In 1982 Congress created Section 280E of the Internal Revenue Code, IRC, which significantly limited the business expenses that a cannabis company could deduct. It states "no deduction or credit shall be allowed for any amount paid or incurred during the taxable year in carrying on any trade or business if such trade or business (or the activities which comprise such trade or business) consists of trafficking in controlled substances (within the meaning of schedule I and II of the Controlled Substances Act) which is prohibited by Federal law or the law of any State in which such trade or business is conducted."

The DEA has categorized marijuana as a Schedule 1 substance alongside, heroin, ecstasy and LSD enabling the IRS to apply 280E to cannabis companies. Numerous expenses that are normally deducted for federal tax purposes by companies are denied for cannabis companies. The list of expenses that cannot be deducted include advertising, marketing, bad debts, board meeting expenses, business association dues, vehicle expenses, charitable deductions, legal fees, office supplies, payroll processing, payroll taxes for employees (including Social Security, Medicare and unemployment taxes), parking, tolls, sales staff salaries and wages, equipment and repairs, furniture and fixtures, rent, home office expenses, insurance premiums, shipping costs, computer software and equipment, utilities, website, workers compensation, and many more things.

Losing Money AND Paying Taxes

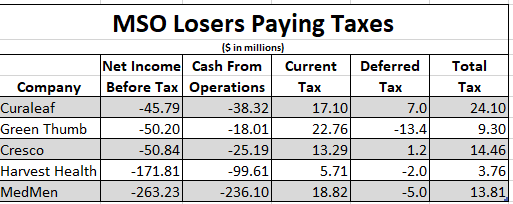

The IRS has created the incredible situation where cannabis companies are forced to pay federal taxes even though they are losing money and have negative cash flows. The following exhibit shows the tax liability for five of the largest multi-state-operators, MSOs, for their most recent fiscal years. It shows that all five had net losses before tax yet each had a current tax liability. Furthermore, each of the five reported negative cash flow from operations. These numbers vividly illustrate the inequity of cannabis company taxation. The numbers are astonishing and more like what might be expected in a totalitarian country not the USA.

Curaleaf (OTCPK:CURLF) lost $45.8 million but had a current tax of $17.1 million, Green Thumb (OTCQX:GTBIF) lost $50.2 million but had a current tax of $22.8 million, Cresco (OTCQX:CRLBF) lost $50.8 but had a current tax of $13.3, Harvest Health (OTCQX:HRVSF) lost $171.8 million but had a current tax of $5.7, and MedMen (OTCQB:MMNFF) lost $263.2 million but had a current tax liability of $18.8 million.

Since these companies have also had negative cash flow from operations, they have been forced to borrow money and sell stock to pay taxes to Uncle Sam for the privilege of losing money. What an absurdity? It's no wonder the stocks of these companies have performed poorly.

Corporate Tax Comparison

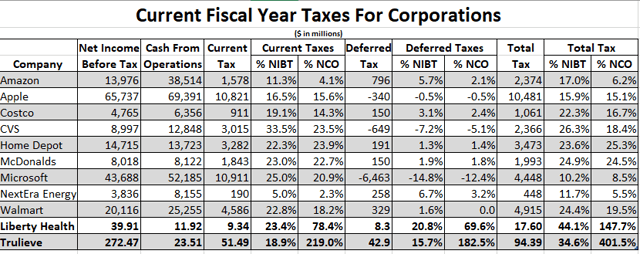

To determine how badly cannabis companies were getting treated by the IRS, I decided to examine several prominent non-cannabis companies against two cannabis companies with which I was most familiar. The following exhibit was constructed using data from the most recent 10K of each non-cannabis company and the most recent fiscal year Sedar filings of Trulieve (OTCQX:TCNNF) and Liberty Health Sciences (OTCQX:LHSIF).

Non Cannabis Company Taxes

The above exhibit shows that NextEra Energy (NEE), a/k/a Florida Power & Light, had the lowest tax rate. Its current taxes represented only 5.0% of its net income before taxes, NIBT. The non-cannabis company that had the highest current tax percentage of NIBT was CVS Health (CVS). Its current tax liability was 33.5% of its NIBT.

In ascending order Costco (COST) had a current tax liability representing 19.1%% of its NIBT, (Home Depot (HD) 22.3% Walmart (WMT) 22.8%, McDonalds (MCD) 23.0%, and Microsoft (MSFT) 25.0%. Interestingly, the two companies with stock market capitalizations in excess of $1 trillion had very low current tax liabilities. Amazon's (AMZN) current tax liability represented only 11.3% of its NIBT, while Apple's (AAPL) was 16.5%.

The above exhibit shows current taxes as a percentage of net cash from operations, NCO, ranged from a low of 2.3% at NextEra to a high of 23.9% at Home Depot. Importantly, current taxes of non cannabis companies as a percentage of NCO were lower than as a percentage of NIBT for every corporation except Home Depot. Every other non-cannabis corporation had cash flow from operations greater than their net income before taxes; therefore, their current tax liability as a percentage of NCO was greater than as a percentage of NIBT.

The top federal income tax rate for corporations during the time period studied was 21%. Among the non-cannabis corporations, Microsoft's total taxes (current + deferred) were the lowest as a percentage of net income before taxes at 10.2%, while CVS was the highest at 26.3%. In descending order after CVS were McDonalds 24.9%, Walmart 24.4%, Home Depot 23.6%, Costco 22.3%, Amazon 17.0%, and Apple 15.9%.

Taxes At Two Profitable Cannabis Companies

A comparison of Trulieve and Liberty Health data with the non-cannabis corporations shows their current taxes as a percentage of their net incomes are quite similar. The cannabis companies' current taxes are, however, a much higher percentage of their cash flows. In fact, the current taxes of Trulieve represented 219% if its cash flow from operations and Liberty's was 78.4%. The highest non-cannabis percentage was 23.9%, so it wasn't even close.

Deferred taxes as percentages of NIBT and NCO at Trulieve and Liberty represented much higher percentages than those observed for any of the non-cannabis corporations. The difference is largely attributable to cannabis companies blindly using International Financial Reporting Standards, IFRS, accounting instead of Generally Acceptable Accounting Principles, GAAP, since IFRS includes cannabis as revenue while it is growing.

When current and deferred taxes were combined, the total taxes of Trulieve and Liberty as percentages of NIBT and NCO dwarfed those of non-cannabis companies. A quick review of earlier year results showed identical results so it was not an aberration.

The data in the above exhibit clearly show that profitable cannabis companies that report positive net cash provided from operations report significantly higher taxes as percentages of net cash flow from operations and net income before taxes. This is the result of Section 280E denying cannabis companies normal business deductions.

Current Tax and the Cash Flow Statement

The traditional cash flow statement presented in audited annual reports is divided into three sections: Cash Flow From Operating Activities, NCO; Cash Flow From Investing Activities; and Cash Flow From Financing Activities. Of the three, NCO is the most important in valuing a business or a share of stock in a business, since it shows the amount of cash thrown off or available. It also shows the ability of a firm to fund itself. An ideal firm would show consistently growing sales and net cash provided by operating activities.

A cash flow statement begins with the net income after taxes obtained from the income statement. Taxes deducted from net income before taxes include current taxes as well as deferred taxes. Importantly, current taxes are assumed to be paid during the fiscal year being reported.

The difference between current taxes and the amount paid are entered as income taxes payable. If a company pays less than the current taxes shown on its income statement, the difference is recorded as a current liability and added as a line item in the cash flow statement.

The following shows an analysis of net cash provided by operating activities for seven of U.S. centric, publicly traded cannabis companies. They are listed in descending order based on their capitalizations with Curaleaf (OTCPK:CURLF) at $3.06 billion at the top and MedMen (OTCQB:MMNFF) at $73.8 million as the smallest.

It is noteworthy that only two of the seven companies, Trulieve and Liberty, show a profit and positive operating cash flow for their most recent fiscal year. Curaleaf showed a net loss after taxes of $69.95 million and a negative operating cash flow of $38.32 million; Green Thumb (OTCQX:GTBIF) had a NIAT of -$59.55 million and NCO of -$38.32; Cresco (OTCQX:CRLBF) had a net loss of $65.3 million and negative cash flow of -$25.19 million. Harvest Health (OTCQX:HRVSF) had a net loss of $175.57 million and a net operating loss of $99.61 million. MedMen (OTCQB:MMNFF) lost $277.05 million in its most recent fiscal year and also had negative operating cash flow of $236.10 million.

Interestingly, all of the above cannabis companies, except Trulieve, actually paid fewer taxes than they showed as current taxes. Trulieve actually paid more in taxes than they incurred during their latest fiscal year. Liberty's current tax was $9.34 million for its fiscal year ended February 29, 2020; however, it actually did not make any tax payment during its Fiscal 2020. Liberty, therefore, showed $9.34 million more in cash flow than it would have.

Tax Adjusted Cash Flow

The above exhibit adjusts actual cash flow to accommodate the actual payment of current taxes. If a cannabis company paid its exact amount of current tax incurred during the year then the net cash from operations would equal the tax adjusted cash flow. As shown in the above exhibit, the tax adjusted cash flow for Liberty was $2.58 million, which is $9.34 million less than the amount it reported, because that is the amount of tax it did not pay. On the other hand, Trulieve's tax adjusted cash flow of $26.33 million actually exceeded the operating cash flow it reported of $23.51, because it fully paid its fiscal year 2019 current tax of $51.49 million plus it paid an additional $2.82 million.

As previously noted, cannabis companies in the USA pay exorbitant amounts of tax because of expense deduction denials in IRS regulations. The sheer size of current tax liability incurred must therefore be carefully analyzed to determine its impact on net cash provided by operating activities. A company can increase its net cash provided by operating activities by simply not paying its current taxes just as Liberty did in its fiscal 2020.

Conclusion

It is clear that the tax code unduly punishes cannabis companies because IRC Section 280E denies such companies expense deductions available to all other legitimate corporations. This article clearly shows cannabis companies losing hundreds of millions of dollars but paying millions in income taxes. Taxes are a huge expense at cannabis companies and a primary reason why cannabis companies net such small percentages of sales revenue as profit and cash flow even though they are in an all cash business.

The cannabis industry needs to exert maximum effort to free cannabis companies from the onerous application of IRC Section 280E. A nascent industry needs encouragement not discouragement.

The IRS is effectively lowering cannabis company net income after taxes and cash flow and that weighs on the stock prices of companies in the cannabis sector. In the near future state and local governments will need additional tax revenue to sustain basic services and a healthy, growing cannabis sector can help meet that need via expanded legalization and less oppression by the IRS.

The top corporate tax rate of 21% is likely to be increased in the near future because of the soaring federal debt. Any such increase will be extremely painful for cannabis companies, which already have a much higher corporate. To soften the coming blow, cannabis companies must exert maximum effort to get out from under IRC Section 280E.