The legal cannabis industry was one of the biggest disappointments of 2019 and smaller player OrganiGram Holdings (NASDAQ:OGI) was no different. Last year, OrganiGram stock shed nearly 32% after failing to sustain momentum during the first half. However, a recent earnings lift may help build the case for OGI shares in 2020.

In a market segment that quickly earned a reputation for consistently not delivering on the hype, OrganiGram was a breath of fresh air. For the fiscal first quarter of 2020, the company rang up revenue of 25.2 million CAD ($19.03 million), more than doubling the year-ago quarter’s haul. More importantly, the sales tally beat analysts’ consensus target by a whopping 10.2 million CAD.

Further, adjusted earnings before interest, taxes, depreciation, and amortization (EBITDA) finally went back up into positive territory. Over the last three quarters, EBITDA had dipped worryingly into the red. With so much positive enthusiasm, OrganiGram stock launched into low-earth orbit.

But just as quickly, gravity took hold of shares and mercilessly crated them. At time of writing, OrganiGram stock has given up almost all its fiscal Q1 gains. So, what caused the immediate reversal?

Primarily, a closer examination of the numbers suggests that while enthusiasm in OGI was warranted, the magnitude wasn’t. Yes, Q1 delivered a strong comparative revenue beat. However, the sales tally for fiscal Q2 2019 actually exceeded recent results to the tune of 7.3%. And the following Q3 report wasn’t that much off.

Cannabis consumption isn’t exactly seasonal. Whether you want to use it –medicinally or recreationally — it’s discretionary funds and not the weather that determines your purchasing decision.

Nevertheless, I think there’s enough to like here to interest risk-tolerant speculators.

Efficiency is Working in Favor of OrganiGram Stock

Given the dramatic losses in the cannabis sector in 2019, this caveat is true for any sector player: marijuana or CBD shares have the potential to make you rich as much as make you poor. If you can’t handle the volatility, this is not a segment you want to engage.

Even if you can handle it, you want to gamble responsibly. That’s especially the case for a small-cap investment like OrganiGram stock.

But on the positive side, what I do like about the underlying company is management’s fiscal discipline. Unlike other pot firms that seemingly abandoned business basics to focus purely on growth, OGI is comparatively taking baby steps. In the infancy stage of the marijuana game, that might have ticked off investors. Now, everyone sees such an approach as prescient.

As you may know, OrganiGram has a single cultivating and processing facility. Rather than stretch themselves to expand their footprint, management has instead decided to make their lone facility more efficient.

One of the key takeaways from the fiscal Q1 report is that this efficiency protocol is working: in the three months ending Nov. 30, 2019, the cost to produce a gram of dried flower was 61 cents CAD. That compared favorably to fiscal Q4’s metric of 66 cents CAD.

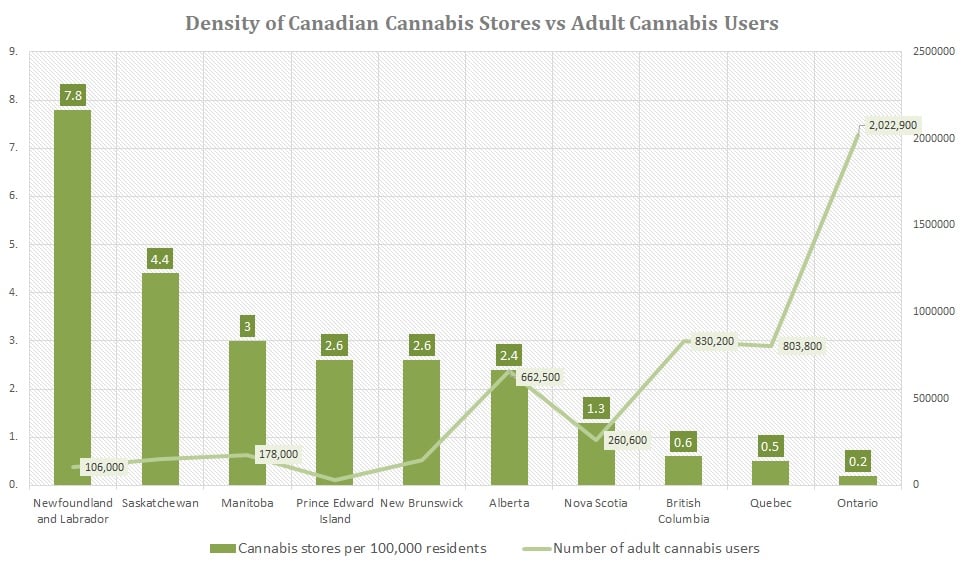

As well, the Canadian government badly bungled their retail marijuana roll-out. I’ve written about this situation before concerning other cannabis stocks. Currently, the biggest cannabis markets often have the fewest number of stores to service the demand. It’s a classic case of government bureaucracy gone wrong.

But for OrganiGram stock, this theoretically isn’t as much of a dealbreaker as it is for hyper-growth-oriented names, like Canopy Growth (NYSE:CGC) or Aphria (NYSE:APHA) From the get-go, OGI was never about quantity but about quality.

Attractively Positioned in the Markets

Interestingly, a study on the purchasing considerations of Canadian cannabis users revealed that quality and safety ranked highest. Lowest price ranked as the second-most important consideration. However, I was shocked at the magnitude gap between the two.

As I just mentioned, OrganiGram focused on taking their lone facility and making it the best. Fortuitously, this was the right call. Supply chain headwinds among other issues made the quantity game a losing one. It also implies that its products feature at least stricter quality control.

This plays into the Canadian market sentiment perfectly. Because the company was also more fiscally disciplined, this suggests that they have some cushion to compete on price. That’s a double whammy that could make OrganiGram stock quite interesting in 2020.