This Rally Has Legs, Ride Your Winners

As I begin to write at 5 am, I see the futures slowly moving back to even. Let's think about what happened yesterday for a moment. Basically, Reuters confirmed what has been the general chatter. Phase 1 is in trouble; China thinks it has "hand" because of impeachment. Trump thinks he has "hand" because the tariffs had no effect on the consumer, and the US has a better economy. According to Trump, the US has the best economy in history. 3 months ago, this news would have slammed the stock market down 3% to 7% over a few days. Now? Well, after indexes had under a 1% dip, the indexes close down less than 0.4%. In fact, the Nasdaq's lowest level was a mere -0.12% and closed down 0.08%. Do we need any more proof that the stock market is bored with the whole trade war narrative? Loyal readers will note that I have been making this assertion for several weeks now. It is a big impetus to the melt-up, and yes, in spite of the little jiggle the first half of this week, the melt-up is alive and well.

My prediction of a Weak Start in the Week, with a strong finish, is happening

What to do? Hopefully, you selected some of my picks yesterday and started to ride them. I think a big majority of them stayed green. Look, the slogan "Buy the Dips - Sell the Rips" makes sense for a flat to meandering market. But when the stock market is in a decidedly sharp upslope, forget the dips, ride the rips. If a stock is stumbling or just going nowhere in this market, it just doesn't make sense to buy them. Again, I feel compelled to say, this article is for the traders among you. For the long-term investor, it makes sense to look for underperforming assets that have good dividends and a longer-term future. For the long-term investor, it still must feel good to know that the stock market is very healthy, and while it is approaching full valuation levels, it is not there yet. How can I make such a blanket statement? Easy, just look at the stock headlines this morning. Who decides whether equities are bargains? The ultimate reason why stock markets exist and why companies go public, to buy companies, not stocks.

Not So Fast...

Please note the above paragraph was written early this morning when the futures were moving into positive territory. The market, in my opinion, was affected by a new concern. Nancy Pelosi announced that the new NAFTA agreement will not be enacted this year. This is new news that the market needs to work through. I still think that the major indexes end in the green today, or at the very least near flat. The S&P is already back above the psychologically important 3100 level

We Have More M&A News, the Appetite for Strategic Acquisitions is Growing

The big one is the merger between Charles Schwab (NYSE:SCHW) and TD Ameritrade (NASDAQ:AMTD), but I want to start with PayPal (NASDAQ:PYPL) spending $4 Billion on Honey Sciences first. I am quoting from Techcrunch:

"What's exciting is that we can take the functionality Honey now offers - which is product discovery, price tracking, offers and loyalty - and build that into the PayPal and Venmo experiences," explains PayPal SVP of Global Consumer Products and Technology, and former Xoom CEO, John Kunze. "When Honey says they're putting money in the pockets of their customers - that's perfectly in line with what we want to do. We want to make digital commerce and financial services more affordable, easier to use, more fun and more accessible to people around the world," he says. Honey tracks sales and retailers' promo codes, as a rival to RetailMeNot and others. What makes the extension so useful is that it automatically tries all the eligible promo codes for you during checkout then selects the one that provided the most savings and applies it on your behalf. This helps shoppers feel more comfortable with their purchases and reduces shopping cart abandonment."

My Take: The article further says that Honey Sciences has been basically under the radar since its founding in 2012. Also very important to us is that the acquisition was mostly in cash. So, why am I saying this reflects on the stock market as a bullish signal? Because this is about a strategic acquisition, accessing a new segment of their target market, and they are willing to pay up REAL money. Even today, $4 BILLION smackers are not chump change. So, this acquisition - even though, this is a private company and even though it is supposed to be mostly cash, it points up to a strong appetite for acquiring companies for strategic purposes. It bodes well for M&A activity in the stock market. According to TechCrunch, Honey Science is already profitable, so those profits should flow right to the bottom line and to PYPL's PE. Right now, the market is selling off PYPL in the premarket, but I would not be surprised if PYPL closes up today. This is another factoid about public companies buying private companies the profits and revenue flow right to the stock price at its PE ratio.

Tiffany (NYSE:TIF) opens its books to LVMH (OTCPK:LVMHF). This new update on LVMH acquisition of TIF was due to LVMH raising its offer from $120 to $130 per share. That is still level is inadequate, but it is a step in the right direction. Why is this important to note ahead of the huge Schwab deal? Well, the head of LVMH is the legendary Bernard Arnault, he is known as a very disciplined buyer. He will walk away from a deal if a target has the temerity to insist on a higher price. Yet, here, he is, acquiescing to a higher offer, and yet, they are signaling that this is not the end of the negotiation. Likely, the price will likely be +140 when all said and done. So, why? Well, LVMH is under-represented in Jewelry under 10%. Jewelry is the fastest-growing luxury good. At the same time TIF, while it has run into temporary trouble, is a storied brand, and has scarcity value. TIF could benefit from LVMH product development, and comarketing. My point is, that a savvy player like Arnault is willing to pay up, he is telling us that the market is...wait for it... That's right UNDERVALUED.

Charles Schwab (SCHW) buying TD Ameritrade - This was a masterstroke 3D chess level move by SCHW. First, they nuke the entire discount brokerage business model and now, they hoover up the pieces to consolidate the market. What's left now that all these players are down to zero-commish? Aggregation of the independent registered investment advisory and wealth management services, gathering assets and offering services like margin lending, and a relationship to sell more sophisticated financial products. The market loves this deal, SCHW is up along with its target AMTD. Kudos to Mr. Schwab and his team. I suspect that consolidation in this space will continue, but there are more targets than there are aggregators, so I would not try to buy the remainders. As evidence, E*TRADE (NASDAQ:ETFC) is down significantly this morning. Get some popcorn and watch the show, don't get involved. Still, this is not a strategic type acquisition, which while less exciting than a strategic type move, it is still an important indicator that the stock market is healthy and doing its job.

Interesting Trades

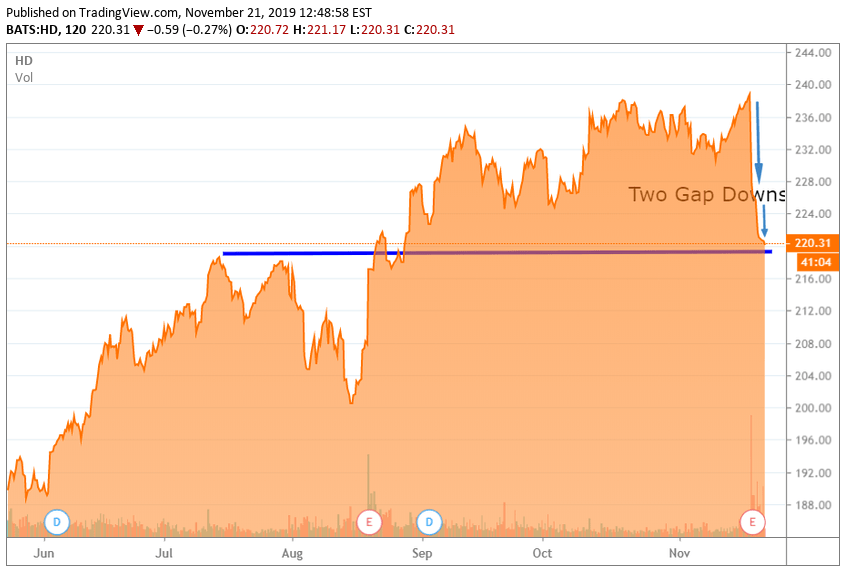

It is finally time to get long on Home Depot (NYSE:HD). If you look at the chart below, you see that that HD has very strong support at just under the current level of 220ish. Let's take look

HD was green this morning, and I expect it to close in the green today. If it doesn't and you want to employ more discipline then wait another day (I am). The chart above shows two separate down gaps. To chartist, once the momentum reverses, these gaps will draw the price up to it. This is termed as "filling the gaps", so the first stop is about 8 points of upside. For a trader that is a pretty nice risk, 2 points of downside and 8 points of upside. I expect HD to start to fill in the upper gap as well, but it may take more time to do that. If we are being strict traders, then if HD breaks below this 218 support level then stop out.

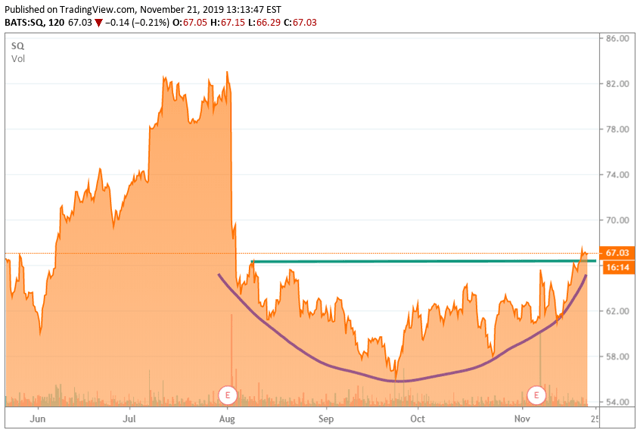

Square (NYSE:SQ) I believe that I mentioned that SQ was breaking out yesterday. I wanted to chart it for you today. Right now, SQ is flat on very high volume, and I think it closes once again in the green. I think it gets back to the '80s. This is a great company that is a small business hero.

As you can see, SQ is showing a wonderful round bottom. The green line marks out the previous high of $66.37 going back to August. This is a wonderful business that is not being priced fully.

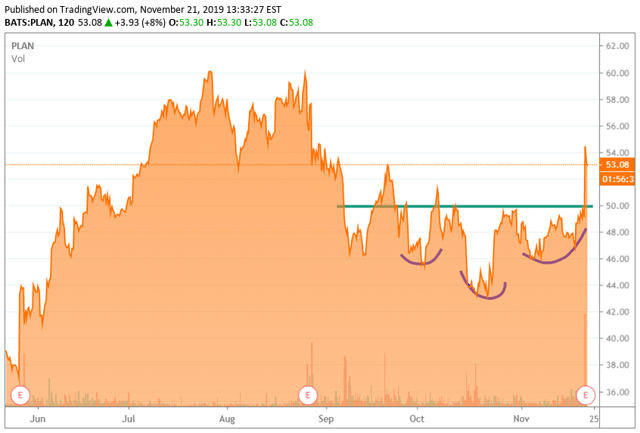

Anaplan (NYSE:PLAN) Reported today. PLAN is a member of my Social-enabled Enterprise software names. Other names on this list are Slack (WORK) and Smartsheet (SMAR). The concept is that a massive socially networked software can release huge productivity. It is kind of ironic in that the original use for social networks is such a huge time waster. In any case, PLAN beat earnings by losing only $0.08 instead of $0.12. The bigger news was that its revenue was up 44% year over year, driven by a 47% increase in subscription revenue. Subscription businesses are the holy grail for cloud software businesses. The stock was up 12%. Now, it is only up 8%. The all-time-high is $60, but I expect it to exceed old highs. This is a strong piece of enterprise software that makes middle management much more productive. Let's take a look at the chart just to make this series a "hat-trick"

The last two charts are very similar. For the last several months, high-growth names like these have not seen the usual sponsorship. Companies that stress growth over profits were temporarily out of vogue as the rally has spread out to a number of sectors. I think that market participants are returning to these names as they continue to grow good revenue in a great business model. To be frank, WeWork created a toxic atmosphere for growth companies that emphasized revenue over profits. When it blew up on the launchpad, growth names were tarred with the same brush of losing on every sale but making it up in volume. In the case of PLAN, the potential profitability will be there in spades, but also it is addressing a real business opportunity.

Analyst Corner

Have You Heard of Northland Securities? Yeah, Neither Have I

Northland Securities downgrades Advanced Micro Devices (NASDAQ:AMD) on price, their target is $36. Who the heck is Northland? Well, they have all of $95 million Assets Under Management (AUM), big whup. They are a "change lost in the couch cushions" level investment manager. They wanted to make a splash and the best way is to cut down the biggest momentum stock in the market. All they needed to do is say AMD is over-priced. They didn't need to do any special study of the market, or channel-checks, or a deep dive into the chips microcode or anything. Just some yo-yo comes up and says, "hey AMD is over-priced" and they get their name in the media. Great for them. Don't fall for it. Here is some fundamental news, just this week AMD announced a 7nm GPU, this is very advanced stuff, this is foundational tech for AI, and gaming. Yes, Nvidia (NASDAQ:NVDA) is the king of this space, but this is essentially a duopoly, and AMD is getting a nice piece of this market. This is a market space that is about to exhibit exponential growth. Is that in Northland's calculus? Doubt it.

Insider Corner

Discovery Communications (NASDAQ:DISCA) David Wargo* (Director) buys 4.5 Million in shares

My Take: John Malone buys $75 Million last week and now this. In an interview today, on CNBC, John simply said the stock is cheap, and then went on to explain that they own all their own content and they are a global content opportunity, he was animated and enthusiastic about his investment.

My trading corner

I went long on PLAN, I also went long Alteryx (NYSE:AYX), I expressed these trades as options. I also made a downside bet on Tesla (NASDAQ:TSLA), I am a TSLA bull, the cars are fantastic, and I believe that TSLA will be a very successful battery based tech company as well as a car company. That said, I wanted to express my speculation that a pick-up truck introduction is a binary event. If the pick-up is not as well-received as Musk who described it as (I believe) as "Blade Runner meets the F150" also as a "Cyberpunk truck" expects it to be, the intro could hammer the stock sharply. Also, TSLA is a very volatile name, and either it is going up, or it's on its way down. Staying in one place is usually a very temporary way-station to the downside. So, I found a very inexpensive PUT option that expires December 20. That is enough time to create a premium on a sharp down move. My strike is so out of the money that a score of contracts amounted to no more than $150. I don't want to give exact details, because I really don't want to encourage such lunacy in my readers. This is very risky and likely not to work. I made a resolution to tell you exactly what I am doing in this account. I want to show that you can express such notions with a very tiny risk. If the stock does fall 50 points in a few days, then I will make a few hundred bucks, most likely I will lose it all. I will do this from time to time, and let you know. That is not an invitation for you to imitate me.