Highlights

A core business of extraction, testing, formulation, product development and manufacturing will enable The Valens Company (TSX:VLNS, OTCQX:VLNCF) to achieve and sustain leadership in Cannabis 2.0. Capabilities and expertise create a moat around the business. Risk management and financial discipline around supply chain enable profitability in Cannabis 2.0. Profitable and net cash positive company in a nascent and growing billion-dollar worldwide market. 136% upside based on applying a Pharmaceutical Contract Manufacturing multiple to FY2020 Adjusted EBITDA estimates.

Introduction

We believe The Valens Company (TSX:VLNS, OTCQX:VLNCF) will emerge as a leader in Cannabis 2.0. With extraction, testing, formulation, product development and manufacturing as their core business; this picks and shovels play is well-positioned to control key aspects to the supply chain to avoid the burdens of commoditization. We see opportunity in both scalable growth and unlimited option value. Our thesis is based on a comprehensive understanding of the cannabis industry, as well as our belief in the fundamental operating economics of VLNS. Trading at just 4.6 times FY2020 estimated Adjusted EBITDA of CAD$54.9 million VLNS offers investors 136% upside to our target price of CAD$5.91.

The Hype Cycle of Cannabis 1.0

Watching the cannabis market unfold it’s hard not to draw some parallels to past hype cycles. Changes in public perception, as well as national and local legislation led to a flood of investments and a swell of expectations. Like most hype cycles early investors into cannabis initially profited handsomely; however, expectations in the capital markets for licensed producers (LPs) outpaced reality. The peak in expectations of LPs, and in cannabis equities in general, coincided with the Federal legalization in Canada. Overinvestment in cultivation led quickly to commoditization of flower. As a result, revenues for the large LPs proved to be significantly lower than expectations. The air was let out of the tires; and, cannabis stocks crashed back to earth with the Horizon’s Marijuana Life Science ETF (TSX: HMMJ) dropping 65% from Oct 16, 2018 to June 2, 2020.

As the dust settles, we find ourselves in the “Trough of Disillusionment” phase of the hype cycle where “get rich quick” investors have thrown in the towel and moved on to the next big thing. Despite all the negative press, this is good news for investors looking to enter what still is a growing industry. The sell-off in cannabis exposed equities has been broad based; and, there are certain companies that are the proverbial “baby thrown out with the bathwater”. As the market evolves into the “Slope of Enlightenment” phase of the hype cycle, now is the opportune time to invest in a different set of companies. We think it is unwise to play Cannabis using the Cannabis 1.0 playbook by investing in acreage and dispensaries. Instead we are setting our sights on the next phase of the Cannabis 2.0 lifecycle.

Cannabis 2.0 Products

So, what is Cannabis 2.0? A core driver of our thesis is the evolution of the cannabis product. In Cannabis 1.0, the end-product was typically the cannabis flower or simple extract. The next phase, Cannabis 2.0 is characterized by second generation cannabinoid products and services within defined regulatory frameworks like Health Canada, the FDA, and the USDA. We believe that cannabinoids will pass through a regulatory process, like the already well-established pharma process, as cannabis derivatives develop into intermediate ingredients and/or final products. Compliant R&D, manufacturing, and commercialization operations will create a moat and translate to protectible margins. With additional requirements for cannabis handling, we believe moderate barriers to entry exist and these will also translate to better margins for brands based on sourcing from validated suppliers. Regulatory environments are updating their requirements to enable compliant participation in these markets; and consequently, a protectable higher margin is created.

Why Extractors and Contract Manufacturing Organizations (CMO)?

The first generation of products were dominated by the stereotypical uses of flower. However, as the industry matures, and the customer becomes more sophisticated; we expect the product will evolve in kind. We expect in Cannabis 2.0 for the portfolio to be made up of familiar everyday products infused with a cannabinoid such as CBD. The graphic below with data compiled by Cowen Research and the Valens Company shows how the evolution of the market may look like. In 2016, 71% of Cannabis consumed was in the form of a flower-based product. By 2018 that had dropped to just 53% and expectations are that in the future flower-based products may represent just 25% of cannabis consumption.

The development of derivative products should be a welcome transformation for the industry as flower encounters commoditization headwinds. Cannabis 2.0 products will drive demand for extraction capabilities and corresponding capacity. The building and operating of this infrastructure type within a matrix of regulations is difficult and creates a moatable business once scale is achieved. Taken together, a need for a vertically integrated, transparent, multifaceted, and compliant supply chain emerges. Companies with capabilities to operate successfully in these segments of the industry are also well positioned for control of B2B white label given preferred sourcing status, with inherent margins based on that trusted sourcing.

In the beginning, the thought was that the LPs would be fully integrated owning the entire supply chain. The first phase of growth and investment was in cultivation. In Cannabis 1.0, with the flower as the end product, the demand for extraction was limited. The commoditization of the flower has resulted in margins for LPs to be a fraction of what was anticipated. This has also led to capital available for investment in subsequent phases for the verticalization of the supply chain to virtually dry up for them. As a result, the demand for outsourcing extraction and manufacturing capabilities to third parties has become the norm and will only increase from here as derivative products take share from flower. The evolution of the supply chain will look very similar to what we see in the pharmaceutical industry where the bulk of the manufacturing is done by Contract Manufacturing Organizations (CMOs).

As the Cannabis industry evolves, we see the middle of the supply chain being dominated by Cannabis CMOs (C-CMOs) who will provide not only extraction capabilities but also purification, formulation, and product manufacturing. The technical and regulatory business requirements are comparable to that of the CMOs found in pharmaceuticals, nutraceuticals, cosmeceuticals, nutritionals and specialty foods; therefore, the economics including the capital requirements are also similar where managing scale and diversity are critical to maintaining operating margins. As the drug development landscape became more complicated, the industry needed more flexibility to separate the various segments and therapeutic areas. At times, certain areas were underutilized; thereby eroding margins. LPs are experiencing this now as they control a single type of supply chain to a single type of product, flower.

CMOs can better maintain utilization of their capabilities by servicing multiple contracts with multiple firms across a wider range of products. Pharmaceutical firms see favorable economics to engage CMOs that can run multiple various production lines instead of maintaining this capability in house. The best performing CMOs manage risk by providing services with flexible capabilities to a portfolio of clients in various therapeutic areas. Given the demanding requirements in a heavily regulated industry, a stickiness develops from the reliance on trusted sourcing and transparency.

These merits of this model have also created value in nutraceuticals, cosmeceuticals, nutritionals, specialty foods, and more. The CMO model has also given rise to the white label industry where the CMO manufactures a product according to the specifications of a client. Note, this is slightly different from the pharmaceutical CMO with an emphasis on R&D and formulation. In the pharma only CMO, the R&D and formulation are more tightly controlled by the client. The white label industry has more branding flexibility.

With the same analyses, the cannabis industry will also rationalize the services of the C-CMO. Similar to how the pharmaceutical industry has evolved to rely on the efficiencies enabled by CMOs across multiple indications and dosage forms, the cannabis industry will need C-CMOs to provide extraction, purification, formulation, and manufacturing capabilities at flexible scale for the full range of cannabis product types.

We believe that VLNS is best positioned to be the best of breed C-CMO based on its strategic approach, technical capabilities, and operating discipline. VLNS has committed to a selective process of engaging clients as it grows into the white label industry. It has the widest range of capabilities enabling contracts with a diverse client portfolio. Most importantly, it is a well-run company having a conservative management team leading an organization of highly skilled professionals rarely found in the cannabis industry. This process surety, including compliance, drives an even stronger stickiness akin to the pharma CMOs.

Extraction Capabilities a Differentiator

A constraint, arguably failure, in Cannabis 1.0 that has been carried over is the one-dimensional scale-up. To date, the common understanding of extraction is limited to converting biomass into oil. As the demand for more complicated products increases, the need for more specialized extraction methods also increases. While there is overlap, different methods enable formulation for different product requirements at varying cost structures. Subsequently, cannabis economies of scale are multidimensional. Companies in this area have been focused on operational efficiency first and capability second. Instead, the right capabilities should be decided upon first. Only after which, should implementation of an efficient model take place given the complexity of set up and calibration of formulation for any given product.

To that end, VLNS has five different extraction methods where the competitors in this space typically have one or two. The graphic below illustrates the range of extraction capabilities that VLNS offers. This diversity enables multiple different supply chains to brand Consumer Packaged Goods (NYSE:CPG) companies with various product requirements. As larger CPG companies look to enter the cannabis space, they will want to partner with a C-CMO that they can trust to produce a high-quality product and will not jeopardize the reputation of their overall brand. We believe VLNS will undoubtedly be the partner of choice. Along with the complexity of operating equipment, the skillset of personnel needed for this operation present a challenge to assemble. Yet, this level of talent exists throughout VLNS from extraction and R&D to Financial Management and Business Development capabilities.

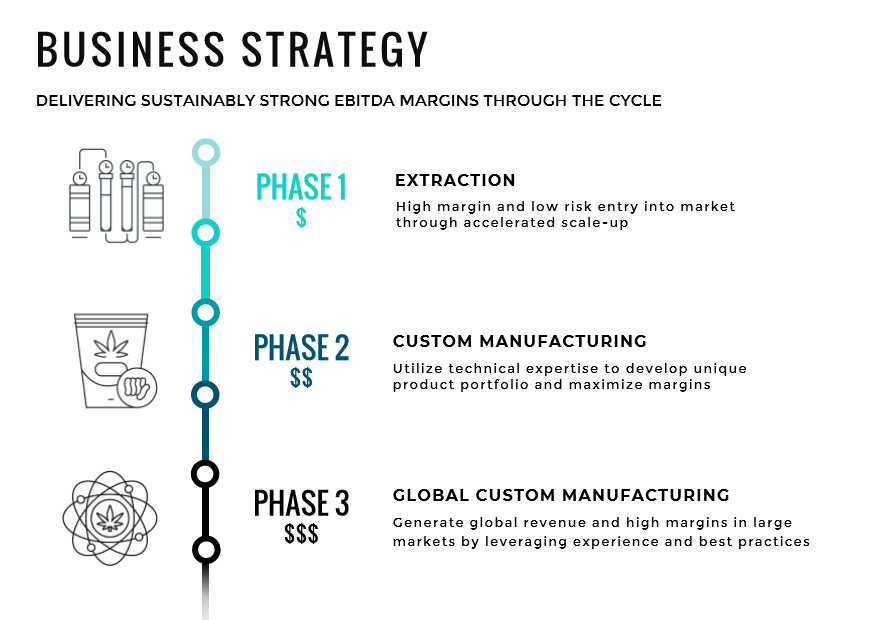

Strategic Approach

In its infancy VLNS has placed specialized extraction and manufacturing capabilities at the core of its business to capitalize on the segments and the product markets of the industry that will have the widest, most predictable margins. Note the highlighting of the segments in their most recent investor presentation. This positioning has unburdened VLNS from the capital-intensive commoditized business of cultivation and shielded it from the overcrowded consumer branding in cannabis. Instead, VLNS developed its capabilities to supply a demand with an increasingly complex product mix.

VLNS’s diversified extraction business will scale with the aggregate market having the ability to supply a wide range of oil-based product markets that are driving aggregate cannabis growth while flower-based product demand falls. VLNS has 14 extraction contracts with the following companies (note: 3 contracts have not been disclosed):

- SpeakEasy: Announced May 17, 2018, a multi-year tolling agreement with an undisclosed minimum annual contracted demand.

- GTEC (TSXV: GTEC): Announced Nov 5, 2018, a 4-year tolling agreement with an undisclosed minimum annual contracted demand.

- Harvest One (TSXV: HVT): Announced Nov 14, 2018, a 3-year tolling agreement with an undisclosed minimum annual contracted demand.

- Canopy Growth Corp (TSX: WEED): Announced December 13, 2018, a multi-year tolling agreement with an undisclosed minimum annual contracted demand.

- Sundial Growers (NASDAQ: SNDL): Announced Jan 21, 2019 a multi-year tolling agreement with an undisclosed minimum annual contracted demand.

- Organigram Holdings Inc. (TSX: OGI): Announced Jan 29, 2019 a multi-year tolling agreement with an undisclosed minimum annual contracted demand.

- Tilray Inc (NASDAQ: TLRY): Announced Feb 26, 2019 a multi-year tolling and white label agreement with initial minimum annual demand of 15,000 kg which was then amended to 60,000 kg.

- The Green Organic Dutchman (TSX: TGOD): Announced March 11, 2019 a 2-year tolling agreement with 30,000 kg and 50,000 kg in the second year.

- HEXO Corp (TSX: HEXO): Announced April 25, 2019 a 2-year tolling agreement with 30,000 kg in year 1 and 50,000 kg in year 2.

- Tantalus Labs: Announced May 28, 2019 a 2-year tolling and white label agreement with an undisclosed minimum annual contracted demand.

- Emerald Health (TSX: EMH): Announced Dec 13, 2019 a 4-year tolling and white label agreement with 10,000 kg of minimum annual contracted demand.

As the market continues to evolve so too is VLNS. The further shift to Cannabis 2.0 and the growth in derivative products is leading to a shift in the revenue mix for the company. The company is increasing its manufacturing capabilities and targeting the white label market. In essence, VLNS is manufacturing products that are then branded by other companies. So far, the company has 10 white label contracts including the following: (note that 3 contracts have not been disclosed).

- Tilray Inc (NASDAQ: TLRY): Announced Feb 26, 2019 a multi-year tolling and white label agreement.

- Tantalus Labs: Announced May 28, 2019 a 2-year tolling and white label agreement.

- Iconic Brewing: Announced Sept 12, 2019 a 5-year white label agreement with 500k beverages per year.

- Shoppers Drug Mart: Announced Sept 16, 2019 a multi-year white label agreement of gel caps, tinctures, vapes, topicals and others.

- BRNT: Announced October 30, 2019 a 2-year white label agreement to produce 1.1m vape pens per year.

- Emerald Health: Announced Dec 13, 2019 a 4-year tolling and white label agreement with the production of vapes, soft gels and tinctures.

- Dynaleo: Announced Dec 13, 2019 a 2-year white label agreement.

The transition to white label is not replacing extraction demand but building upon it. As the company grows the proportion of revenue coming from white label will increase. This transition has only accelerated due to COVID-19. In the third quarter of 2020 the company expects greater than 50% of revenue to come from white label and this should be greater than 60% by the fourth quarter. We would expect this to only grow going forward.

Market Growth

While the dramatic fall in Cannabis related equities suggests a dying industry, falling stock prices are just a sign of deflating of unrealistic expectations. In reality, the Canadian cannabis market continues to grow still represents a CAD$12.5 Billion Opportunity by 2025 according to Cowen and Company.

The shift in consumption towards derivative products will allow VLNS to benefit handsomely from this growth. In 2019 VLNS generated CAD$21 million in EBITDA. Consensus estimates are for this to grow to nearly CAD$55 million in 2020, CAD$83 million in 2021 and CAD$95 million in 2022.

Catalysts

- Adjusted EBITDA Estimates: Hitting these estimates will give credibility to the EV/EBITDA multiple used in the valuation.

- Branded Product Mix: An increase in revenue mix of branded products, with an overall total revenue and gross margin increase, will help validate their strategy of moving up the value chain.

- Bulge Bracket Canadian Bank Analyst Coverage: An initiation from a top tier analyst will expose the company to Canadian value-focused institutional investors.

- US Sell-side Analyst Coverage: An initiation by U.S. sell-side analysts will expose the company to US value-focused institutional investors.

- Investor-base Rotation: The transition of majority ownership to institutional from retail investors will help realize the intrinsic value of the company and will reduce the volatility in the stock price.

- US Legalization: Legalization will likely occur as states look for additional revenue sources to cover the tax revenue shortfall due to the COVID-19 economic shutdown.

- Major US Stock Exchange Listing: Listing onto NASDAQ or the NYSE will increase the pool size of potential institutional investors.

Valuation

Given that VLNS is currently profitable and is net cash positive, we chose to apply an Enterprise-Value-to-EBITDA (EV/EBITDA) multiple in calculating the appropriate valuation for this investment opportunity. However, before we go through the income statement focused valuation analysis, we would like to focus on a potential risk issue on their balance sheet. As we analyze their balance sheet, their Accounts Receivable (A/R) value warrants further discussion as an outsized and growing number coupled with a high Days-Sales-Outstanding (DSO) typically indicates a looming cash crunch scenario.

A/R Analysis:

As of February 29, 2020, A/R was CAD$50.24 million or 33.5% of expected FY 2020 revenue estimates of CAD$149.9 million. Of which, CAD$12.93 million or 25.7% has aged over 60 days, but while still high this is within the average collection cycle range of 30 to 90 days. The concentration of aged receivables past 60 days is due to the payment dynamic of provinces who typically pay after 60 days. Importantly, CAD$27.13 million or 54% of these receivables have been collected subsequent to the end of the first quarter, thus reducing the risk on their balance sheet. Management has acknowledged the risk concerning the level, concentration and unpredictability of their cash collections and has indicated that their customer base will be more diversified and stable as the mix of provincial retailer customers increase and their branded customers overtake their license customers in the second half of FY2020. Until then, some mitigating factors include no one customer representing more than 10% of total revenues and strict enforcement of contracting controls regarding pre-payment terms and feedstock quality control (ex. 90% of potential feedstock sources fail on excessive pesticide content tests). So, although this potential issue has seemingly been addressed, it warrants further vigilance as VLNS continues to grow revenues and more monies is used for working capital needs.

Analysts currently expect Adjusted EBITDA of CAD$54.9 million in FY2020 which management is comfortable in attaining. With a net cash position of CAD$71.42 million, shares outstanding of 129.1mm, and a FY2020 Adjusted EBITDA target of $54.9 million, VLNS is trading at a 4.6 times EV/EBITDA multiple.

As of February 29,2020:

- Net Cash and ST Investments: CAD$44.29 million

- Collected A/R Subsequent to Quarter End: CAD$27.13 million

- Fully Diluted Shares Outstanding: 129.10 million

EV/EBITDA Analysis:

- Stock Price (6/2/2020): CAD$2.50/sh

- EV: CAD$2.50 * 129.10 million - (CAD$44.29 million + CAD$27.13 million) = CAD$251.33 million

- Adjusted EBITDA Consensus Estimate: CAD$54.9 million

- EV/EBITDA = 4.6 times

EV/EBITDA Valuation:

- In calculating our target price for VLNS we apply the average EV/EBITDA multiple of our Pharmaceutical CMO comparable group of 12.6 times to consensus 2020 EBITDA estimates of CAD$54.9 million to calculate a fair value for the company at CAD$5.91 per share. This valuation represents a 136% appreciation opportunity to the closing price of CAD$2.50/sh (6/2/2020). We anticipate that this valuation will start to be realized as their branded products accelerate their introduction in the second half of this fiscal year and tolling revenues revert back from the COVID-19 related slowdown. Looking forward to FY2021, with a projected Adjusted EBITDA of CAD$82.8 million, there is upside to our price target provided the company can execute on its profitable growth plans.

Conclusions

We believe VLNS will emerge as a leader in Cannabis 2.0. With extraction, testing, formulation, product development and manufacturing as core businesses. This picks and shovels play is well-positioned to control key supply chains to avoid the burdens of commoditization. We see opportunity in both scalable growth and unlimited option value. Trading at just 4.6 times 2020 estimated EBITDA of $54.9 million VLNS offers investors 136% upside to our target of $5.91 and offers investors an ideal way to play the evolution of the cannabis market.

Risks

- Accounts Receivable conversion needs to be monitored as cashflow generation is needed to fund working capital and required to validate their business model.

- A collapse in the demand for cannabis related products will hamper profit estimates and invalidate the EV/EBITDA multiple used in our valuation.

- The failure to realize their white-label or international growth plans will also invalidate the EV/EBITDA multiple used.