The past year has been a tough one for publicly traded cannabis companies, particularly multi-state operators in the United States, many of whom have seen their valuations drop to a quarter of their early 2019 highs. This decline in value coupled with the current Covid-19 virus-fueled economic downturn has many investors sitting on the sidelines. But a host of factors are brewing that could cause a powerful tailwind for the U.S. cannabis industry.

Many U.S. operators, particularly those with a strong focus on operating fundamentals, have already started to see their valuations rebound off the lows from late 2019 and early 2020. But these companies should still have lots of room to grow. In fact, a strong argument can be made that many American cannabis stocks are attractively valued compared to their current and anticipated long-term growth rates.

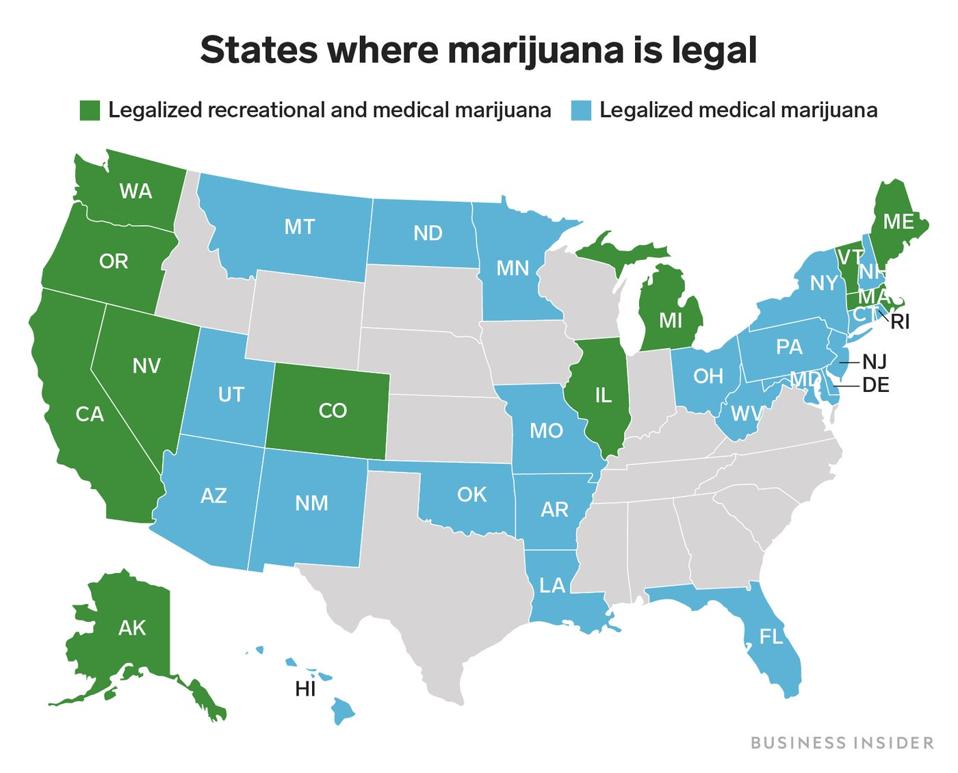

American cannabis company valuations also continue to lag their peers in Canada, despite what’s demonstrably better recent operational and financial performance and clear sight lines in larger addressable markets. Canada has already legalized cannabis nationwide, and while implementation has been slow and rocky, it is no longer in its initial phases. In a country of only 37 million people, Canadian cannabis companies like Canopy Growth and Aurora must rely on nascent international markets to substantially grow their revenue, while in the U.S., only 11 of 50 states have legalized for adult use and cannabis remains a Schedule I controlled substance at the federal level, leaving lots of room for growth and expansion at home in a country with nearly ten times Canada’s population.

Perhaps most importantly, the fundamentals of the top U.S. cannabis companies are strengthening almost across the board, despite the American and global economies being rocked by the coronavirus pandemic and the ensuing economic downturn. Market leading operators like Green Thumb Industries, Curaleaf and Trulieve are all expected to surpass $100 million in quarterly revenue in Q2 of 2020, marking the first time that three U.S. companies will pass this milestone. Even mid-sized multi-state operators, like my own company 4Front, have reported meaningful revenue increases over the past six months.

Notably, these revenue increases have happened in the industry despite the general economic downturn with states across the country reporting record cannabis sales. The most recent state to legalize, Illinois, recently reported record monthly sales of $47.6 million in June, marking the fourth straight month of sales growth, all during the pandemic. Sales in five western states (Arizona, California, Colorado, Nevada, and Oregon) have also continued to grow, with total sales across those states up 14% from $644.9 million in April to $735.4 million in May.

This looks to be answering a popular question about the cannabis economy: How would it hold up during an economic downturn? While alcohol has long been seen as a recession-proof industry, cannabis only became legal in Colorado and Washington in 2012, so until now there has been no reliable data to show how cannabis sales may fare in a down economy. The sales data for the first four months of the Covid-19-fueled downturn seem to indicate the same is likely true for cannabis, as it is proving to be a consumer staple. For investors looking for a relatively safe investment during what could be a prolonged recession or depression, cannabis stocks may be one of the smarter plays in the market today.

This is not to say that all American cannabis companies are without risk, as well publicized troubles plaguing industry giants MedMen and Acreage Holdings have made clear. Investors should pay close attention to management teams and operating fundamentals in deciding where to park their capital. But recent industry trends should be viewed positively, as cannabis companies by in large have shifted their strategies and made adjustments that favor traditional business fundamentals over the stock promotion, license aggregating, and hype that dominated the cannabis stock boom of 2017– 2019, burning many investors.

There has also been a shift among the C-Suites of cannabis companies across North America, with businesses replacing promoters and financial engineers in their management with real operators focused on execution and operational capabilities. Companies have also seen the light on right sizing their cost structures, jettisoning non-cash flowing or low revenue licenses that mostly served as “dots on a map” to demonstrate a large license portfolio, while focusing on core markets and assets that provide real time returns on their investments. Coupled with right sizing their staffs to reduce cash burns that have plagued the industry through the years, these companies have set the stage for profitable growth and real operating leverage moving forward.

With many cannabis companies now better focused on operating fundamentals and profitability, they are well positioned to take advantage of the legislative and regulatory changes to come in the near future. The cannabis industry has already been deemed essential in nearly every state during the height of the pandemic shutdown, and it is clear that state governments recognize the tremendous impact that cannabis businesses can and do have on their state coffers. It is difficult to see states rolling back progress. Rather, we could see more states and the federal government starting to look at legalization as a new source of much-needed revenue during a period of economic and budgetary distress.

And real reform at the federal level may be on the horizon, which would very likely provide a huge boost in the valuations of American publicly traded cannabis companies. The SAFE Banking Act, which would provide access to banking for cannabis businesses in the U.S. and likely open up new avenues for investment capital, already passed the House of Representatives as a standalone bill in 2019, and again as part of the HEROES Act, the latest attempt at a Covid-19-relief package in the House. While neither went on to become law, efforts are underway to ensure that relief for cannabis businesses is included in whatever new Covid-19-relief package is passed when Congress returns from their summer recess, potentially injecting new life, protections and capital into the fledgling industry.

With the Democratic Party having shown an increased interest in legalization at all levels, a Democratic sweep of the House, Senate, and White House in November could lead to full scale federal legalization in 2021 or 2022, despite reluctance on the part of the Democratic standard bearer Joe Biden. While not an entirely partisan issue, it has largely been Republican leadership in the Senate that has proven the largest impediment to federal reform.

All told, given the shift that cannabis companies have made towards operating fundamentals in the past year, coupled with rising sales and good prospects for coming legislative changes, now is as good a time as ever for investors to take a fresh look at publicly traded American cannabis companies. This may be the best industry-wide, long-term investment opportunity the market has seen since the crash of the dot-com bubble in the mid-1990s, and the subsequent explosion of operations-focused tech companies that came to dominate the global economy in the following decade.