Historically, cannabis stocks have tended to move in unison. As the publicly traded cannabis sector evolves, though, we are beginning to see returns between various sub-sectors and even between the members within those sub-sectors vary from one another more than they have traditionally. The advent of more sophisticated investors, varying financial conditions among the companies and leverage to different drivers all suggest we should expect stock-picking to become increasingly important.

We break the cannabis sector into 10 different sub-sectors: Large American MSOs, Medium American MSOs.,Small American MSOs, Large Canadian LPs, Other Canadian LPs, Canadian Extraction LPs, Canadian Retailers, Ancillary Companies, CBD Companies and Biotech Companies.

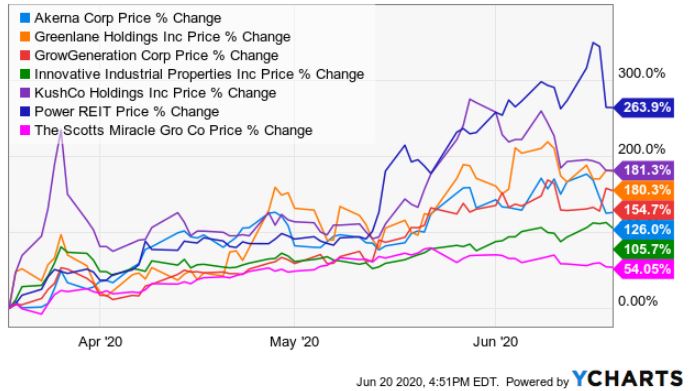

Since the market bottomed in March, Ancillary Companies has been the strongest sub-sector. The New Cannabis Ventures Global Cannabis Stock Index includes 7 companies that provide goods or services to the industry, or 20% of the overall number of constituents, a representation that has expanded significantly over the past year or so as new ancillary companies have joined while many of the direct cannabis companies have been removed due to no longer meeting the minimum criteria.

Since March 18th, the Global Cannabis Stock Index has increased by 81%. As the chart illustrates, the ancillary companies have been leading the way, with 6 of the 7 companies outperforming the index:

With the index down 27% in 2020, it’s worth noting that 6 of these companies have positive returns year-to-date.

We think that there are several reasons why investors are opting for ancillary companies over direct cannabis companies. First, most of these companies trade on the NASDAQ or NYSE, which greatly expands the investor base. Second, many investors are seeing the ancillary companies as a way to get diversified exposure without having to bet on individual operators. Third, several of these companies are profitable, with some even paying dividends. Finally, these businesses are substantially less capital-intensive than direct cannabis operators.

We have been surprised by how slowly the public ancillary space has evolved to date, but we expect to see more companies in the future. Several SPACs have raised substantial capital that they can deploy only into ancillary or CBD companies. We are aware of private REITs considering going public as well.

One company apparently working on going public is behemoth Hydrofarm, an independent wholesaler and manufacturer of hydroponics equipment and grow lights. Earlier this year, it filed a Form D with the SEC indicating that it had raised $23.5 million from 18 investors as part of a $50 million private placement of equity. In December, it reported that it had sold over $7 million in convertible debt through a private placement directed by Aegis Capital. In late 2018, it reported that it raised $55 million in a private placement that included Serruya Private Equity and other investors.

We note that Scotts Miracle-Gro recently upped its guidance for its Hawthorne Gardening division, suggesting sales this fiscal year could be about $1 billion, up 45-50% from a year ago, and this type of headline in November could attract additional investor interest in the ancillary space.