1. Technical parameters

A few words about the technical picture to begin with.

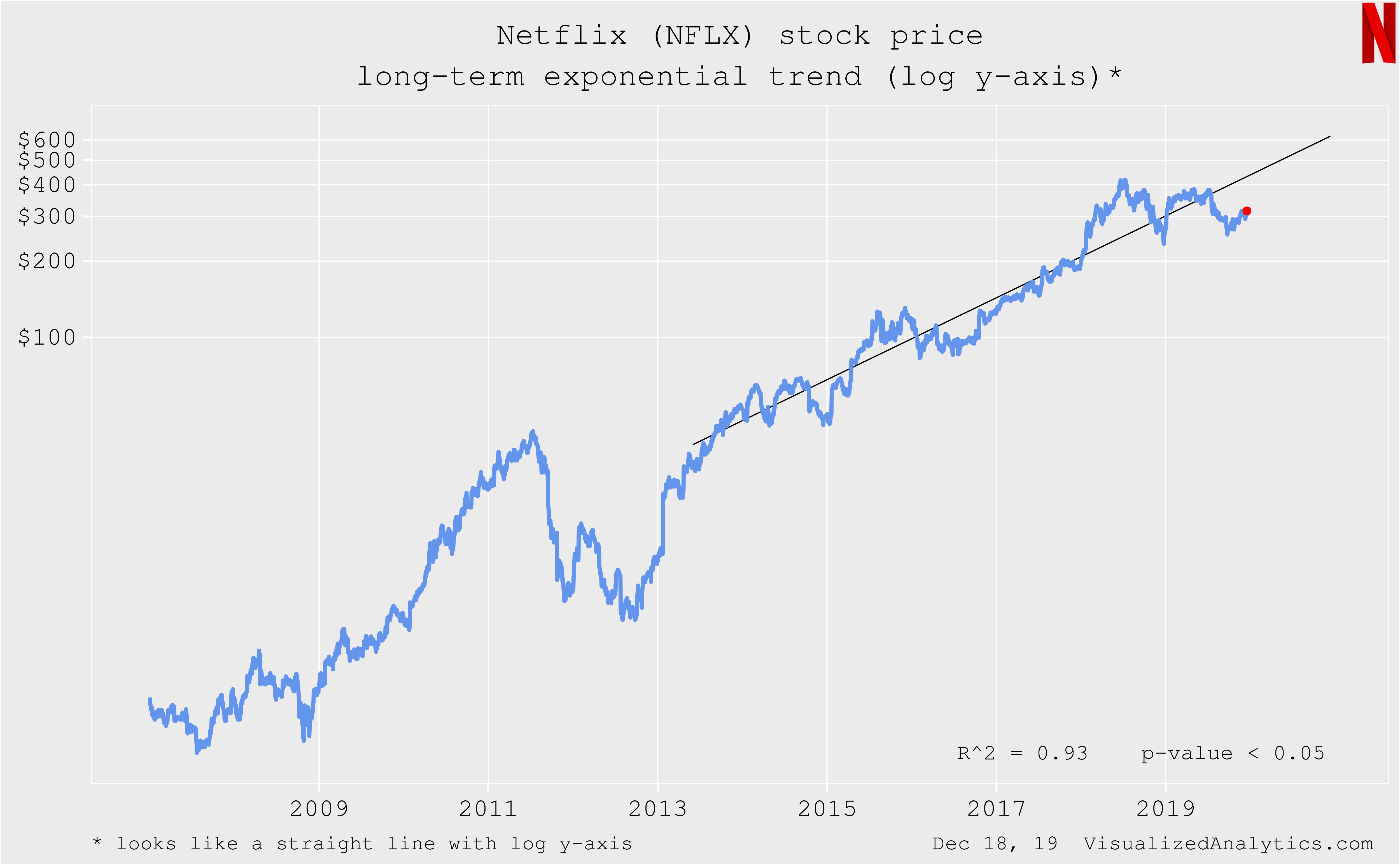

Starting from 2013, Netflix's (NFLX) stock price has been following its long-term exponential trend:

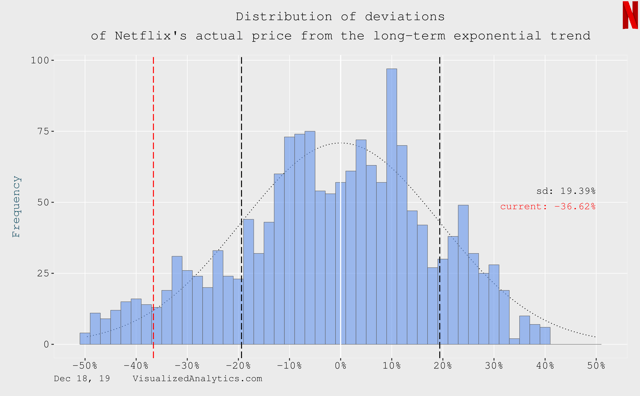

Now, the company's stock price is below this trend by more than one standard deviation:

At the same time, there are early signs of a gradual synchronization of the dynamics of Netflix stock price and its exponential trend.

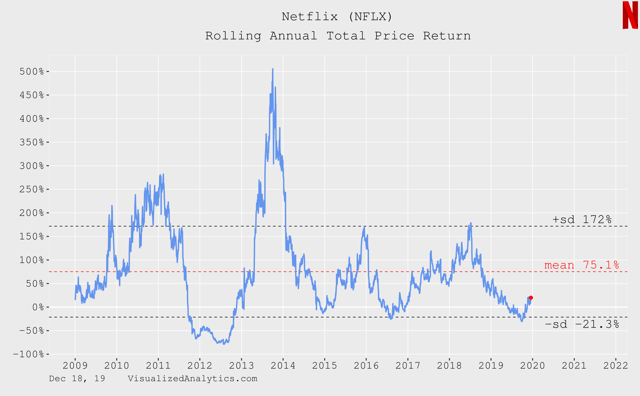

Throughout the year, the rolling annual total price return of Netflix's stock has been fluctuating around the lower border of the standard deviation. It's typical when reaching the bottom:

So, technically, now Netflix's stock price is prone to growth.

2. Growth drivers

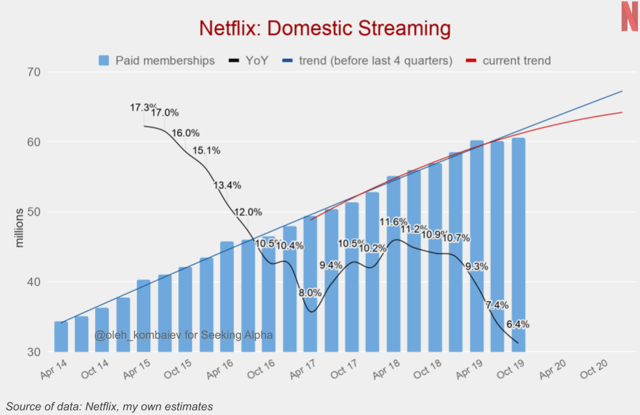

According to the current trend, it is possible to predict that the audience of "Domestic Streaming" will have reached 64 million by the end of 2021. Before the results of 2019 were published, the trend had assumed that it would be 67 million over the same period. It means that most likely peak saturation levels for this segment have been reached.

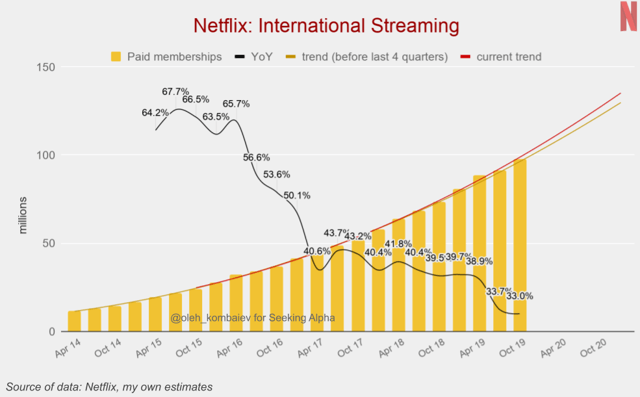

But the audience of "International Streaming" is still growing exponentially. Here, one can expect that its number will be 135 million by the end of 2021.

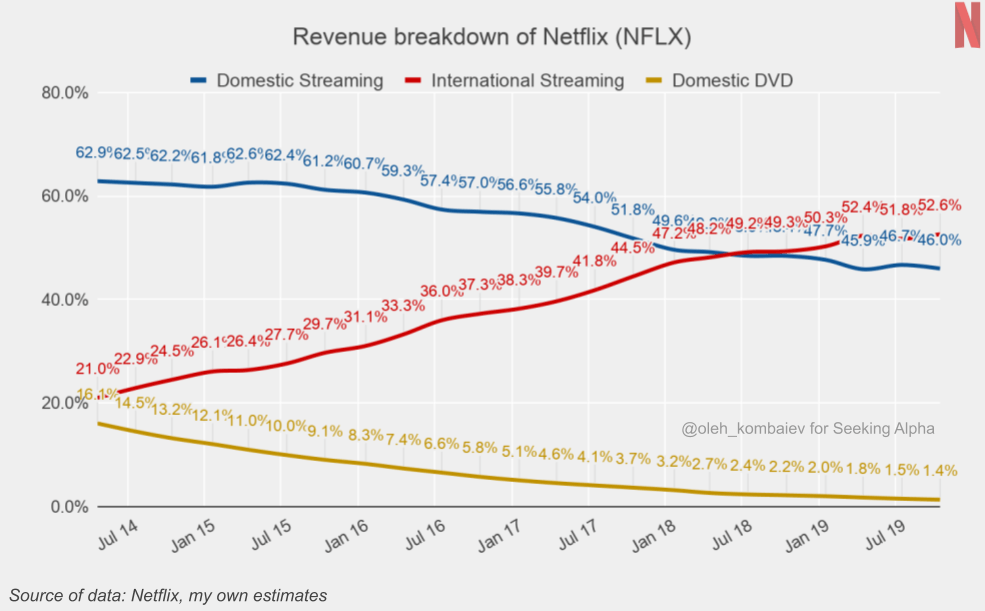

In any way, now Netflix drives most of its revenue from outside the U.S. But I would not say that it is bad because there are no signs of saturation for this segment, yet.

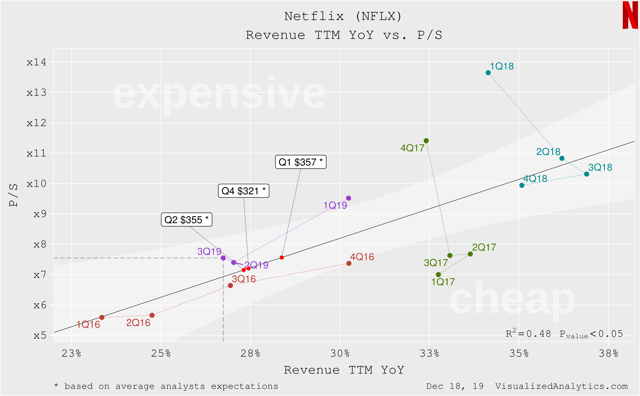

Going further. Having considered the long-term relationship between Netflix's revenue growth rate and its P/S multiple, it should be recognized that the current price of the company is balanced. But, according to the average estimates, the revenue growth rate is expected to accelerate in the coming quarters. In the bounds of this model, this will raise the balanced price of the company's share to $360:

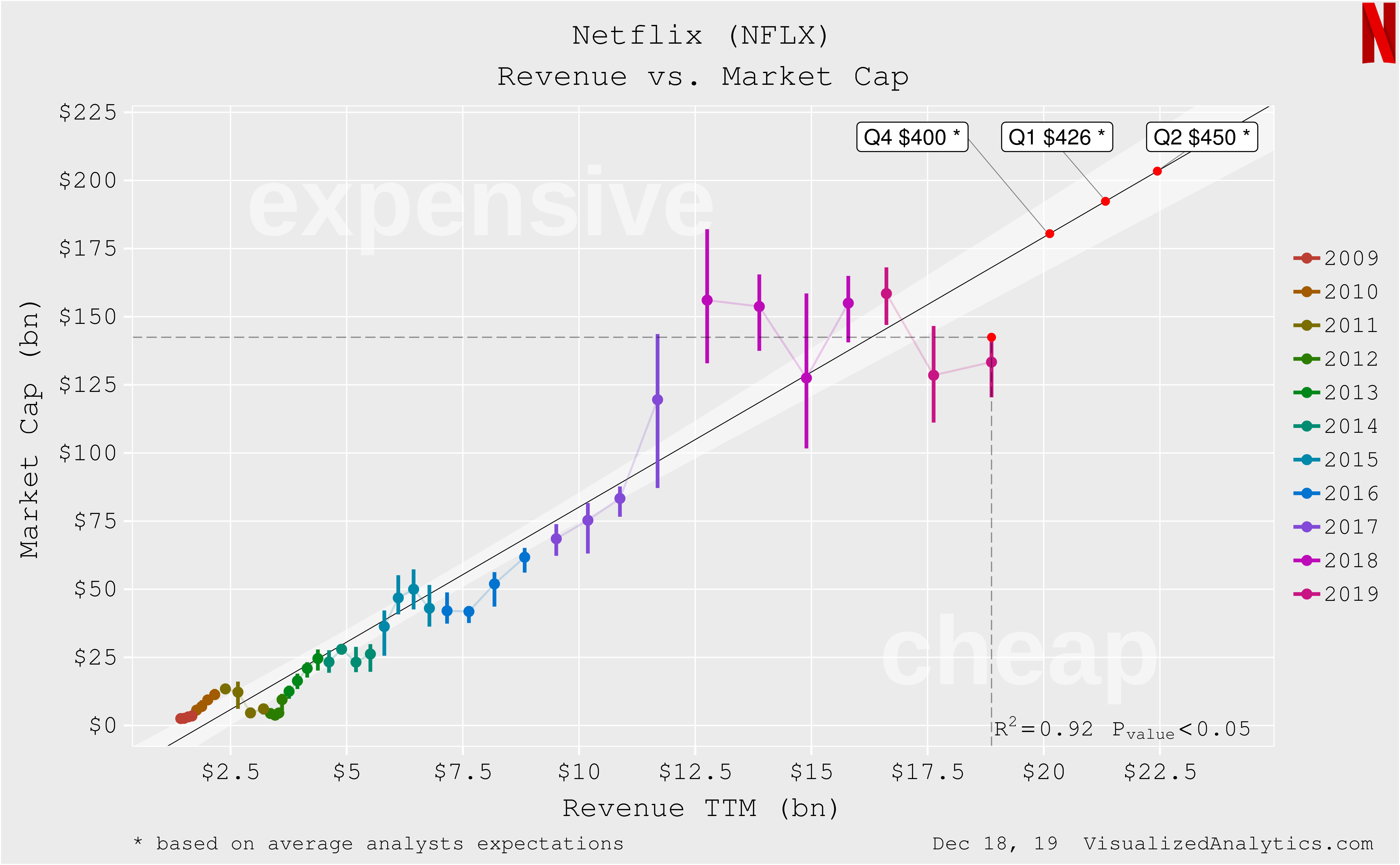

Next. Netflix's capitalization is heavily dependent on the absolute size of the company's revenue TTM. If we take the analysts' average expectations as a basis within the bounds of this model, the company's balanced price per share in Q2 2020 will be around $450:

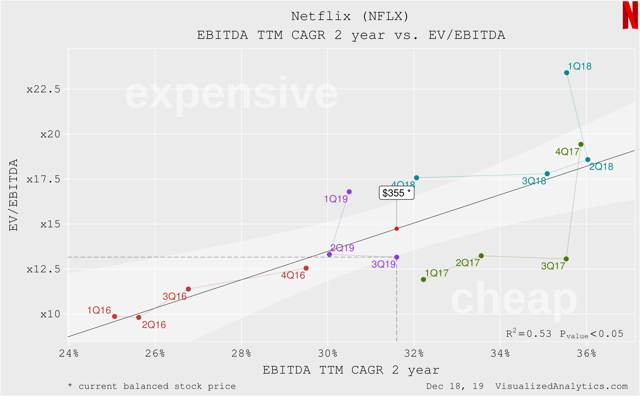

Over the last four years, Netflix's capitalization has been responding well to the EBITDA growth rate. As demonstrated by the following chart, the current growth rate of this indicator points to the undervalued state of the company:

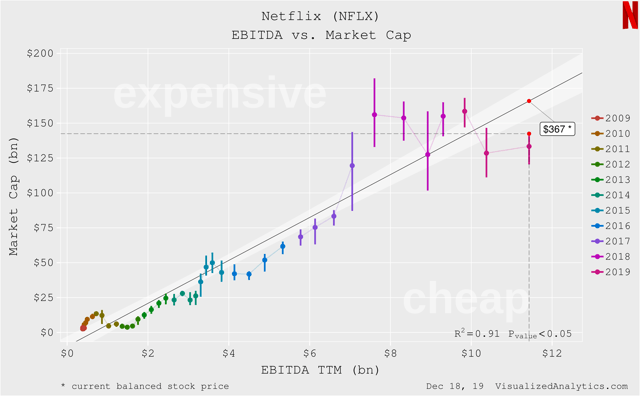

Based on the long-term relationship between the EBITDA TTM absolute size and the company's capitalization, Netflix's current price is undervalued too:

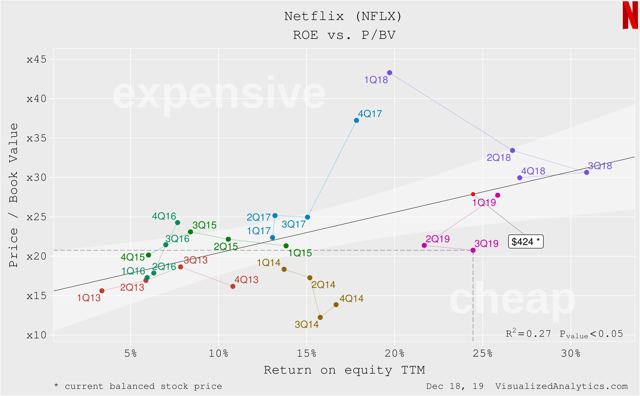

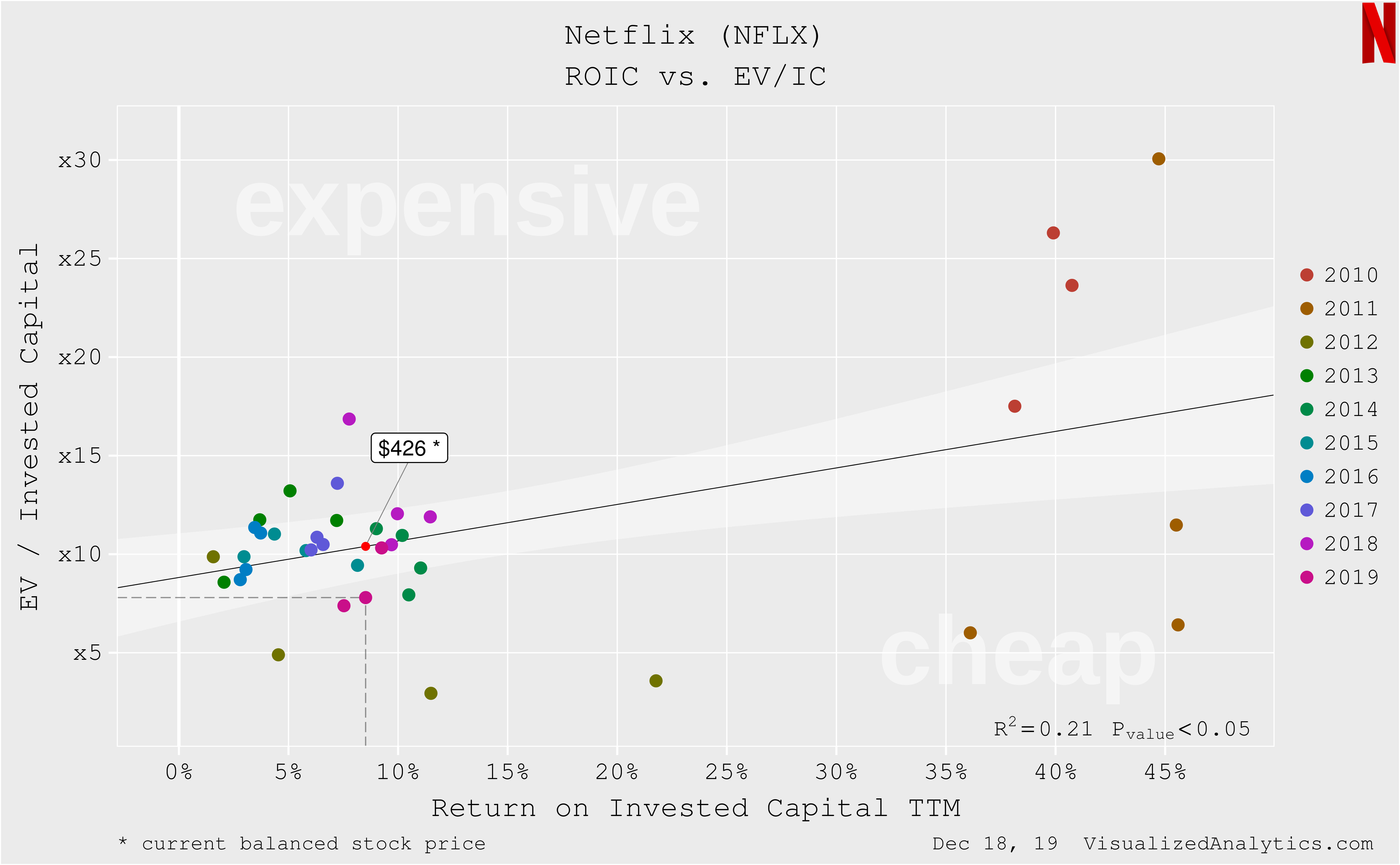

There are also some specific dependencies, all of which characterize Netflix as undervalued:

In terms of well-established relationships, Netflix's balanced or rational price is definitely above its current level.

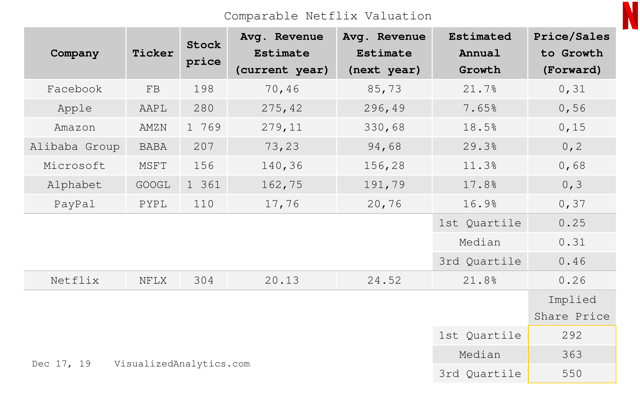

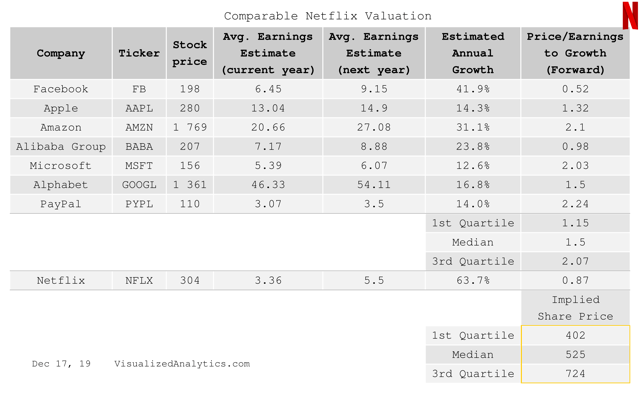

3. Comparable valuation

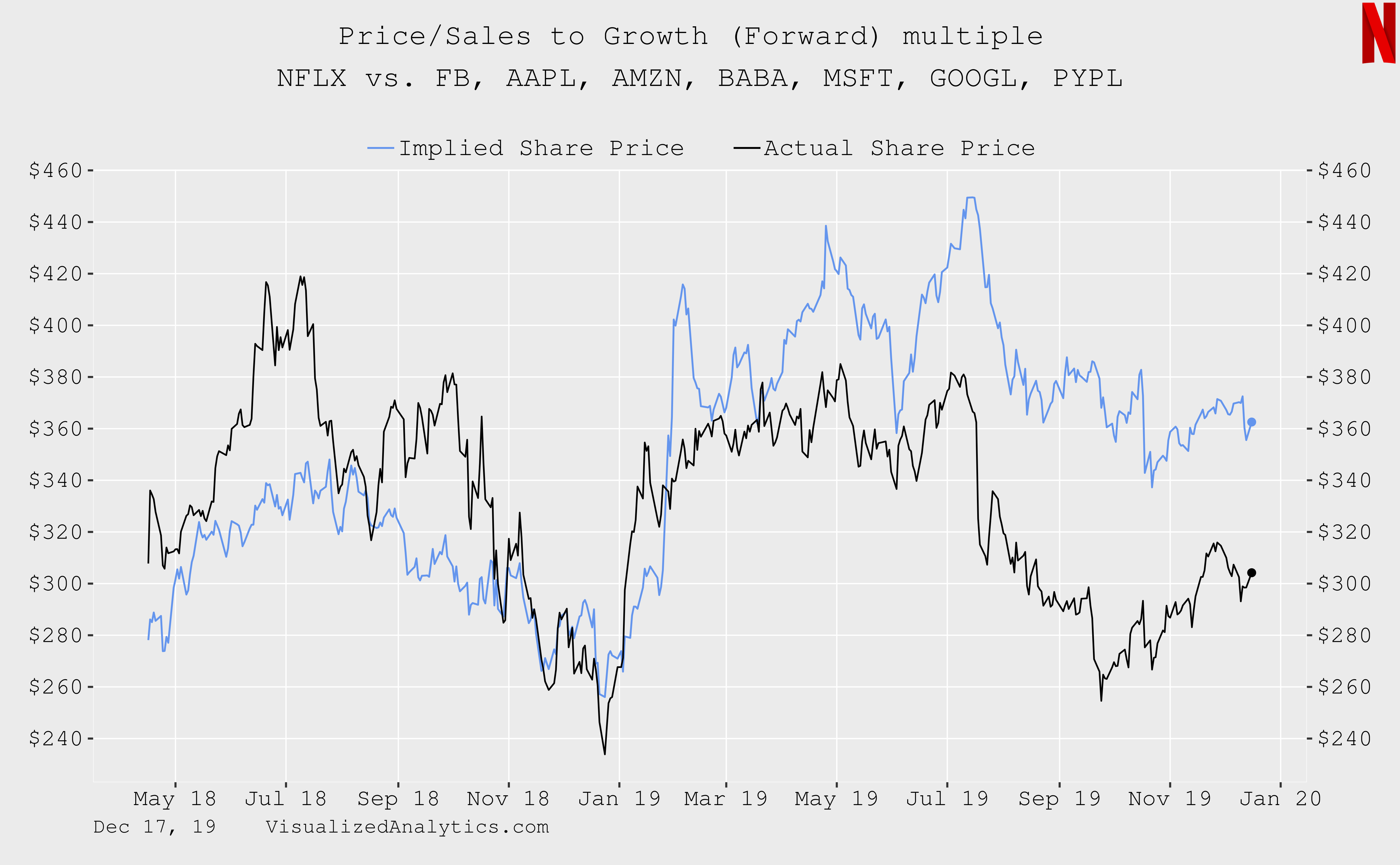

Judging by the P/S (forward) multiple adjusted by the expected revenue annual growth rate, Netflix's share stock price is now 20% below the balanced level:

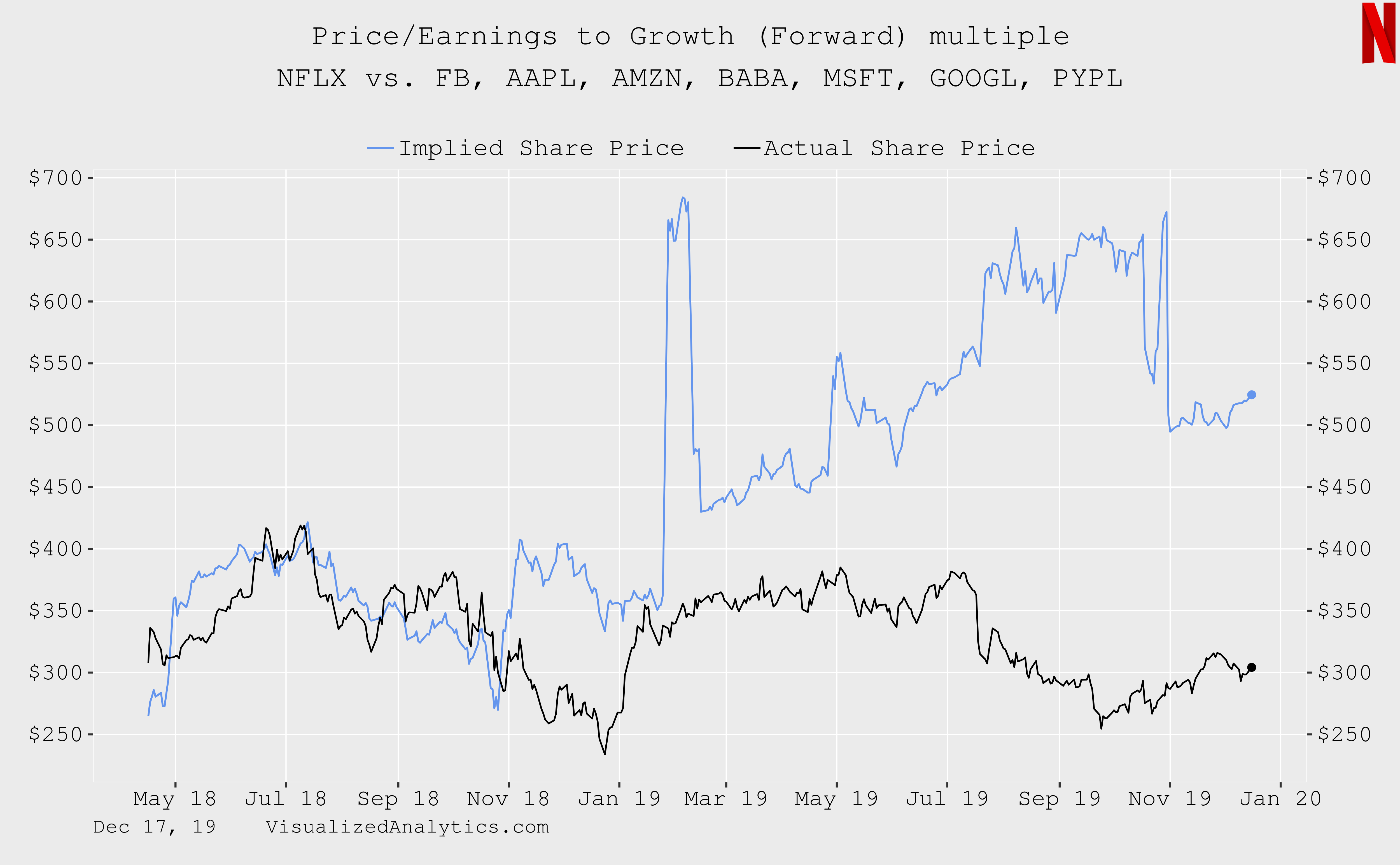

Judging by the P/E to growth (forward) multiple, Netflix is undervalued as well, and over time, this undervaluation tends to increase:

In terms of the key forward-priced multiples, now Netflix is undervalued relative to the main blue chips in Nasdaq.

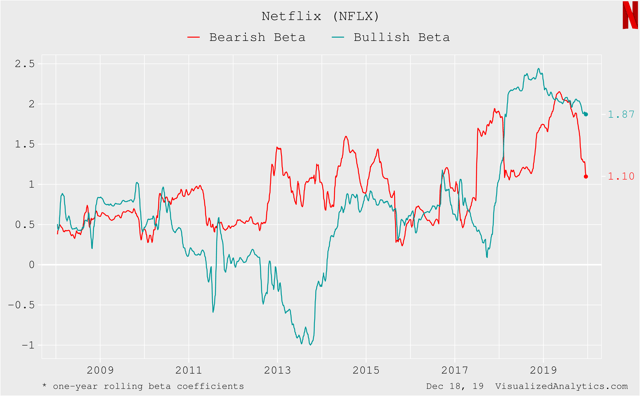

4. Risk Parameters

Netflix's Bearish Beta (a measure of how a stock price tends to drop when the market is only down) is much less than the Bullish Beta (a measure of how a stock price tends to rise when the market is only on the rise). It means that Netflix stock is more responsive to the overall growth of the stock market than to its decline.

Bottom line

There is a saying: In a long-distance race wins not the one who runs faster but the one who runs out first. Of course, increasing competition is a challenge for the company. But the leading position of Netflix has not changed. At the same time, given the foregoing, Netflix is clearly not overvalued now.