Icanic Brands Company Inc. (ICAN:CSE; ICNAF:OTCQB) is the fast-growing micro-cap stock with the only fully automated, high-speed cannabis pre-roll manufacturing technology on the planet.

At up to 1,000 pre-rolls per hour, this machine definitely means faster production and a more consistent product for consumers than every competitor out there. But it could also mean higher margins and better cash flow.

This only makes sense—hand-made pre-rolls could only be done at a fraction of that pace. It's simple economics.

Icanic's machine—after more than two years of research and development (R&D)—is already making an impact. April 2020 was its first month in full operation, and in their last public quarterly (Q3/20) [Icanic] said that gross margin was 44%, and they reported their first-ever positive EBITDA [earnings before interest, taxes, depreciation and amortization]—over $130,000! Positive cash flow is exactly what cannabis investors (and institutional buyers!) want to see.

The cannabis stocks that have been doing really well in 2020—like Trulieve Cannabis Corp. (TCNNF:OTCMKTS) and Jushi Holdings Inc. (JUSH:CSE; JUSHF:OTCMKTS)—have fast-growing top line and cash flows (EBITDA).

Icanic reports their year-end financials (YE/20) at the end of November. Their machine will have been working for the fullquarterly, for the first time.

Icanic operates in California and Nevada—making it an MSO (multistate operator). They have been steadily gaining new dispensaries where they sell their market leading GangaGold brand, and their new Taylor's brand.

With nine-month 2020 revenues of $5.3 million, versus $265,000 in 2019, the market knows that the YE/20 numbers will be much better for Icanic than last year. The automated pre-roll machine has been working steadily since April—the month they reported their first-ever positive cash flow. I'm excited to see what kind of growth they can show!

So YE/20 financials could be a big catalyst for shareholders. But even before that—just in a few days, in fact—a Democratic win in the U.S. election could see a lot of money funds flow move into U.S. MSOs.

Icanic has already shown they can generate positive cash flow for these funds at a very small annualized revenue. They could be one of the biggest beneficiaries of any new inflow of institutional capital into this space.

Rapidly improving cash flow—which Icanic has already showed in its financials—is what makes companies successful, and attract institutional interest in their stock.

There Are So Many Growth Avenues Here

1. Pre-rolls are now just 10% of sales, which means that almost everyone is choosing to do it the hard way by rolling their own.

But folks, that wasn't a choice: It was the only option. No automated pre-roll production technology has become accepted. The best existing technologies are very manual, which results in poor quality and consistency of pre-rolls.

Icanic Brands has an automated pre-roll technology that is already working—and pre-roll sales are going to become the choice of the consumer, because pre-rolls will suddenly be more convenient and higher quality.

Once everyone realizes you can buy the same high-quality pre-roll, all the time—just like you can with cigarettes—the market will see a huge shift. That should benefit Icanic a lot. It's all about delivering the same product, every single time.

I think this machine has the potential to be an inflection point for the U.S. cannabis industry. I mean, there is no way that five years from now, with national sales in the hundreds of millions of dollars, that hand-rolling joints will still be 90% of the market.

Businesses will automate to create efficiencies and become more profitable. It happens in every industry, all the time. This is just the first one. But competitors will find it very hard to duplicate. This machine was not easy.

Other growth avenues:

2. The machine is only doing one shift per day, five days a week. With sales increasing, they can move it up to two shifts, then three shifts, then seven days a week.

3. More municipalities in California are allowing cannabis sales. Icanic can continue to grow their more than 350 dispensary count.

4. Icanic is growing in Nevada as well. The millions of tourists that flock there (post-COVID of course) do not want to work to roll their own.

When you are a low-cost producer, scale (by definition) brings larger cash flows. By the end of November, investors will get their first good look at how that is working for Icanic.

5. Macro growth in cannabis [is occurring] across the United States.

Growth is exactly why investors should be interested in the cannabis sector—because the growth in revenue, earnings and cash flow of this sector are going to be vastly superior here over other sectors for the next 20 years.

That is not a debatable point. It is a fact supported by hard data.

Historically the American economy has grown at a rate of 2–3% per year. Going forward we are going to be lucky if we get that.

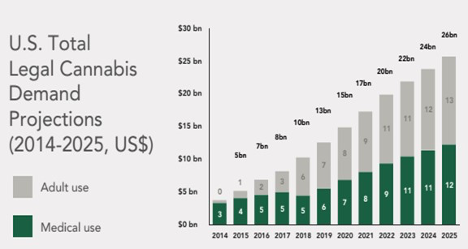

Meanwhile projections for the cannabis industry all look like this one, from New Frontier Data….

While the overall economy grows at a rate of 2–3% in the coming years, legal cannabis sales will be growing at an annual rate that is 5 times that. Everything is easier with the wind at your back, and the wind behind the cannabis sector is five times stronger.

Future Growth—White Label Getting a Royalty On U.S. Cannabis Growth

All the growth avenues I just told you about are happening right now. But in the future, there is a white-label opportunity in areas of the USA where Icanic is not selling its own brands.

As pre-rolls become more mainstream with a consistent product—from automation—any other producer could license the intellectual property from Icanic Brands if they want to become a volume leader in their state.

There are several potential business models around this play. One would be an upfront sale and royalty thereafter. Having a royalty on one of the fastest-growing industries in North America would be a great seat to have.

Or, Icanic could go into a state and operate the machine itself and have the revenue stream be 100% royalty-based.

Before I wrap up here, I do want to say I'm very impressed with CEO Brandon Kou. He has a deep background in marketing and administration.

He has not only built up a huge network of over 350 outlets in his distribution network—to get product on the shelves—he has a marketing team with reps that help retailers get his product off the shelves.

So he is now in a great position to consolidate other brands. He can give them immediate and large distribution (greater revenue) and automated production (lower costs), making any merger-and-acquisition (M&A) deal even more accretive, very quickly.

And to top it all off, several of the key shareholders that helped incubate and finance CloudMD (DOC:CSE; $0.26–$2.70 this year) are shareholders here. Sponsorship counts for so much! Everyone wants to follow a winner. Winners create winners.

In conclusion, I am long this stock. I want to own it before the U.S. presidential election, and I want to own it before the year-end financials come out—which only go up until July 30.

I'm intrigued that their automation started the same month they reported their first positive net income, and now I'll get to see what an entire quarter (Q4) financials look like with the 1,000-stick-per-hour machine operating.

Top-line revenue is already up strongly in the first nine months. I think this could be an inflection point for the company. That's why I'm long, that's why I'm excited.