Due to reader requests, I've decided to break up my weekly "Best Dividend Stocks To Buy This Week" series into two parts.

One will be the weekly watchlist article (with the best ideas for new money at any given time). The other will be a portfolio update.

To also make those more digestible, I'm breaking out the intro for the weekly series into a revised introduction and reference article on the 3 rules for using margin safely and profitably (which will no longer be included in those future articles).

Why Valuation ALWAYS Matters

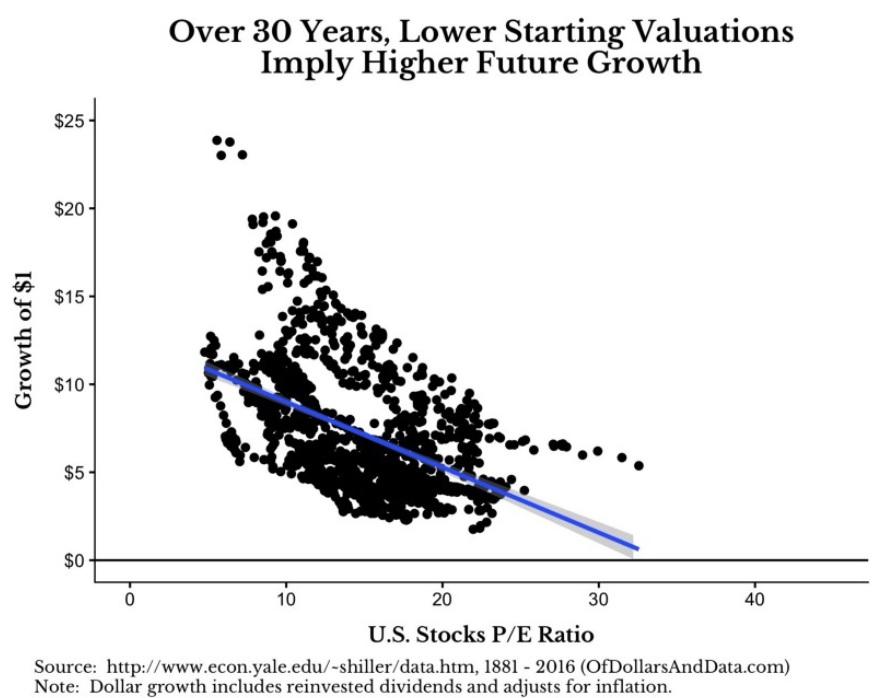

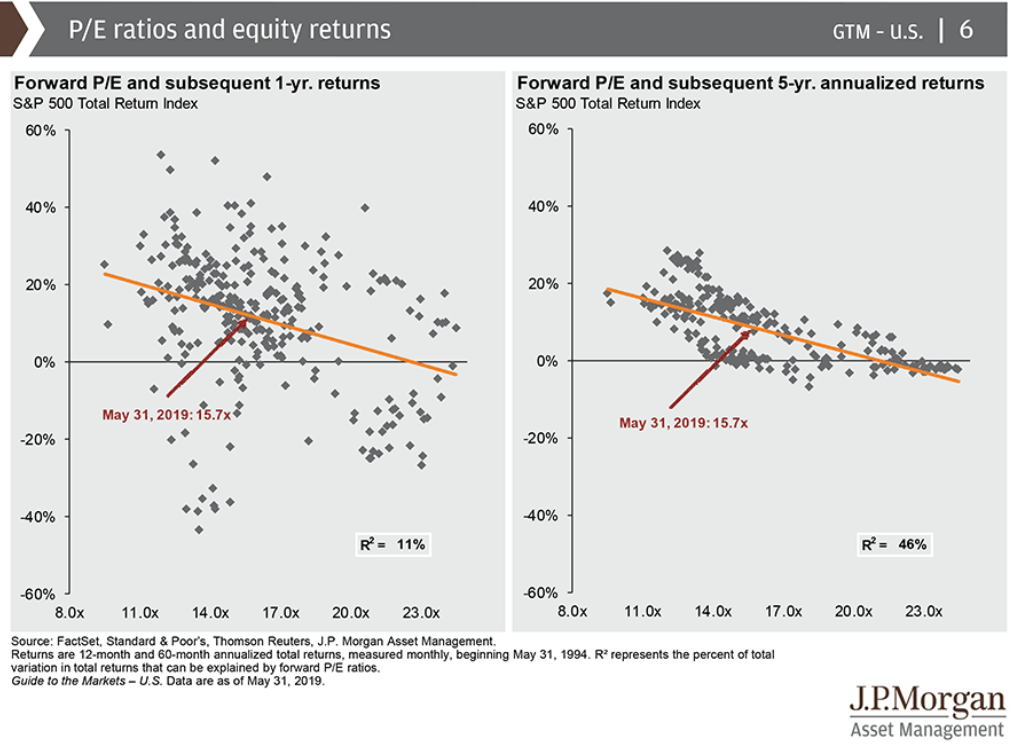

Even the best companies can make terrible investments if you overpay. A Yale study looking at market returns from 1881 to 2016 found that starting P/E ratio had a significant effect on total returns out to 30 years. What's more, in the past few decades, valuation has explained about 46% of the market's forward 5-year returns. Note that 1-year returns have little correlation to valuations because they are driven by volatile and often irrational short-term sentiment.

In other words, buy-and-hold investors can't just blindly buy great companies at any price but need to remember Buffett's famous quote, "It's far better to buy a wonderful company at a fair price than a fair company at a wonderful price."

The corollary to that quote is what I call "the Buffett rule," which is to never pay more than fair value for even the highest-quality companies. Doing so will lower your total returns, and since something great is always on sale, there is no reason to jump the gun on buying quality, low-risk dividend stocks.

After all, patience is the ultimate virtue of the long-term investor, because as Buffett also said, "the stock market is designed to transfer money from the active to the patient."

But there's another reason why valuation is always worth keeping in mind.

Value investing is one of the proven "alpha factors" that consistently beat the market over time. Of course, value investing doesn't work all of the time - no investing strategy does.

Probability Of The Strategy Underperforming The S&P 500 Over Rolling Time Periods

But it's precisely because all investing strategies go through periods of underperformance that alpha factors keep working over decades. Some of Peter Lynch's best long-term investments didn't even break even for four years. If any single approach could guarantee market-beating returns year in and year out, then everyone in the world would use it, and thus, the strategy would lose its edge.

Okay, so maybe value investing is great, and valuation is worth keeping in mind before buying any stock. But how does one find great companies trading at Buffett's mythical "fair value." Well, there are many approaches, but I personally consider four of the most useful for long-term dividend growth investors.

Using these four valuation methods can tell us what are the best quality dividend growth stocks to buy at any given time, no matter how overvalued the broader market may become.

Discounted Cash Flow

Fundamentally, any company is worth the present value of all its future cash flow. That's as basic a valuation method as you can get. However, in reality, the future is uncertain, and the discount rate you use, as well as your growth assumptions, can make a DCF model say pretty much anything you want.

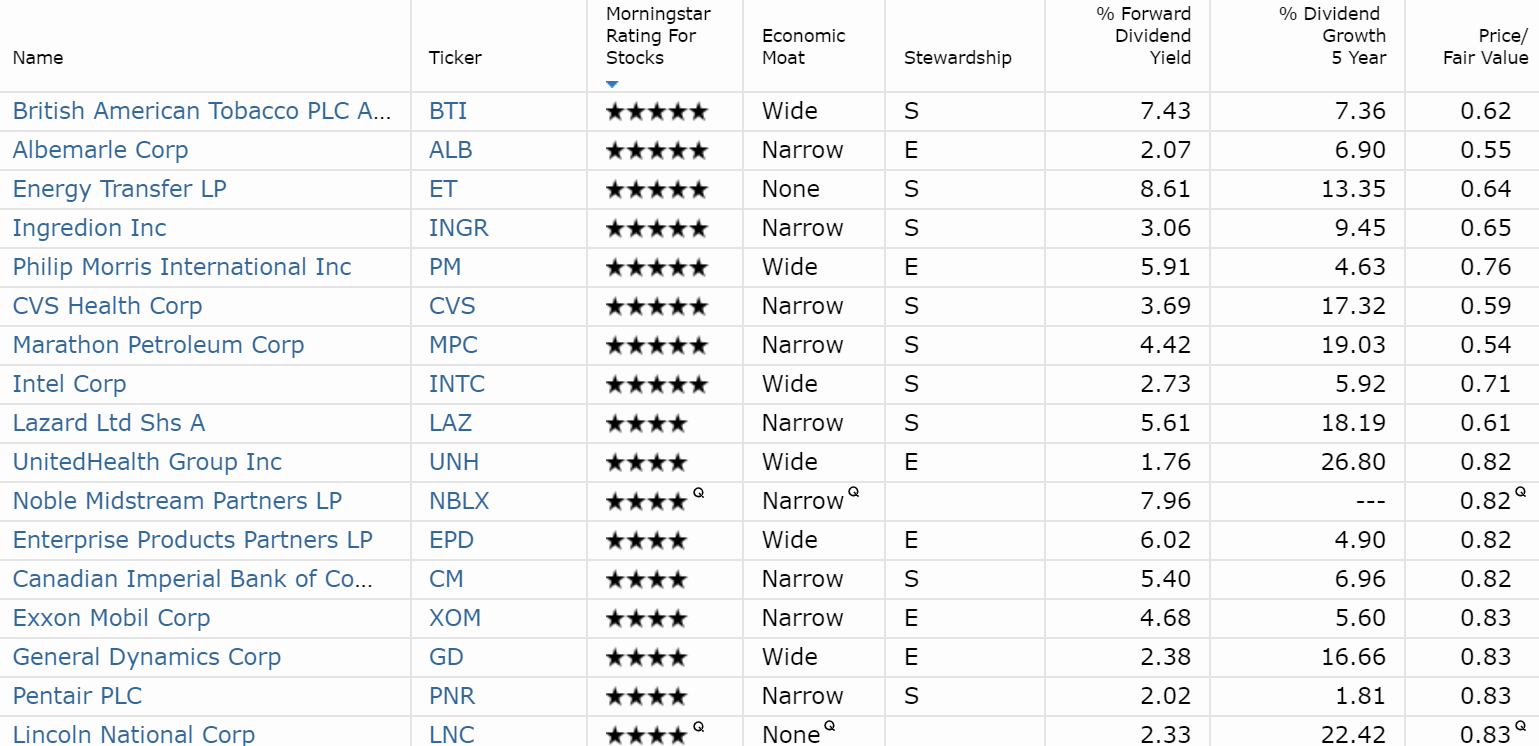

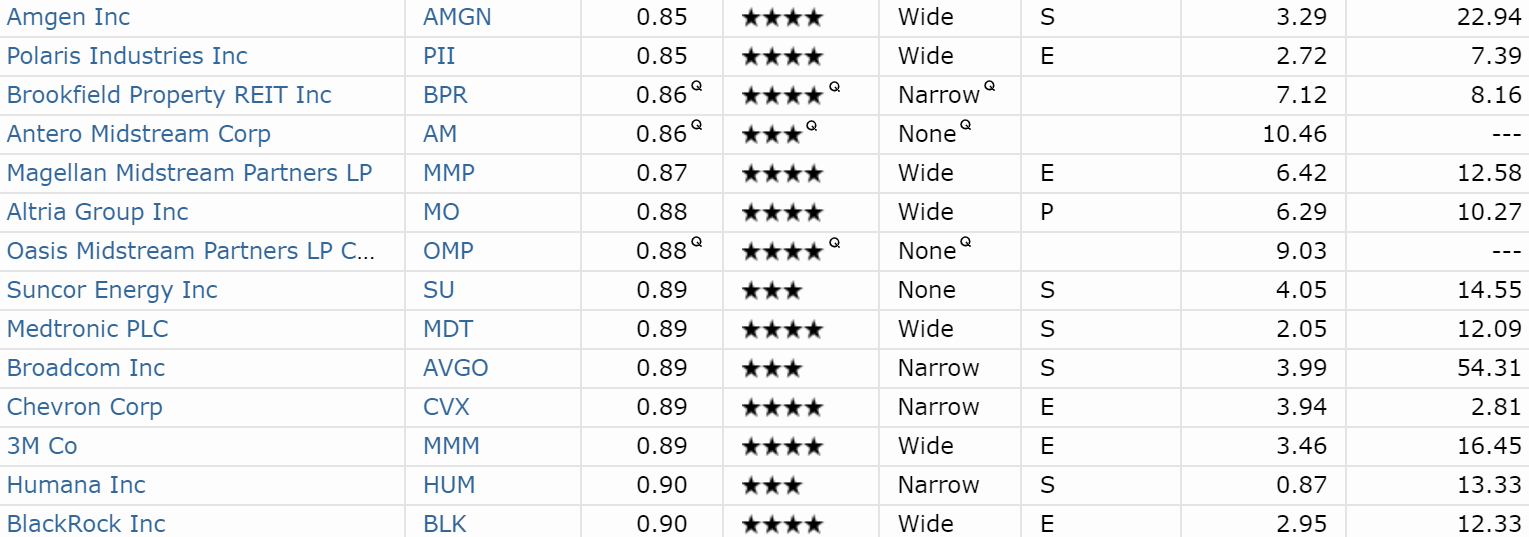

This is why I consider Morningstar's 100% long-term, fundamentals-driven and conservative analysts to be a great source of DCF estimated fair values. Here are my watchlist blue-chips that Morningstar considers 5 star (very strong buys) and 4 stars (strong buys).

Those analysts generally assume slower growth than the analyst consensus and even sometimes management itself. They also take into account the uncertainty surrounding a company's business model/risk profile. Thus, 4- and 5-star rated companies offer a comprehensive margin of safety that potentially makes them good investments.

Note that the "Q" rated companies are quantitative models and slightly less reliable.

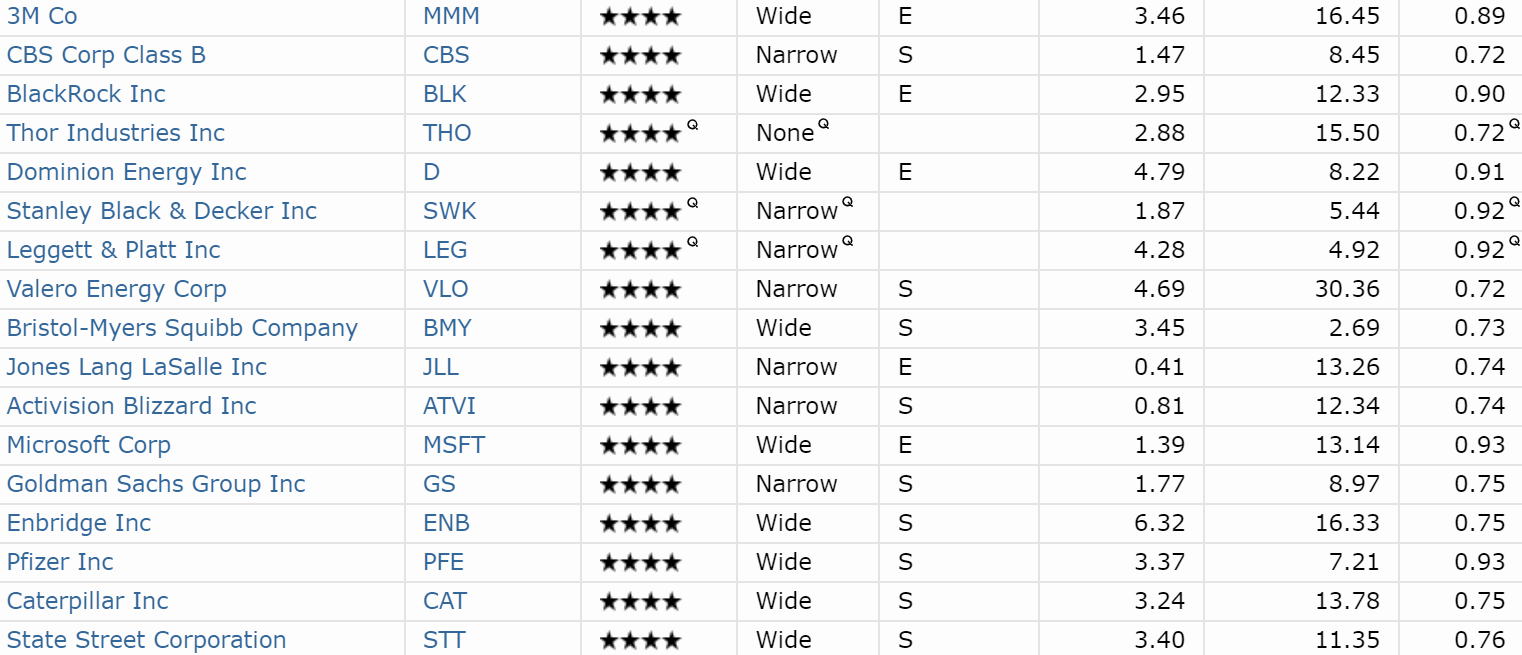

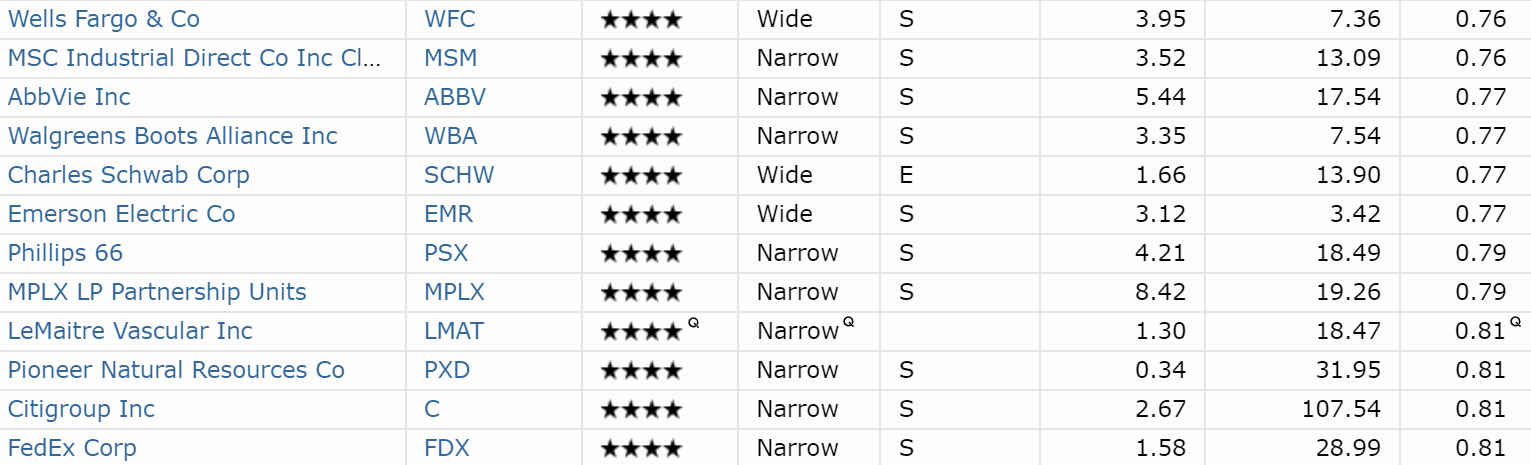

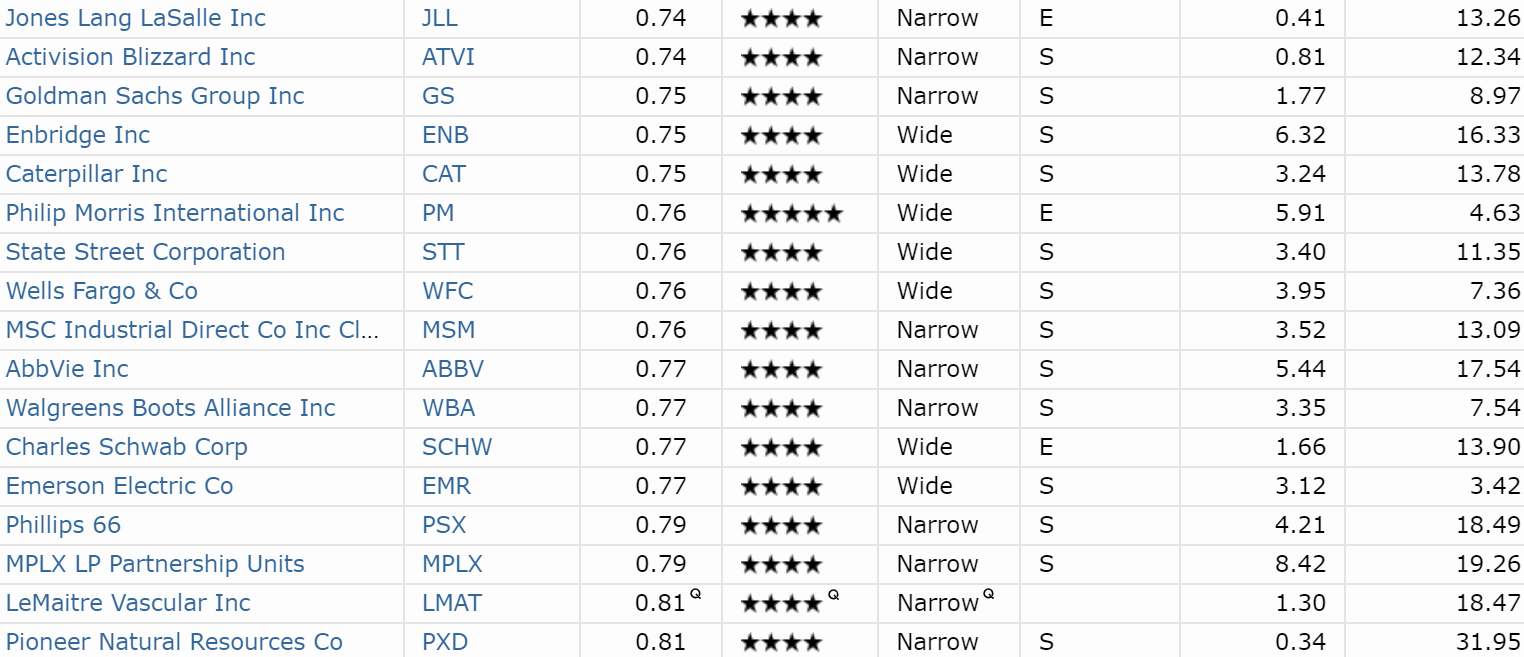

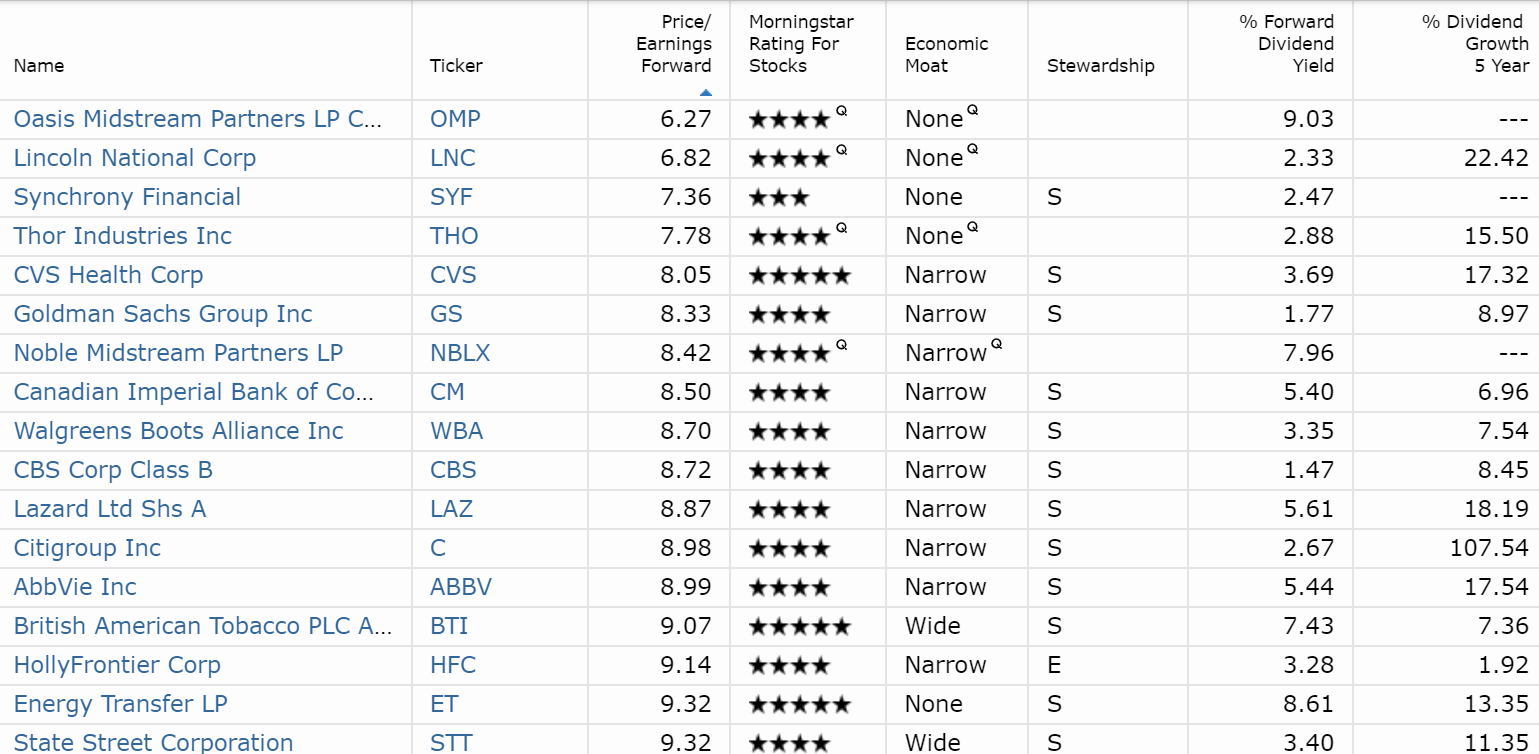

Want a more quantitative approach to DCF? Well, here are my watchlist stocks ranked by price/fair value, with each company at least 10% undervalued per Morningstar's intrinsic value estimate.

The lower the price/fair value estimate, the larger the margin of safety for investing.

But DCF is far from the only valuation method you should consider.

Price-To-Earnings

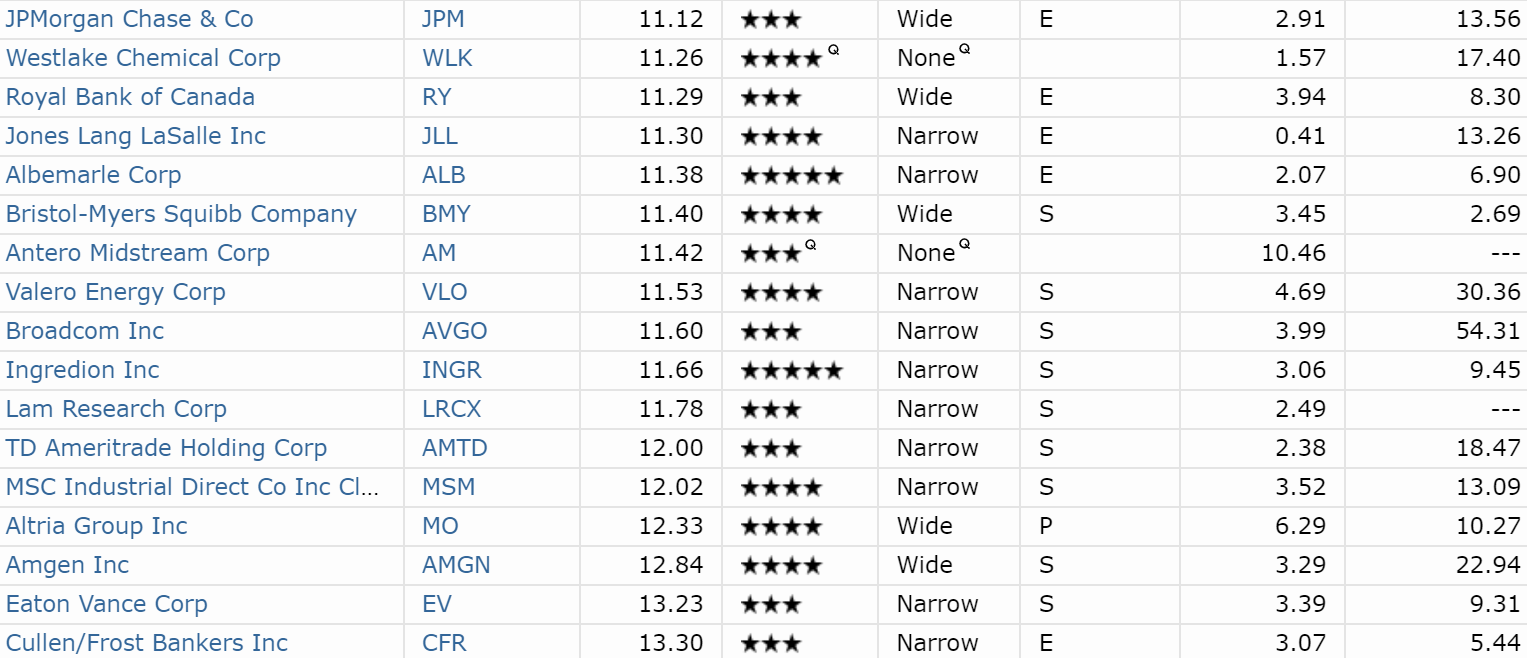

Remember that Yale valuation study that looked at stocks based on P/E ratio? Well, the venerable P/E ratio is one of the most popular valuation approaches, and for good reason. While no valuation method is perfect, a good rule of thumb (from Chuck Carnevale, the SA king of value investing and founder of F.A.S.T. Graphs) is to try not to pay more than 15 times forward earnings for a company. Chuck's historical PE valuation approach has made him a legend on Seeking Alpha and, according to TipRanks, one of the best analysts in the country when it comes to making investors money.

Chuck usually compares companies to their historical P/E ratios, and he's ranked in the top 1.4% of all analysts tracked by TipRanks (based on the forward 12-month total returns of his recommendations). While 12 months is hardly "long term," the point is that Mr. Carnevale is a fantastic value investing analyst and his historical valuation-driven approach is beating 98.6% of all bloggers/analysts, including 5,300 that work on Wall Street.

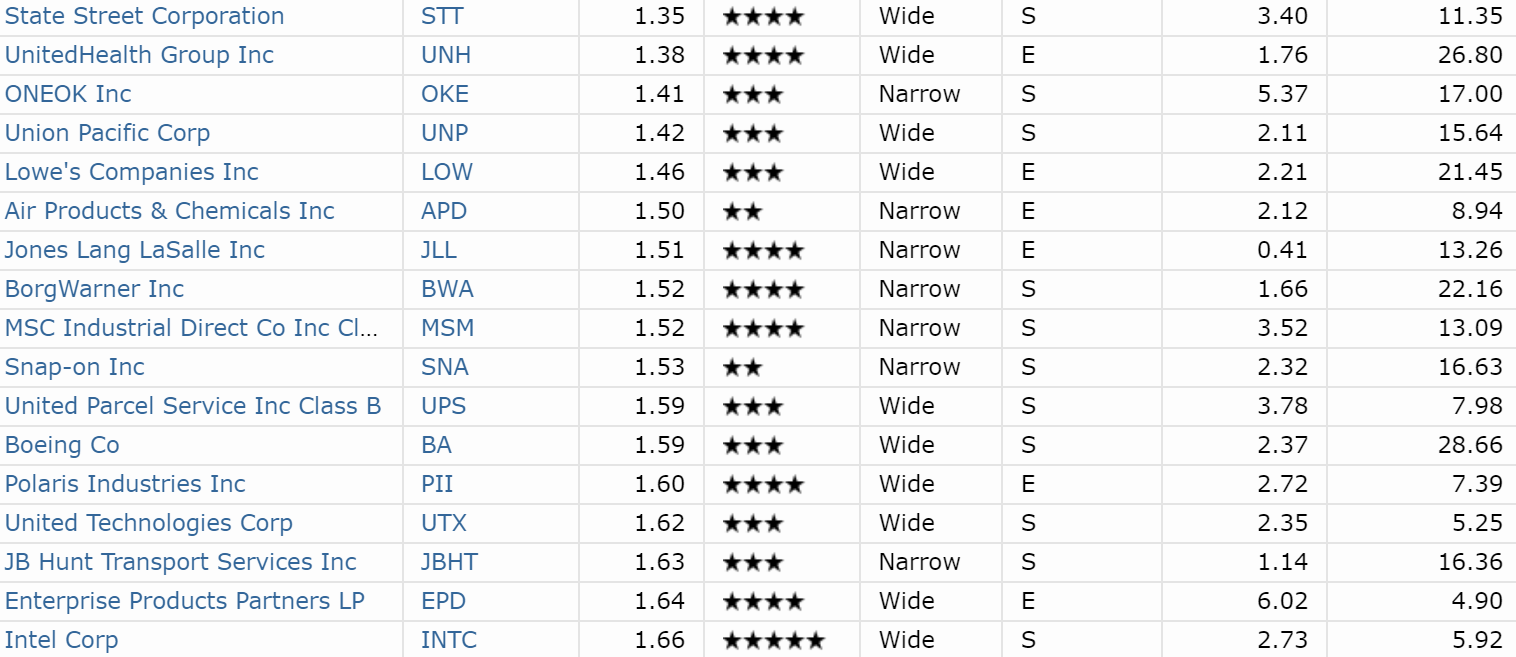

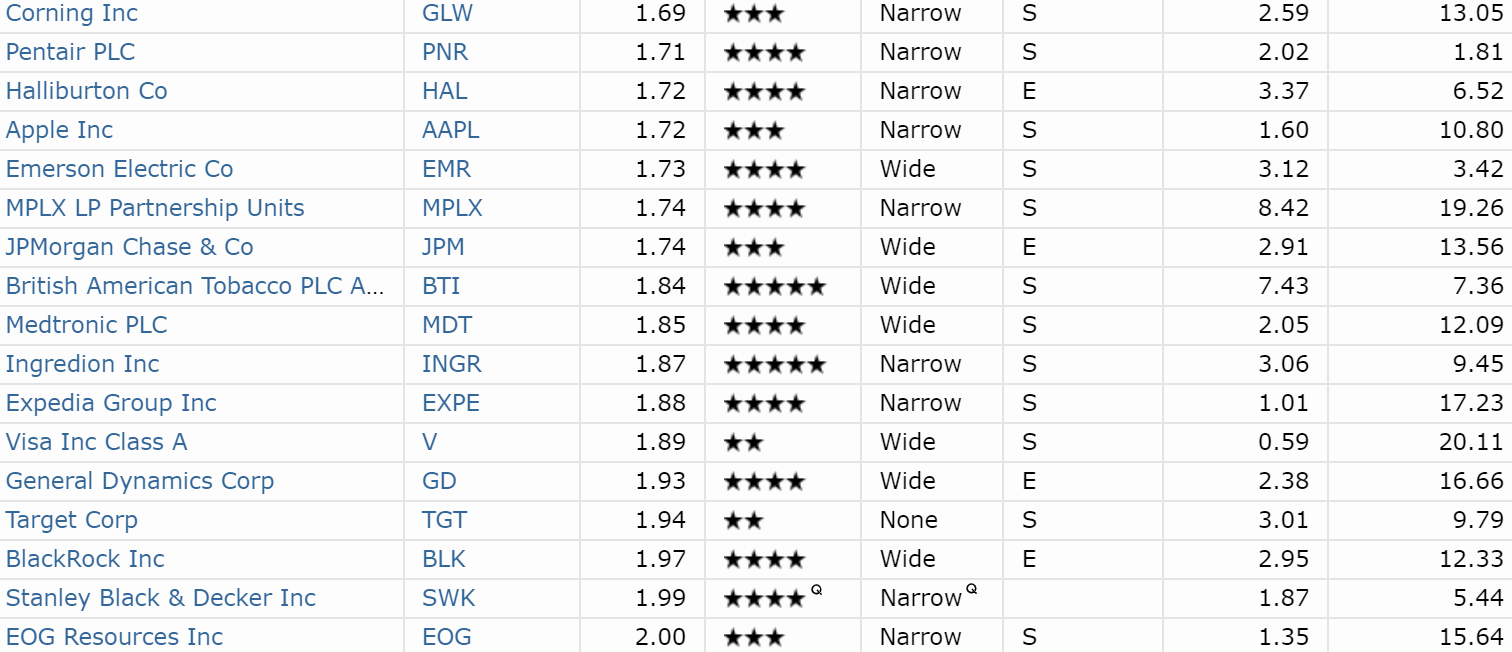

Here are dozens of companies with forward P/Es of 15 or less.

Note that stewardship rating is Morningstar's estimate of the quality of the management team. P = poor (my policy to avoid all such companies if I agree with Morningstar's assessment, which I don't on Altria (NYSE:MO)), S = standard (average to good), and E = exemplary (very good to excellent).

Price-To-Earnings/Growth (PEG) Ratio

A low PE ratio might not necessarily mean a company is a great buy. For one thing cyclical companies can have highly volatile earnings which is why they tend to trade at lower multiples than more stable sectors. Another thing to consider is the long-term growth rate. A company with zero long-term growth potential deserves to have a PE of 7.9 (according to a formula developed by Benjamin Graham, Buffett's mentor and the father of value investing).

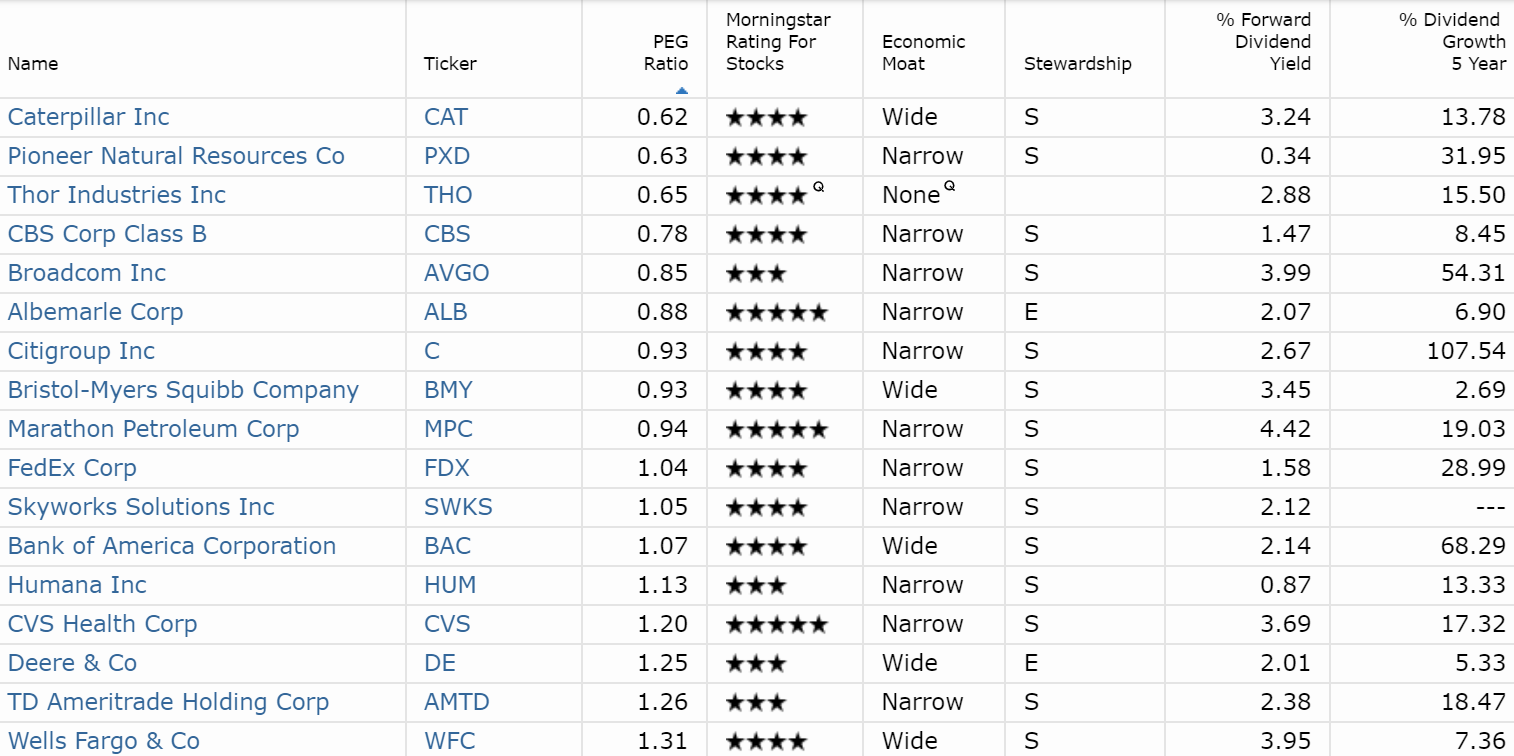

That's why another popular valuation metric is the PEG ratio, which divides the PE ratio by the expected long-term growth rate. A PEG ratio of 1.0 to 3.0 is usually a good rule of thumb, depending on the quality of the company, how stable its growth has been over time, and the sector (REITs, for example, are a slow-growing sector with naturally higher PEGs).

But in general, the lower the PEG ratio, the more likely you are to be getting a good value. The S&P 500's PEG (forward PE/long-term expected EPS growth) is currently 16.5/6.1% = 2.7. Here are my watchlist stocks with PEG ratios of 2.0 or less.

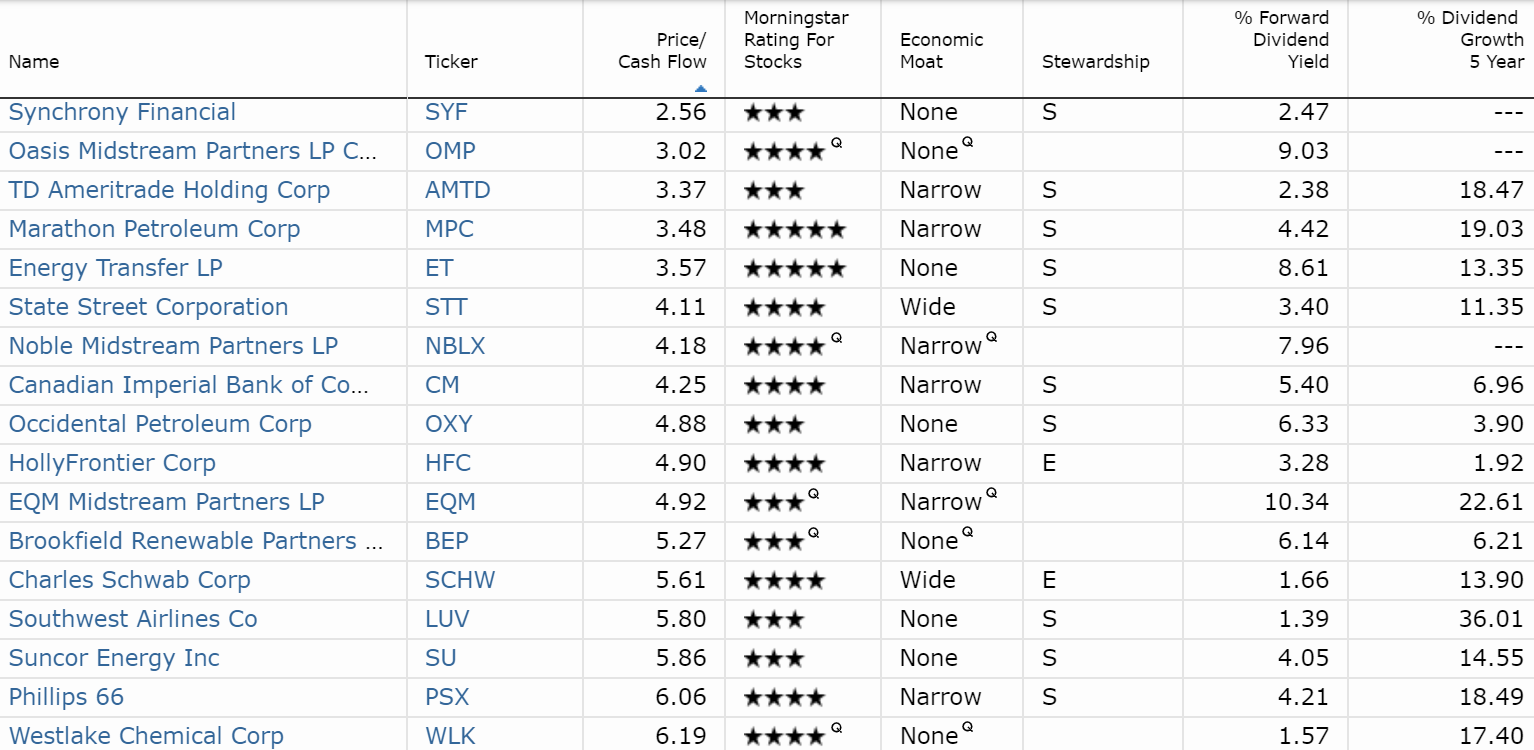

Price/Cash Flow

While earnings are usually what Wall Street obsesses over, it's actually cash flow that companies run on, and use to pay a dividend, repurchase shares and pay down debt. Thus, the price/cash flow ratio can be considered a similar metric to the PE ratio, but a more accurate representation of a company's value. Chuck Carnevale also considers a 15.0 or smaller price/cash flow ratio to be a good rule of thumb for buying quality companies at a fair price. Buying a quality company at a single-digit cash flow multiple is a very high probability long-term strategy.

Here are all the companies in my watchlist with single-digit price/operating cash flow ratios.

Blue-Chips Near 52-Week (Or 5-Year) Lows, aka "Fat Pitch Blue-Chips"

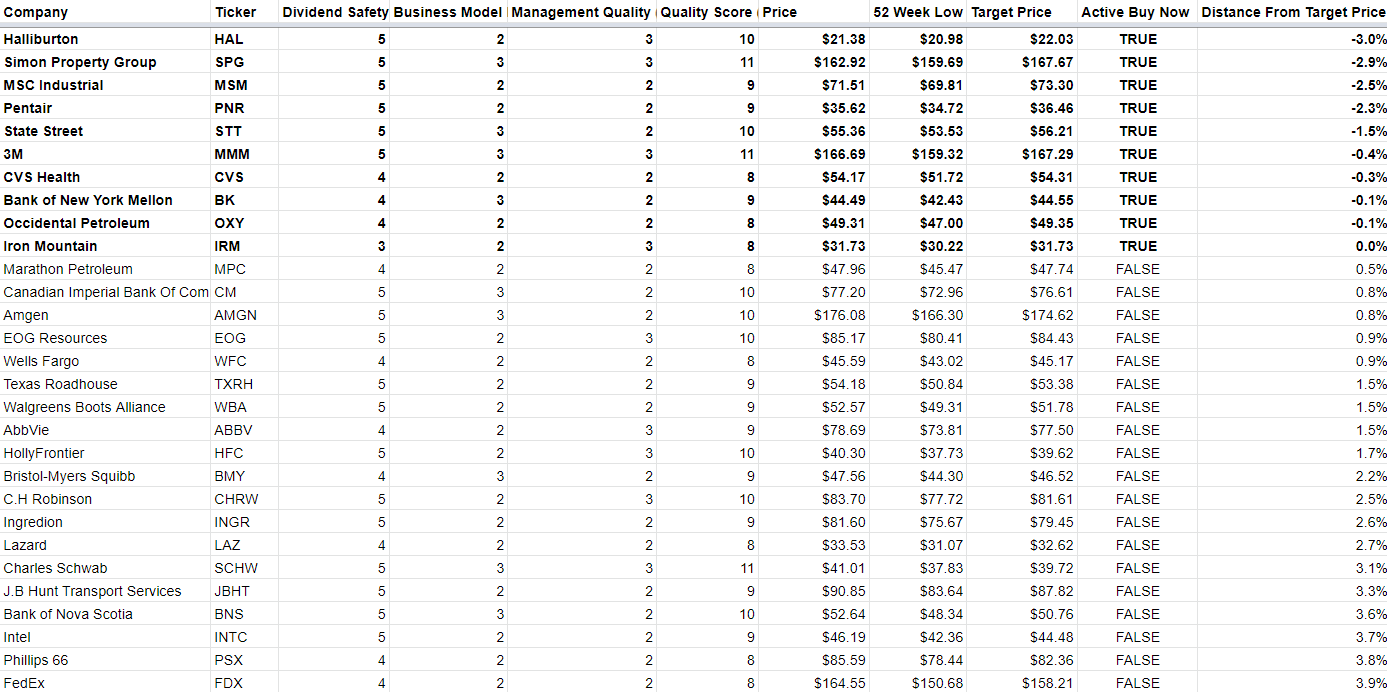

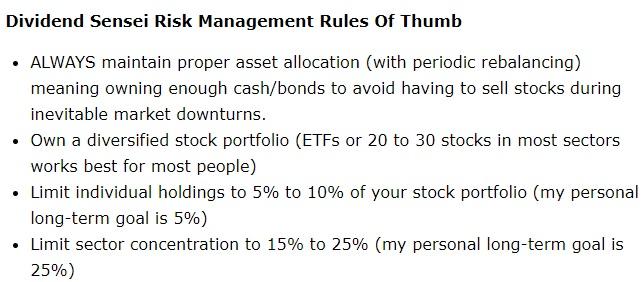

I maintain a watchlist that takes every company I track and applies an 11-point quality score based on dividend safety, the business model, and management quality. All dividend stocks can be ranked 3-11, and my watchlist (189 companies and growing slowly over time) only includes those with quality scores of 8 and higher.

- 8: Blue-chip (buy a modest discount to fair value) limit to 5% to 10% of your portfolio.

- 9 to 10: SWAN stock: buy with confidence at fair value or better, limit to 5% to 10% of your portfolio.

- 11: Super SWAN (as close to an ideal dividend stock as you can find on Wall Street).

I've programmed that watchlist to track prices and use the 52-week low as a means of estimating a target price at which a blue-chip or SWAN stock becomes a Buffett-style "fat pitch" investment. This means a blue-chip/SWAN stock is:

- Trading near its 52-week (or often multi-year) low.

- Undervalued per dividend yield theory (more on this in a moment).

- Offers a high probability of achieving significant multiple expansion within 5 years and thus delivering 15+% long-term total returns over this time period.

Another method you can use is to target blue chips trading in protracted bear markets, such as sharp discounts to their 5-year highs. Buying a company at multi-year lows is another way to reduce the risk of overpaying and boost long-term total return potential.

Basically, "Fat Pitch" investing is about achieving high-risk style returns with low-risk stocks, by buying them when they are at their least popular ("be greedy when others are fearful".)

Dividend Yield Theory: Market-Beating Blue-Chip Returns Since 1966

This group of dividend growth blue chips represents what I consider the best stocks you can buy today. They are presented in 5 categories, sorted by most undervalued (based on dividend yield theory using a 5-year average yield).

- High yield (4+% yield)

- Fast dividend growth

- Dividend Aristocrats

- Dividend Kings

The goal is to allow readers to know what are the best low-risk dividend growth stocks to buy at any given time. You can think of these as my "highest-conviction" recommendations for conservative income investors that represent what I consider to be the best opportunities for low-risk income investors available in the market today. Over time, a portfolio built based on these watchlists will be highly diversified, low-risk, and a great source of safe and rising income over time.

The rankings are based on the discount to fair value. The valuations are determined by dividend yield theory, which Investment Quality Trends, or IQT, has proven works well for dividend stocks since 1966, generating market-crushing long-term returns with far less volatility.

That's because, for stable business income stocks, yields tend to mean-revert over time, meaning cycle around a relatively fixed value approximating fair value. If you buy a dividend stock when the yield is far above its historical average, then you'll likely outperform when its valuation returns to its normal level over time.

For the purposes of these valuation-adjusted total return potentials, I use the Gordon Dividend Growth Model or GDGM (which is what Brookfield Asset Management (BAM) and NextEra Energy (NEE) uses). Since 1954, this has proven relatively accurate at modeling long-term total returns via the formula: Yield + Dividend growth. That's because, assuming no change in valuation, a stable business model (doesn't change much over time), and a constant payout ratio, dividend growth tracks cash flow growth.

The valuation adjustment assumes that a stock's yield will revert to its historical norm within 10 years (over that time period, stock prices are purely a function of fundamentals). Thus, these valuation total return models are based on the formula: Yield + Projected 10-year dividend growth (analyst consensus, confirmed by historical growth rate) + 10-year yield reversion return boost.

For example, if a stock with a historical average yield of 2% is trading at 3%, then the yield is 50% above its historical yield. This implies the stock is 3% current yield - 2% historical yield)/3% current yield = 33% undervalued. If the stock mean-reverts over 10 years, then this means the price will rise by 50% over 10 years just to correct the undervaluation.

That represents a 4.1% annual total return just from valuation mean regression. If the stock grows its cash flow (and dividend) at 10% over this time, then the total return one would expect from this stock would be 3% yield + 10% dividend (and FCF/share) growth + 4.1% valuation boost = 17.1%.

The historical margin of error for this valuation-adjusted model is about 20% (the most accurate I've yet discovered).

Top 5 High-Yield Blue-Chips To Buy Today

Top 5 Fast-Growing Dividend Blue-Chips To Buy Today

Top 5 Dividend Aristocrats To Buy Today

Top 5 Dividend Kings To Buy Today

Bottom Line: If Get A Trade Deal In The Next Few Months, Then We Likely Avoid Recession And The Most Undervalued And Trade Sensitive Stocks Are Likely To Roar Higher

While recession risks are certainly rising (Morgan Stanley's proprietary Business Condition Index just saw its largest single month decline ever and is at 2008 levels), an economic downturn in 2020 is far from certain.

But as Marko Kolanovic, J.P. Morgan’s global head of quantitative and derivatives strategy, recently wrote:

“The U.S. economy is facing a quite unique situation in which one individual can disrupt global trade and investment plans of U.S. corporations, tax consumers on a broad range of imports, etc...Given all of this — why are we not bearish on equities and the economy?Because this situation can also be undone on short notice and many market segments already price in worst-case outcomes...This would translate into a quick [approximately] 5% rally in broad markets, and a 10-20% rally in value and high beta. As a strong market and avoiding a recession would boost re-election odds, it would only be rational to expect this outcome.” - JPMorgan (emphasis added)

What JPMorgan is saying is that undervalued stocks and trade/economically sensitive names (like tech, energy, and financials) are the most likely to outperform following a likely trade deal with China. One that would significantly reduce recession risk by boosting business and consumer confidence and likely keep the longest bull market in history chucking along for the foreseeable future.

This series is meant to highlight the blue-chips off my 189 company watchlist that I consider worth owning because they are likely to prove dependable sources of safe and rising income across the entire economic cycle. And by buying deeply undervalued companies (confirmed via several of these methods), you have the best chance of both enjoying short-term market rallies like we're seeing now, as well as minimize the probability of a permanent loss of capital during inevitable future market declines.

But even deeply undervalued blue-chips can still fall in a fearful market. Never forget what Peter Lynch (second greatest investor in history behind Buffett) famously said:

"Far more money has been lost by investors preparing for corrections, or trying to anticipate corrections than has been lost in corrections themselves...If you're in the market, you have to know there's going to be declines... When they're gonna start, no one knows. If you're not ready for that, you shouldn't be in the stock market... What the market's going to do in one or two years, you don't know. Time is on your side in the stock market." - Peter Lynch (emphasis added)

My goal with these articles is to provide good investing ideas, in companies with high margins of safety that have less to fall in a market correction or bear market, and which are all coiled springs that are likely to deliver outsized total returns if their valuations return to historical levels. No matter what the broader market is doing, quality blue-chips are always on sale.

But always remember that all of my dividend stock recommendations are purely meant as buying ideas for the equity portion of your portfolio and never as bond alternatives. Always use the appropriate risk management and asset allocation for your individual needs.