Introduction

I am a do-it-yourself investor and a firm believer in investing according to the business cycle. I wrote "Portfolio Strategies For Employer Sponsored Plans" for Seeking Alpha in October describing investment strategies for plans with limited options. This month I met with a Fidelity Financial Adviser and moved all of my pre-tax funds from the Employer Sponsored Plan into a Traditional IRA to expand access to other funds. I used the methods described in this article to develop a proposed portfolio, and have a followup meeting to finalize the transition.

As I have written during the past year in, "Portfolios Of Funds That Do Well In A Bear Market" and "Building Bear Market And Full Cycle Portfolios", I have concentrated on reducing risk in portfolios. The past three months has been a good stress test to see how funds will perform in a Bear Market. In this article, I selected one hundred funds in 47 different Lipper categories that have done well during the past year or have the potential to do well if interest rates rise at a slower rate.

The funds were selected based on Ulcer Index, Maximum Draw Down, Martin Ratio, and Risk and Rank Ratings from Mutual Fund Observer. Morningstar was used to further reduce the funds based on performance during the recent downturn. Portfolio Visualizer was used to create portfolios with approximately 10 funds for each of Vanguard, Fidelity, other mutual funds, and exchange traded funds to maximize return at 3.5% volatility (standard deviation) which compares to 5.0% for my baseline, Vanguard Wellesley Income Fund (VWIAX).

Below is a summary of the Model Portfolios for the past 12 months. For the Combined Fund Portfolio, I chose one fund per Lipper category to avoid over-concentration of investments. Based on this information, my ideal defensive portfolio in this environment will have a standard deviation lower than the Wellesley Fund, have about 35% stocks which are mostly large caps overweighted in health care, real estate, and utilities, and a very low allocation to high yield bonds.

Investment Model

The Investment Model is built upon 30 main indexes including leading and coincident indicators, monetary policy, interest rates, housing, income, orders, profits, valuations, inflation, and financial risk, among others. It was built to provide a six month outlook of the direction of the stock market. It currently shows that the investment environment has been deteriorating since late 2017 and the decline has accelerated during the past quarter. The risk of a recession starting in the near term is relatively low, in my opinion, and I expect the markets to recover, but remain volatile in 2019.

The slowdown has become more pronounced and the number of negative indicators is starting to increase.

The Federal Reserve Bank of Atlanta GDPNow raised its forecast to 3.0% real growth from 2.4% last week.

Indicator Highlights

Below is the Monetary Policy Indicator in the Investment Model. It is a composite of money supply, federal funds rate, 1 Year Treasury rate minus the federal funds rate, and monetary base. It reflects higher interest rates and the unwinding of Quantitative Easing.

While there are many positives in the economy, Construction is showing weakness.

Orders are starting to show weakness.

Housing is not doing well.

The Global Economy is slowing down.

Rising interest rates slow the economy and the yield curve has inverted for two and five year rates.

Financial Risk (Conditions, Stress, Uncertainty, and Volatility) is increasing.

Retail and Institutional Investors have been building cash reserves modestly. In the short term, Retail Investors are increasing Money Funds, while Institutional Investors are decreasing them.

Funds By Lipper Category

Below are the Lipper Categories and the funds selected. I selected funds from Vanguard, Fidelity, other mutual funds, and Exchanged Traded Funds, if they met the volatility and risk criteria. Average Risk (1 is lowest risk and 5 is highest) is the Mutual Fund Observer risk rank average of funds shown for each Lipper Category. Average Rank (5 is best rank and 1 is lowest) is the Mutual Fund Observer performance rank of funds shown for each Lipper Category. The majority of the funds in my proposed Fidelity Portfolio are in the list below with the exception of the Fidelity Advisor Multi-Asset Income Fund (FAYZX).

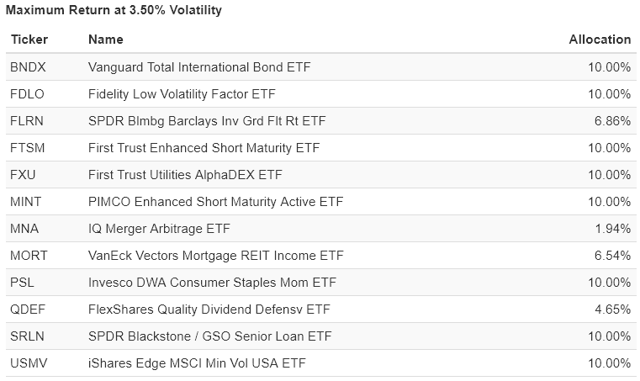

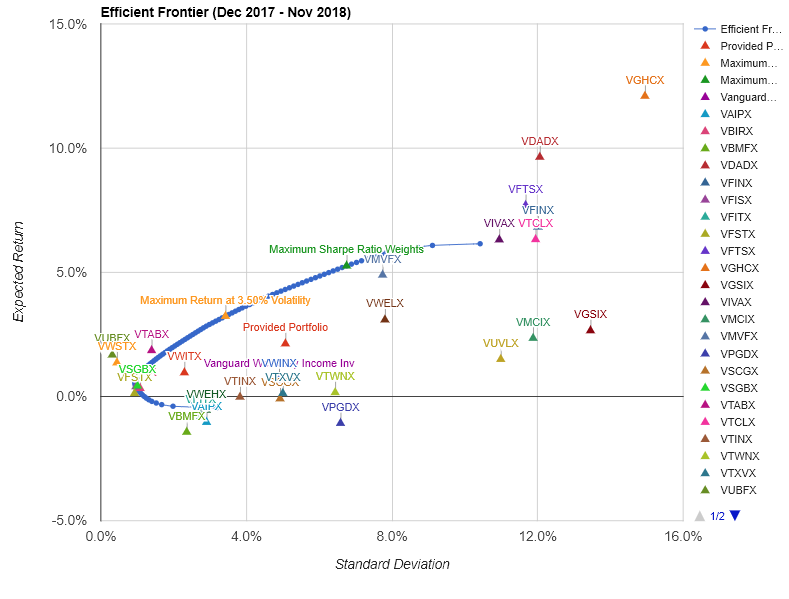

Exchange Traded Funds

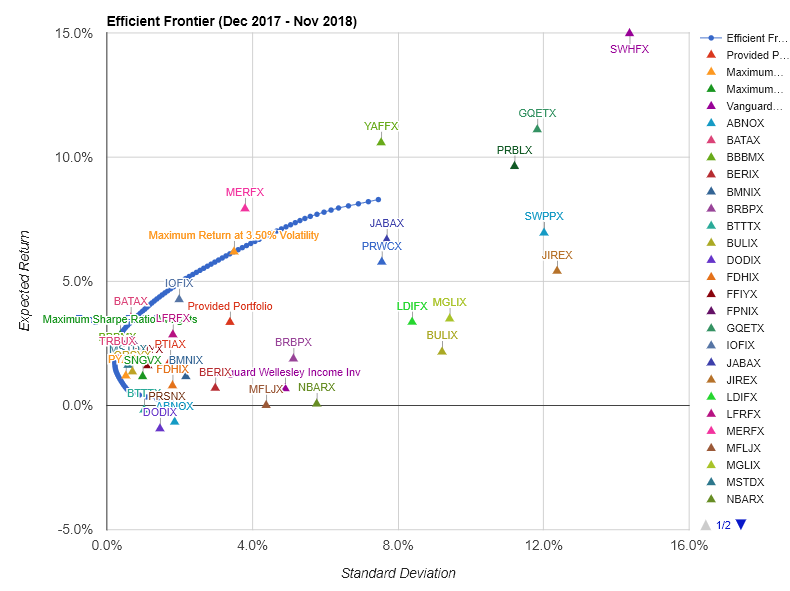

The link in Portfolio Visualizer is provided and interested readers can change parameters to suit their own tastes. The following is the Efficient Frontier (Return vs Volatility) for the Exchange Traded Funds for the past year. Standardization is a measure of deviation from the mean. In "The Great Owl Portfolio", I show the relationship of Standard Deviation to Bear Market Deviation and Martin Ratio.

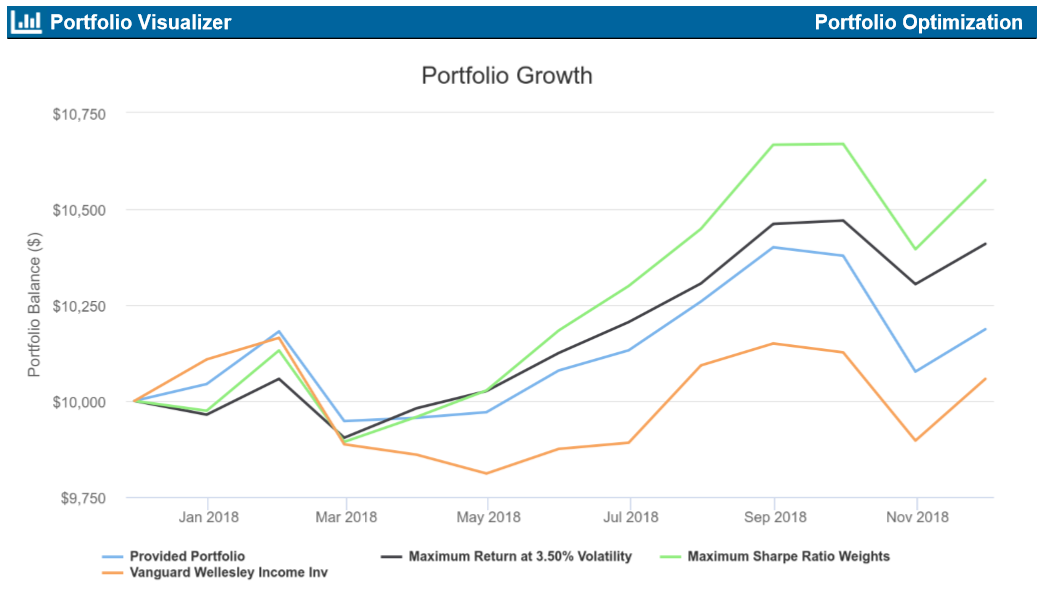

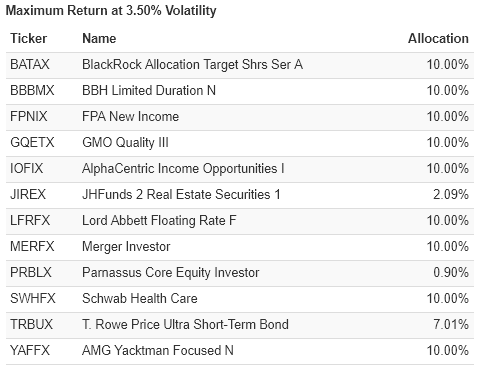

The Exchange Traded Funds selected to maximize return at 3.5% volatility are shown below. The return for the 3.5% Volatility Portfolio was 5.6% while the maximum draw down was 1.6. This compares to -0.5% return for the Vanguard Wellesley Income Fund (VWINX) with a maximum draw down of 3.5%.

In addition to the Portfolio with the Maximum Return at 3.5% volatility is the Vanguard Wellesley Income Fund (VWIAX). The Provided Portfolio is the equal weighted universe of selected exchange trade funds.

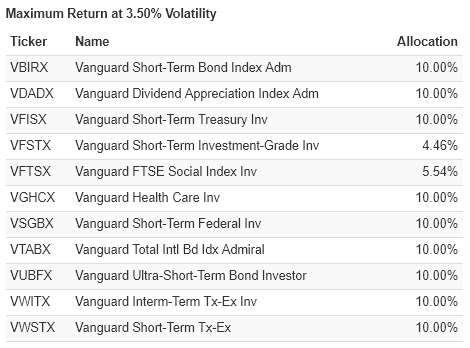

Vanguard Mutual Funds

The link in Portfolio Visualizer is provided. The following is the Efficient Frontier (Return vs Volatility) for the Vanguard Mutual Funds for the past year.

The Vanguard Mutual Funds selected to maximize return at 3.5% volatility are shown below.

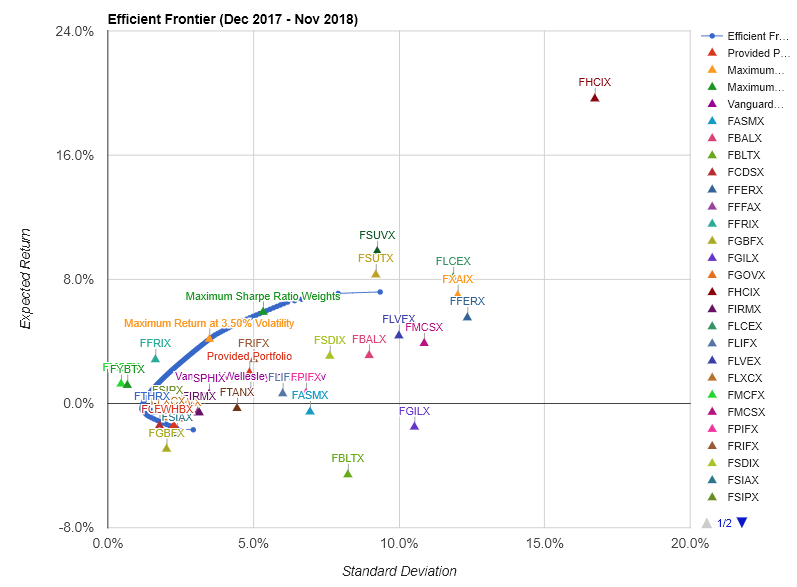

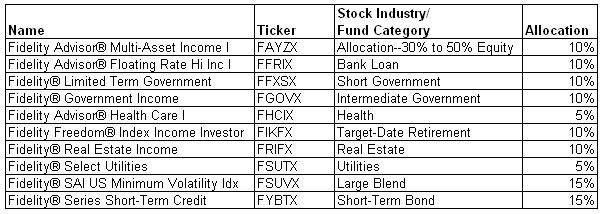

Fidelity Mutual Funds

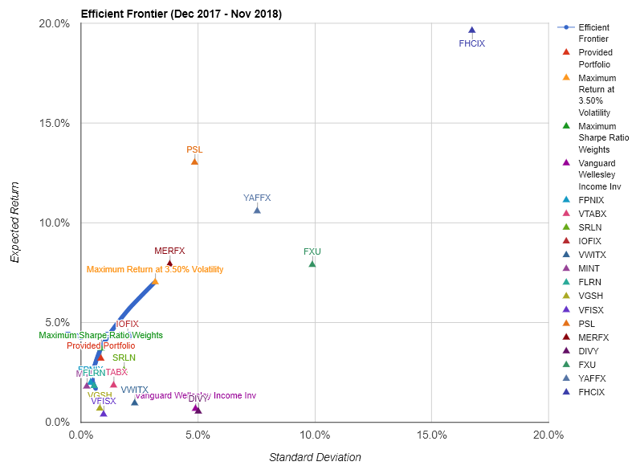

The link in Portfolio Visualizer is provided. The following is the Efficient Frontier (Return vs Volatility) for the Fidelity Mutual Funds for the past year.

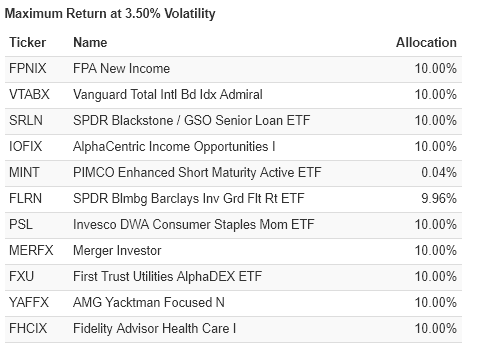

The Fidelity Mutual Funds selected to maximize return at 3.5% volatility are shown below.

Other Mutual Funds

The link in Portfolio Visualizer is provided. The following is the Efficient Frontier (Return vs Volatility) for the Mutual Funds other than Vanguard and Fidelity for the past year.

Source:

Source:

The Mutual Funds other than Vanguard and Fidelity selected to maximize return at 3.5% volatility are shown below.

Combined Funds

All of the 100 mutual funds and exchange traded funds are used to create the combined portfolio. The link in Portfolio Visualizer is provided.

From the combined list of 100 mutual and exchange traded funds, the funds selected to maximize return at 3.5% volatility are shown below.

By comparison, the same 100 funds were used to maximize the Sharpe Ratio.

Comparison Of Portfolios

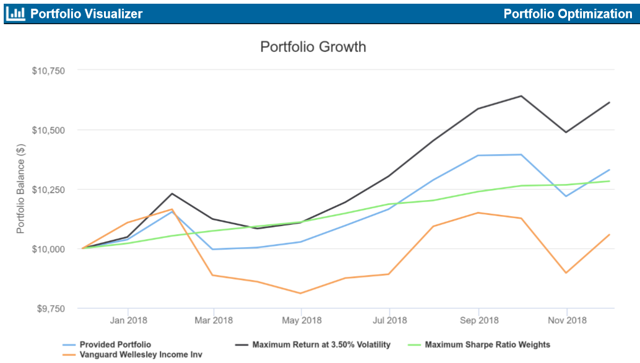

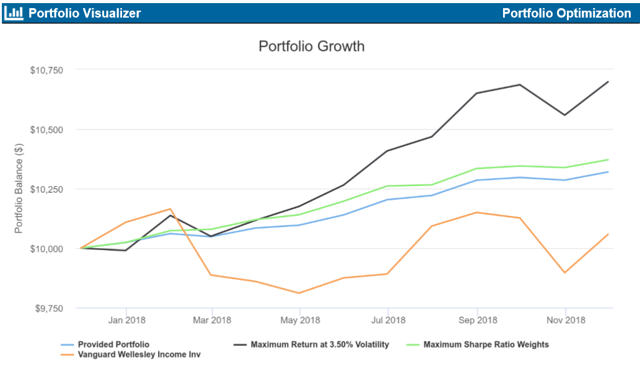

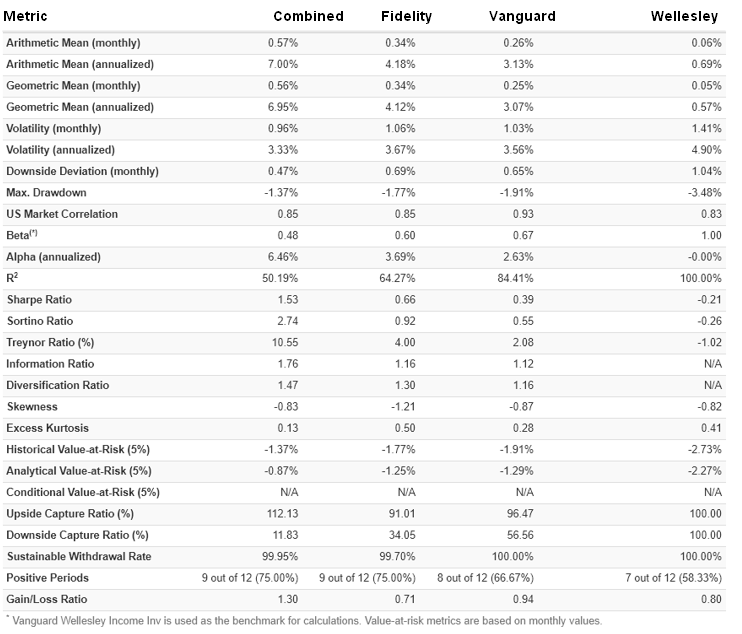

The Portfolios for the Vanguard Funds, Exchange Traded Funds, Combined Funds are compared, along with the Vanguard Wellesley Income Fund which I use as a conservative baseline fund. As can be seen below the Portfolio from the Combined Funds has a higher return with lower draw down than the others including the Vanguard Wellesley Income Fund. The link in Portfolio Visualizer is provided.

Conclusion

Future performance is guaranteed to be different than the past. The optimum portfolio is a journey and not a destination. Moving funds from an Employer Sponsored Plan to a Traditional IRA sped up the process, but other areas of my portfolio still need attention.

Below is my choice for a conservative, defensive portfolio as I near retirement. It is about 35% stock with about 75% in large cap stock and is overweight in defensive sectors. I will create a CD ladder instead of some of the bond funds when I meet with my Financial Adviser. The portfolio below would have returned 4.5% YTD with a maximum draw down of -1.7%.

I write one or two articles per month which involve investing according to the business cycle, managing risk and/or portfolio optimization. I write based on the topics that interest me, as someone approaching retirement.