There supposedly is no such thing as a free lunch. But every December and January, Wall Street does offer up something that comes close.

That’s because of two forces that artificially depress certain stocks’ prices in December. When those forces are removed every January, as they inevitably are, those artificially-depressed stocks -- far more often than not -- enjoy an outsized bounce.

These two forces are window dressing and tax-loss selling. In the first, of course, institutions sell their losers as Dec. 31 approaches, to avoid the embarrassment of showing, in their year-end reports, that they had owned a losing stock. In the second, investors sell their losing stocks before the end of the year to realize losses that they can use to offset capital gains on which they would otherwise have to pay taxes in April.

Notice carefully that neither of these two forces has anything to do with stocks’ intrinsic value. Nor do either of those forces persist into January.

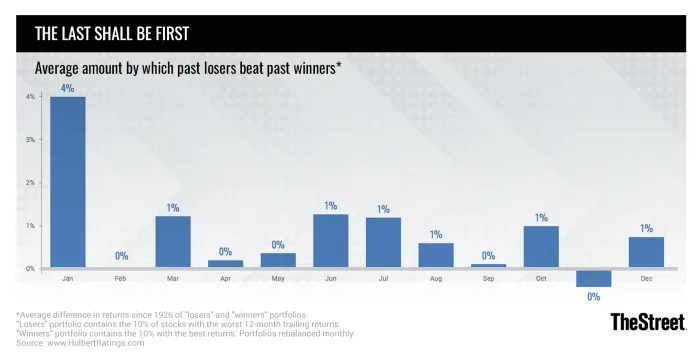

One way to gauge the magnitude of these losing stocks’ rebound potential in January is by comparing the performance of two hypothetical portfolios: One contains the 10% of stocks with the worst trailing 12-month returns, while the other contains the 10% with the best returns. Both portfolios are reconstituted each month.

In all Januarys since 1926, according to data from Dartmouth University finance professor Ken French, this losers portfolio has beaten the winners portfolios by an average of 4.0 percentage points. On an annualized basis that’s equivalent to more than 60% per year.

In the other 11 months of the calendar, in contrast, the losers portfolio beats the winners portfolio by an average of just 0.6 percentage points per month. The difference between January and the other months is highly significant according to traditional statistical standards.

George Putnam, editor of The Turnaround Letter, tries to do even better than this already-impressive historical tendency. Each December, he selects from a list of the year’s worst performers those stocks he thinks have the greatest potential to rebound in the New Year. The table below shows the results from the past three years.

Performance from Nov. 30 through the following Jan. 31:

Year | Year-End Bounce Candidates | S&P 500 |

2018 | -6.9% | -1.5% |

2017 | 12.9% | 6.9% |

2016 | 8.4% | 3.9% |

Notice that the table reports performance from the end of November, which is when Putnam releases each year’s bounce candidates. You could do better than the numbers reported here if you put in buy orders below the Nov. 30 prices for these stocks, anticipating that tax-loss selling in December would depress their prices even further.

Notice also that Putnam’s 2018 year-end bounce candidates lagged the market as a whole. This market-lagging performance, however, was almost entirely attributable to just one stock on Putnam’s 2018 list: Pacific Gas & Electric. That stock, you may recall, lost nearly half its value in the December-January period a year ago, as the company filed for Chapter 11 bankruptcy protection.

That stock therefore serves as a cautionary reminder that there are no guarantees on Wall Street, even when you are trying to exploit something that’s close to being a free lunch. And it also serves to remind us that we should diversify our bets among several stocks rather than on just one situation.

With all this in mind, below are the year-end bounce candidates that Putnam last week released to clients:

Duluth Holdings (DLTH)

L. Brands (LB)

Meredith Corp. (MDP)

Mylan N.V. (MYL)

Occidental Petroleum (OXY)

Residio Technologies (REZI)