue to grow quickly, but the global demand for coal will likely peak around 2025. Growth in the use of oil, which is predominantly used for transport, will slow down as vehicles get more efficient and more electric; here, peak demand could come as soon as 2030....Overall, though, coal, oil, and, gas will continue to be 74 percent of primary energy demand, down from 82 percent now. After that, the rate of decline is likely to accelerate." -Mckinsey (emphasis added)

US oil & gas production is likely to remain the world's swing producer, resulting in several decades of steady cash flow for these MLPs. Once growth projects are no longer economically justified, buybacks can keep DCF/unit and payouts rising safely for many years beyond peak new midstream infrastructure demand.

However, there is an expiration date on midstreams, which are not a "buy and hold forever" investment. That expiration date is likely to be 20 to 30 years from now, which for most retirees or near-retirees, still makes them excellent long-term holdings in a properly risk-managed portfolio.

Risk management is the most important part of long-term investing success. That's because 20% to 40% of investments won't work out as planned (according to Peter Lynch and Howard Marks). Quality companies with competent and trustworthy management, bought at a sufficient margin of safety are just one part of managing risk.

Risk management is the most important part of long-term investing success. That's because 20% to 40% of investments won't work out as planned (according to Peter Lynch and Howard Marks). Quality companies with competent and trustworthy management, bought at a sufficient margin of safety are just one part of managing risk.

Proper asset allocation, the mix of stocks/bonds/cash you own, is the most fundamental risk management principle of all.

Bonds have always acted as a shock absorber to stock market declines...Bonds can provide dry powder to rebalance into the stock market or pay for current expenses when the stock market inevitably goes through a nasty downturn. Bonds keep you in business even if they don’t provide high returns as they have in the past." - Ben Carlson (emphasis added)

No dividend stock is a true bond alternative, no matter how stable its cash flow or how safe the dividend.

Long-duration US Treasuries have fallen 20% twice since 1926. In contrast, these three MLPs, while less volatile than the broader market over time, have suffered far higher short-term volatility.

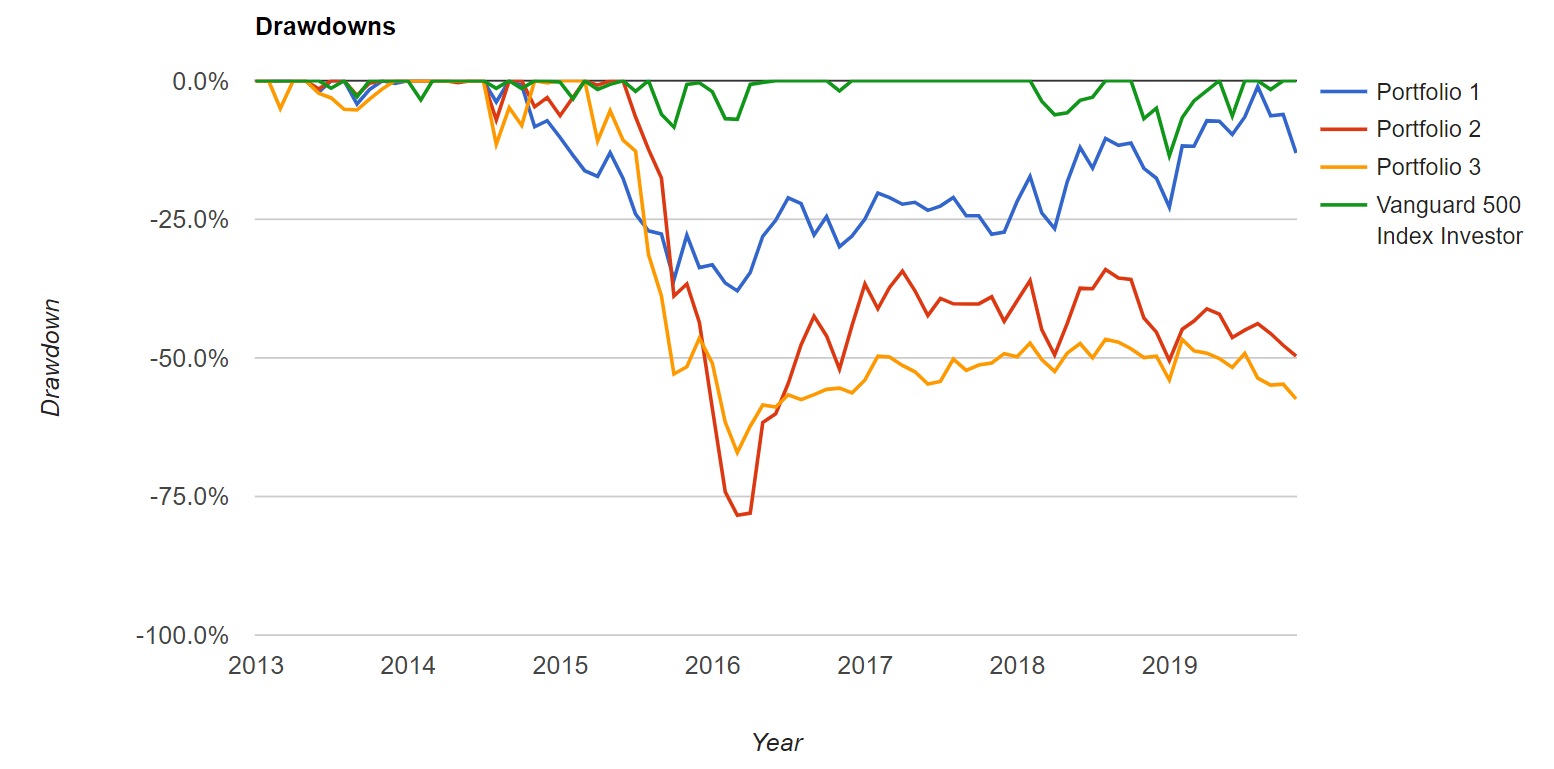

EPD, ET and MPLX Peak Declines Since 2013

Remember that anyone who has owned all of these MLPs since 2013 has still made money, thanks to safe and rising distributions. Only those who bought at outlandish valuations (like the 2015 industry bubble) and sold, out of financial necessity or just plain fear, have lost money owning these three MLPs.

Long-term success with income investing requires the ability to patiently wait out irrational and very long bear markets such as this. This is why portfolio construction, asset allocation, and proper sector, industry, and holding size limits are so important.

These are what keep you "in the game" long enough to win it. The long-term might be all about the fundamentals, but it's also made up of thousands of short-term periods in which fear and sentiment (like blind panic we're seeing today) dominate.

Risk management is how you win by not losing, avoiding critical single points of failure that can turn you into a forced seller of quality income stocks bought at reasonable, or in this case, amazing valuations.

Bottom Line: Insane MLP Panic Selling Is Creating The Best Buying Opportunities In A Decade For EPD, ET, and MPLX

I am NOT a market timer, just a fundamentals/value-focused investor. I can't tell you when this irrational MLP crash will end but barring a catastrophic breakdown on the entire industry, it most assuredly will.

Fundamentals are the only thing that determines stock prices in the long-term. Cash flow and the safe payouts that stem from them are what MLP investors can and should count on.

Enterprise, Energy Transfer and MPLX have rock-solid fundamentals as seen in their most recent earnings results. These are not dying value traps but steadily growing energy utilities with rising cash flows, falling leverage, strong coverage ratios, and long growth runways to pursue via self-funding business models.

Eventually, the market will recognize these objective facts, and then multiple expansion will make patient and disciplined high-yield investors seem like geniuses. In reality, all we're doing is recognizing fundamental value that's attractively priced.

Today EPD, ETP, and MPLX are trading at their most attractive valuations in a decade, or in the case of MPLX, ever. 22% to 60% margins of safety are rare for quality assets, as is the potential to lock in safe 6.7% to 11.3% yields that will grow steadily over time and likely generate market-crushing double-digit returns, not just for years, but probably for decades.

While there are no guarantees on Wall Street, this latest MLP freakout has all the hallmarks of blind panic selling that is what happens right before capitulation, and a strong and sustained long-term rally begins.