Thesis Summary

Trulieve Cannabis Corp. (OTCQX:TCNNF) is a medical cannabis company with most of its operations based in Florida. This company is a rare find in the cannabis space, due to its high growth, sound finances, and good profitability. Despite a +100% appreciation of the stock in the last year, I think Trulieve is still undervalued given the growth potential, and I believe the stock price could double once again in 2021.

Company Overview

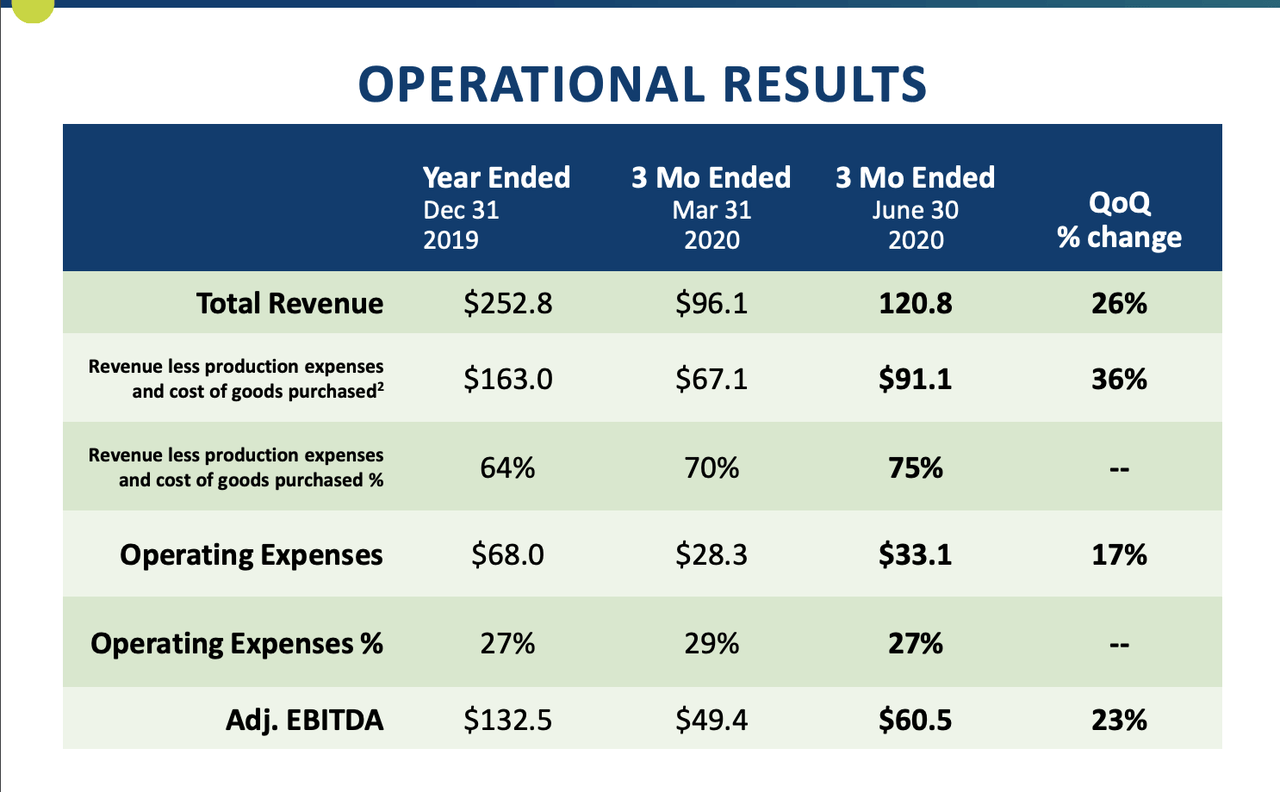

Trulieve operates as a producer and distributor of legal use marihuana, with most of its operations based in Florida. The company has seen revenue growth of 120% and is expanding its operations both regionally and in terms of product offerings. Trulieve Cannabis shares have been skyrocketing in the last year on the most recent results:

Trulieve has been able to achieve triple-digit growth in the last year, while also keeping a lid on expenses, showing impressive customer retention rates and organic growth. Furthermore, the company has been able to achieve this without further expanding its indebtedness. Trulieve carries around $130 million in long-term debt, which is about the same as a year ago. However, this now represents only 18% of assets and interest expenses, at 6.5% of revenue, seem manageable.

All in all, Trulieve looks reasonably financially secure, has outstanding growth, good profitability, and is by many metrics cheaply valued. But what can investors expect for this company during the next year?

Market and Competition

The cannabis market has been a hot topic of discussion for the past few years. It is undeniable that there is an ever-increasing demand for both recreational and medical uses. In this regard, it seems that the market still has significant growth ahead of it.

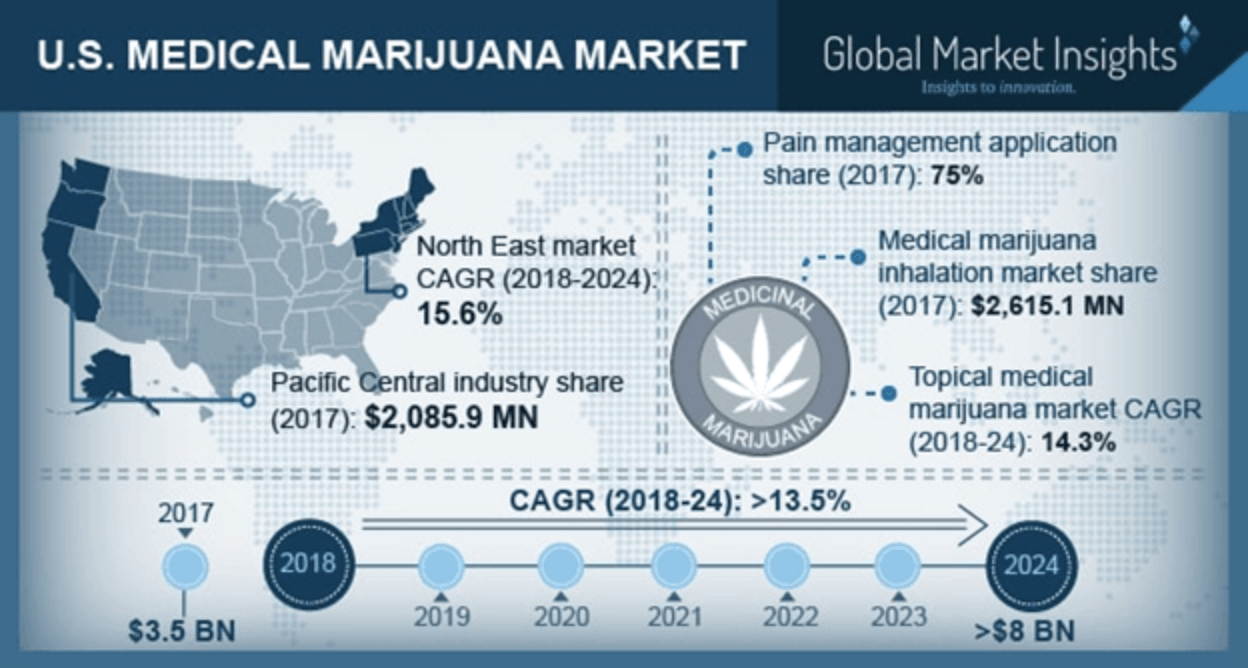

According to Global Market Insights, the U.S. cannabis market could grow to $8 billion by 2024. Interestingly, much of this growth could be found in the North East of the country, a geographical market that the company has just entered. Despite all this, returns for the sector have underwhelmed investors over the past 3 years.

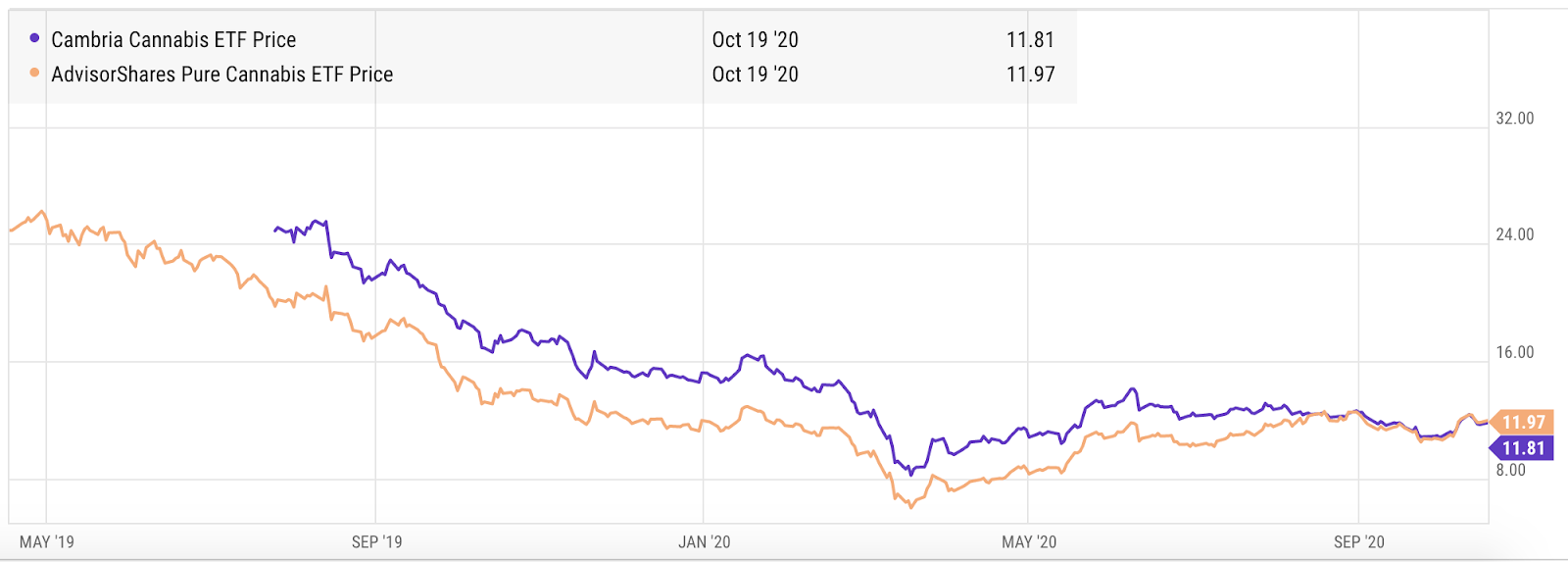

The graph above shows the return of a couple of ETFs in the sector; Cambria Cannabis ETF (TOKE) and AdvisorShares Pure Cannabis ETF (YOLO). These ETFs hold some of the biggest names in the industry but have lost over 50% of their value since their inception. However, Trulieve can be seen as an exception. While the stock traded sideways since its IPO in 2018, it has enjoyed great returns and profitability in the last year.

Trulieve is currently a market leader in Florida, but it will have to compete with other players for the rest of the domestic market. For example, Illinois based Green Thumb Industries (OTCQX:GTBIF) also operates a similar business, both growing and distributing cannabis products. Green Thumb has been growing revenues at over 200% in the last year and, unlike many other players, is also relatively profitable.

Growth Outlook

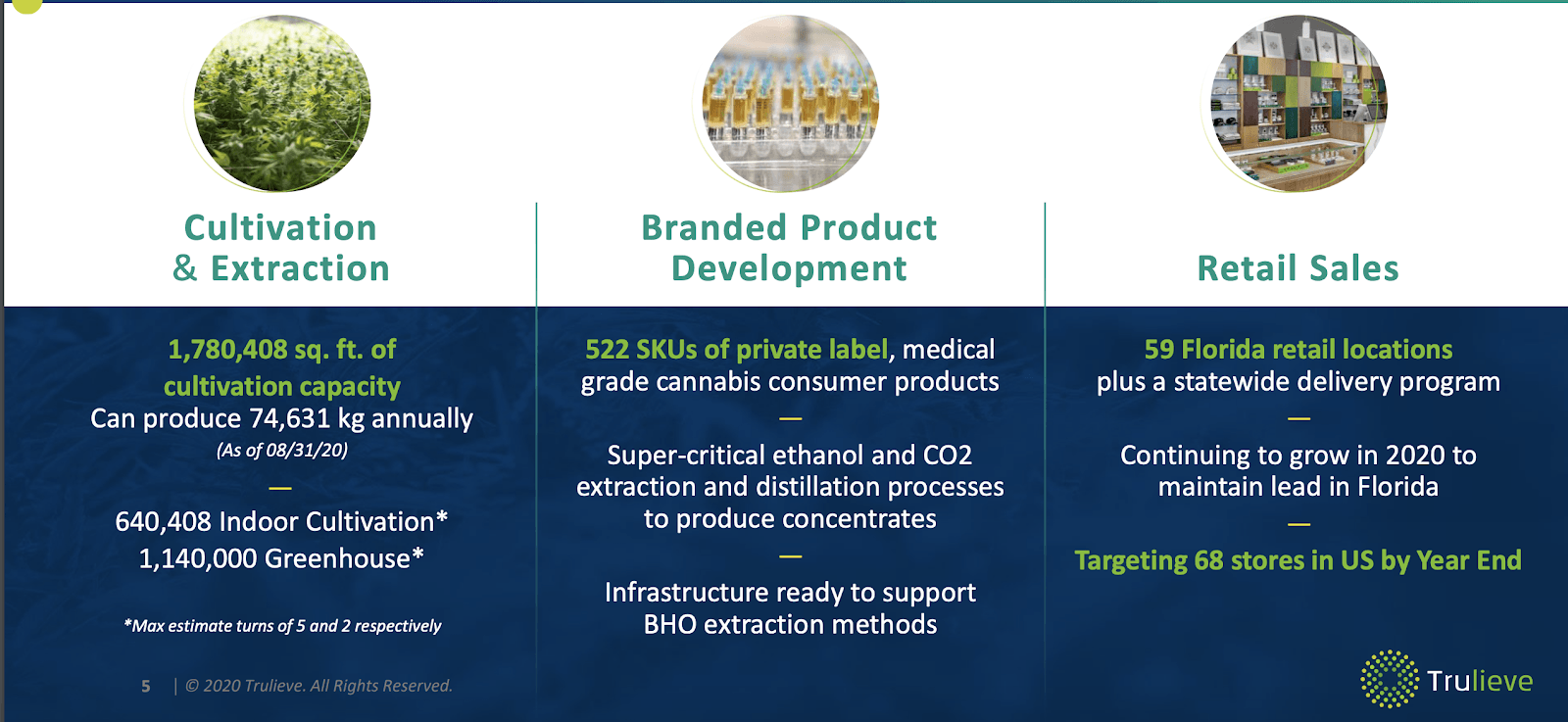

What sets Trulieve apart from many other producer and distributors are its vertically integrated operations and strong branding efforts:

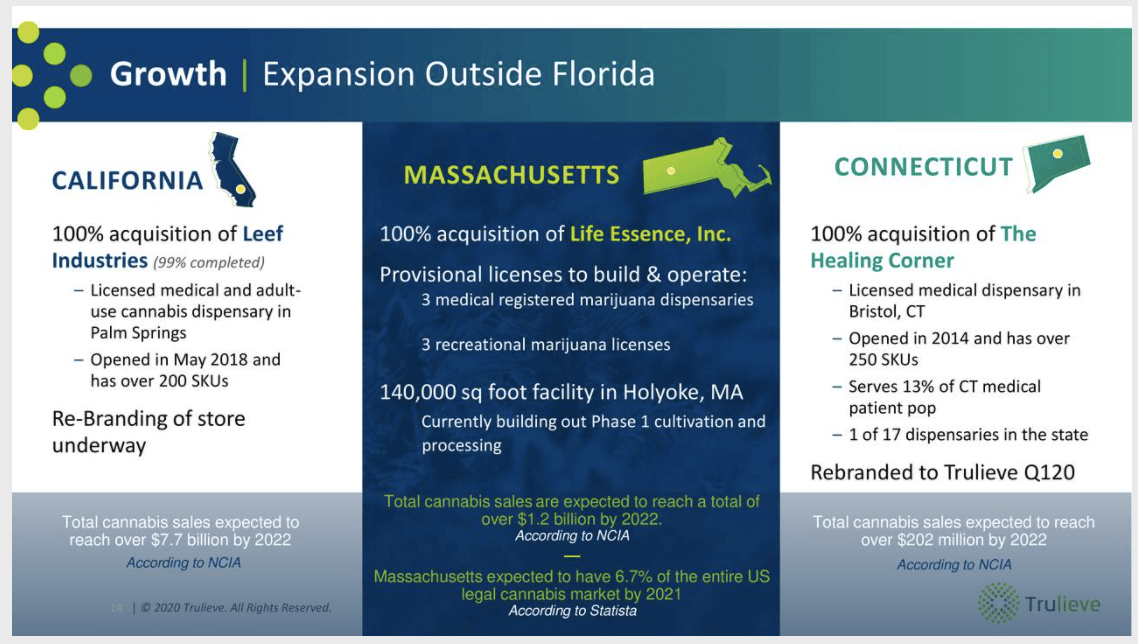

Trulieve has a quality product, a strong brand, and also operates its retail and online stores. Much of the company's success can be attributed to first-mover advantage. In 19 out of 29 municipalities in Florida, Trulieve was the first dispensary to open. Now, the company must be able to repeat this success in other states. Trulieve now has its sights set on California, Massachusetts, Connecticut, and more recently Pennsylvania.

Trulieve has been very active in the M&A space, using cash and equity to expand and absorb other companies. The Leef Industries and Massachusetts acquisitions date back to the end of 2018. As mentioned above, both Massachusetts and California are high growth areas in the domestic cannabis space. Combined, these acquisitions should generate just under $9 billion in sales by 2022. More recently, the company acquired The Healing Corner, which was only rebranded in the first quarter of this year.

Lastly, and most recently, the company has expanded its reach to Pennsylvania by acquiring Solevo and Prepenn for a combined $39 million in cash and $37 million in stock. This acquisition also stipulates earn-out potential payments of $104 million, which is 4.6x EBITDA minus the upfront payments. With this acquisition, Trulieve has gained another 3 operational dispensaries and an added 13 million potential customers.

This aggressive expansion has come with some strings attached, in the form of $130 million in long-term debt. However, I find Trulieve's M&A strategy successful for two reasons. Firstly, because the company has always bought businesses outright, and secondly, the 50% cash/equity exchange with the added earn our potential payments seems like a great way of assuring success while reducing risk.

Comparative Analysis

Unlike many of its competitors, Trulieve has a reasonably strong financial position, is profitable, and has a well laid out plan for growth with a proven track record. But despite the stock price more than doubling, I still find Trulieve to be undervalued compared to some of its peers:

TCNNF | GTBIF | CURLF | |

EV/EBITDA (TTM) | 11.29 | 52.65 | 66.79 |

Price to Book (TTM) | 7.77 | 3.92 | 6.87 |

Price/Cash Flow (TTM) | 33.87 | 71.62 | 1,145.34 |

Price/Sales (TTM) | 6.54 | 8.99 | 12.32 |

The chart above shows valuation metrics for Trulieve, Green Thumb, and Curaleaf Holdings, Inc. (OTCPK:CURLF). For the most part, the cannabis sector is comprised of more speculative, high growth "money-losing" companies, but the above have managed to turn a profit in the most recent quarters. This is already a reason why I was attracted to Trulieve, as it is one of the few value plays available in the space. Even when compared to other profitable competitors, the company offers the best value in terms of P/S and price/cash flow.

Risks

Despite the fabulous growth and valuation, the company and sector still face significant challenges ahead. Cannabis consumption, even for medical purposes, remains a hot-button issue. The problems for the future go well beyond full-on illegalization. Most likely, the industry will be forced to undergo stricter regulations and government control, which could put a dampener on profits.

In the case of Trulieve, specifically, the company now has a considerable amount of debt to repay. While its M&A strategy has worked so far, it remains to be seen how the latest acquisitions in Pennsylvania will pan out. Furthermore, growth will inevitably slow-down, as its most profitable markets become saturated, and this is something investors must account for.

Takeaway

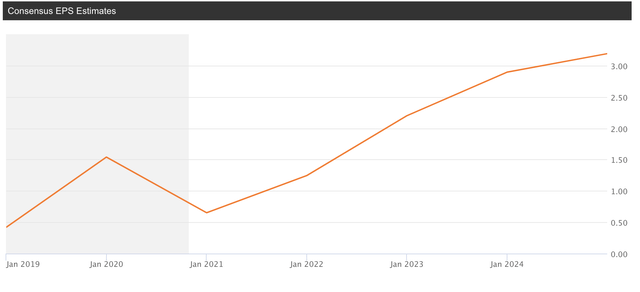

Trulieve is, in my humble opinion, the best value play in the U.S. cannabis sector today. A rare find in a sector filled with duds and zombie companies. Trulieve has managed to achieve growth without giving up profitability and sound finances. The company has some great years ahead of it, and the valuation still does not reflect all the potential this business has. According to legendary investor Peter Lynch, a company will be fairly valued when its growth rate is equal to its P/E. A company that is growing 15% should have a P/E of 15. In other words, a well-valued company should have a PEG of 1. In the case of Trulieve, here are the consensus EPS estimates:

If we are to believe the analysts, Trulieve should reach $1.24 EPS by the end of 2021, which represents a 90.77% increase from 2020, at $0.65. Currently, Trulieve trades at around a 0.5 PEG ratio. For this to reach a "fair value" as proposed by this method, the price would have to double. Having said this, the current sector average PEG is 0.82, according to Seeking Alpha. Therefore, we could expect a range of appreciation anywhere between 60% and 100% based solely on multiple expansion. The bottom of the range represents a move towards the industry average and the top of the range would indicate "fair value" as proposed by Peter Lynch's valuation method.

However, even if the PEG were to remain at 0.5, maybe because the company is still in its early stages of development and investors are accounting for this, we should still see the price stock double if the EPS reaches the estimates. Price would be equal to 90.77, growth rate, multiplied by 0.5, PEG, and 1.24 which is the EPS. Put more simply, we could see the stock trade at a P/E of 45. This would give us a target price of around $56/share by the end of the fiscal year 2021.