Like many cannabis stocks, Tilray has had a difficult past few months. The company has been struggling to raise capital, meanwhile management sold large positions of the company as the stock was falling. The lack of confidence management has demonstrated along with the recent performance makes many investors concerned.

Shares of TLRY took a tremendous fall in a very short time when the initial COVID-19 shock hit the markets. The stock fell from $20 to $2 in just a few weeks, which is a 90% drop. Since then TLRY has bounced back from its lows of $2 to trade in the mid $6 range. This represents an almost 300% increase from its all-time lows, but many investors are wondering if this level is sustainable?

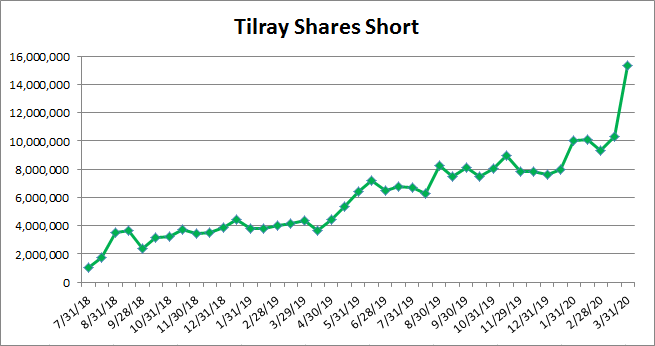

First, let’s talk about short interest in the stock. Just a few months ago there were over 10 million shares of TLRY being shorted, now that number has climbed dramatically. Referring to the chart below, we can see that over the past month, the number of shares being shorted has skyrocketed by 50% to over 15 million.

This data paints a grim picture which indicates that 1 in every 7 shares of TLRY is being held short. This increased short interest is a big red flag as it signals that even at these prices, short sellers feel that TLRY will be heading lower once again.

The total number of TLRY shares increased this past month after the company announced another capital raise. TLRY sold 7.25 million shares causing immediate dilution hence the share price decline. Along with the additional shares, TLRY sold pre-funded warrants to purchase another 11.75 million shares. Finally, they announced warrants for an additional 19 million shares. The total value of this offering came in at 90 million.

So things are not looking good for TLRY, especially in this environment where growing revenues will be a lot harder than before. Let’s take a look at what analysts have to say about the company.

Last week Jefferies downgraded TLRY to underperform from the previous rating of neutral. They also reduced their price target to $5 per share. Jefferies estimates that TLRY will post a net loss of $1.44 per share for this fiscal year and $0.80 in 2021.

A big part of the Jefferies’ downgrade has to do with its overall outlook on the Canadian cannabis market. Analyst’s Owen Bennett and Ryan Tomkins estimate that total sales in the country will be much lower than expected. They forecast CA$2.3 billion for 2020 meanwhile the general estimate sits at CA$3 billion.

The two analysts at Jefferies said, “We think the consensus is expecting too much from an industry where pricing is seeing real pressure and new product launches are unlikely to contribute meaningfully.”

Overall we believe that TLRY has a lot more to prove (earning profits and not diluting their shareholders) before new investors should consider getting involved. The current market conditions TLRY is facing, combined with the company’s lack of profitability, make them a highly risky and speculative investment.