I have written before about the shift that appeared first in September when investors dumped their tech-heavy winners and bought barrels of underperforming financials, industrials, old-tech names, and even banks. My interest was more than academic; being on the wrong side of that trade, our firm experienced some of the worst singles days of relative performance in our fourteen-year history. So, I was motivated to understand its source.

At the time, it almost appeared as if investors (or machines) chucked the top-performing decile of the S&P in exchange for the bottom fifty. I wrote that this phenomenon, while dramatic and painful, was unlikely to hold down those growth stocks that could satisfy the market’s appetite for strong earnings acceleration. The fact that our portfolio stopped its slide and my heart rate settled down was evidence that buyer interest was broadening to include banks, biotech, retail, and energy, as well as many prior winners.

Something, however, kept nagging at me. In fact, almost every day, for the past three months, we have heard or seen comments by the financial media telling us that value is outperforming growth. What has bothered me about that concept is that the technology sector was barreling toward a 50% gain for the year, well above any other sector. The closest was communication services, up 34%, which includes names like Facebook, which were formerly in tech until the S&P pruned off branches here and there to rename its components.

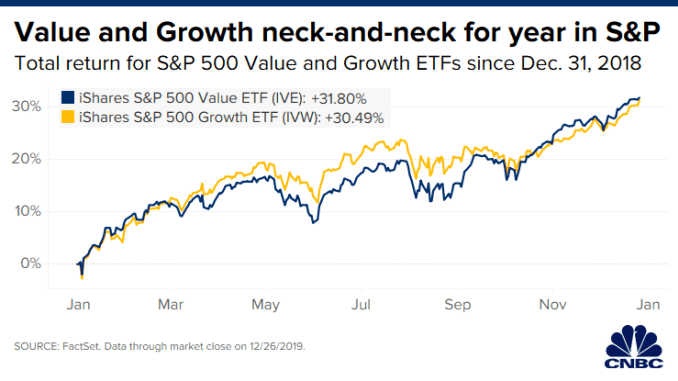

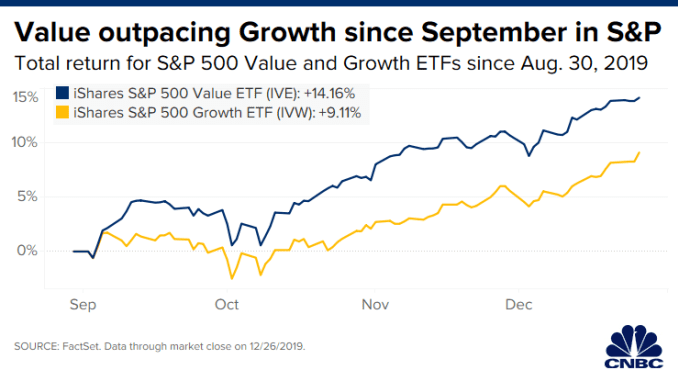

The S&P Value Index, in fact, outperformed the Growth Index in 2019, as shown in the charts below with almost a 5% premium during the last four months of the year. I was scratching my head – how can that be? A close look at the constituents of the S&P Value and Growth indices offers a somewhat misleading key to the puzzle. Its name is APPLE.

Both S&P and Russell have their secret sauce for placing stocks in either the growth or value bucket. S&P rebalances frequently and Russell only twice a year. Primarily because Apple traded at such a low PE at the beginning of the year, its 80%-plus gain through November 30th accrued entirely to the S&P Value index. Not only did Apple end its value run at a 9.5% index weight, but the stock’s 5.14% contribution to the total index return roughly equaled that of JP Morgan, AT&T, Brookfield Asset Management, Citigroup, Costco, Walmart, and Procter & Gamble combined.

Notable within the top 25 contributors to the Value index are an absence of drug companies, only one utility at #25, one energy stock, and one sole industrial – GE. There are more semiconductor names than energy and industrials combined.

Which leads me to conclude that crowning value the winner over growth is both misleading and ironic, since most investors consider Apple solidly a “growth” company, even when it trades at a sub-market multiple. Investors need to acknowledge that “technology” is such a large and diverse market segment that both major members of its league and entire teams, such as semis, can suddenly take residence within the value assemblage, when they stumble or fall out of favor.

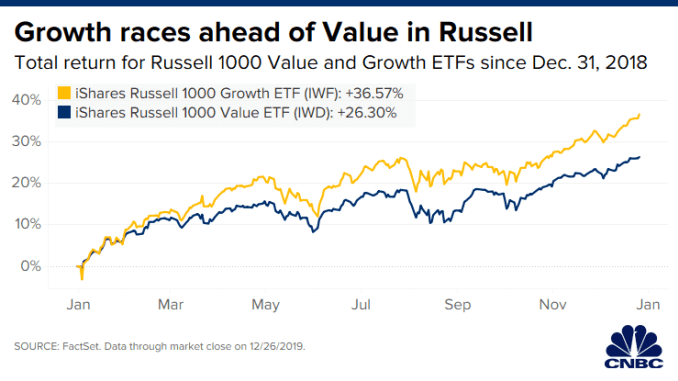

If we removed the full weight of Apple and the chipmakers from the value index, the picture would be very different. Actually, the Russell indexes allow stocks to be split between value and growth based on a range of characteristics. The charts below illustrate that, using this methodology, which allows Apple and names like Advanced Micro Devices and Nvidia to contribute to both indices, growth outperforms value for both the full year and the last four months of the year, when Apple and the chip stocks staged incredibly strong rallies.

With the mystery solved, I realize that I need to pay attention the next time die-hard value or growth fans claim their stocks are outperforming. It might be worth diving into the components of whatever index they are using because those claims could have originated from an unintended case of mistaken identity.