HEXO (HEXO) couldn’t have picked a worse time to announce a delayed filing of FQ2 numbers. The stock market is in the midst of a melt down and any perceived bad news is going to crush any stock. The good news was a revenue beat for the quarter and the delayed filing for an asset impairment charge isn’t necessarily impactful to the investment story.

Delayed Filing

On March 17, HEXO announced a delay of the FQ2 financials due for the quarter ending January 31. The filing was due on March 16.

The cannabis company blamed the delay on needing more time to finalize a large impairment charge and update disclosures to the MD&As based on romments from the Ontario Securities Commission.

The company forecasts reporting an asset impairment charge of C$265 million to C$280 million. With the state of the Canadian cannabis sector and the asset write downs from other companies in the sector, no investor should be surprised by this move.

HEXO ended the October quarter with C$330 million of property, plant and equipment with another C$235 million in intangible assets and goodwill and inventory at C$85 million. These asset levels are very high for their revenue base.

These moves are always made after a stock has been crushed and are more reflective of the current market environment and not related to future growth opportunities.

In addition, the company plans to sell their Niagara facility to completely pull the facility out of future production plans. Closing the facility for good isn’t surprising considering the market shift to outdoor production and HEXO producing 16k kg in the last few quarters while only selling slightly above 4K kg per quarter.

Promising Sales

The key figure in the press release was the release of gross sales at C$23.8 million with net sales at C$17.0 million. The net revenues grew 17% sequentially from C$14.5 million in the prior quarter.

The net sales number is key as HEXO has only reached a previous quarterly high of C$15.4 million back in FQ4. The amount was even slightly above analyst estimates.

In normal market times, the market would’ve celebrated these sales numbers likely boosted from the shift to a value brand late last year before the cannabis market officially shifted. The market will definitely want to see how expenses were constrained in the quarter along with an update to gross margins with the new value brand likely leading the way in sales growth.

The initial numbers provide some encouragement that HEXO was on pace to meet goals for substantial revenue growth throughout 2020 as new stores rollout in Canada and Cannabis 2.0 products reach the market. The coronavirus could shut down the momentum in the current quarter.

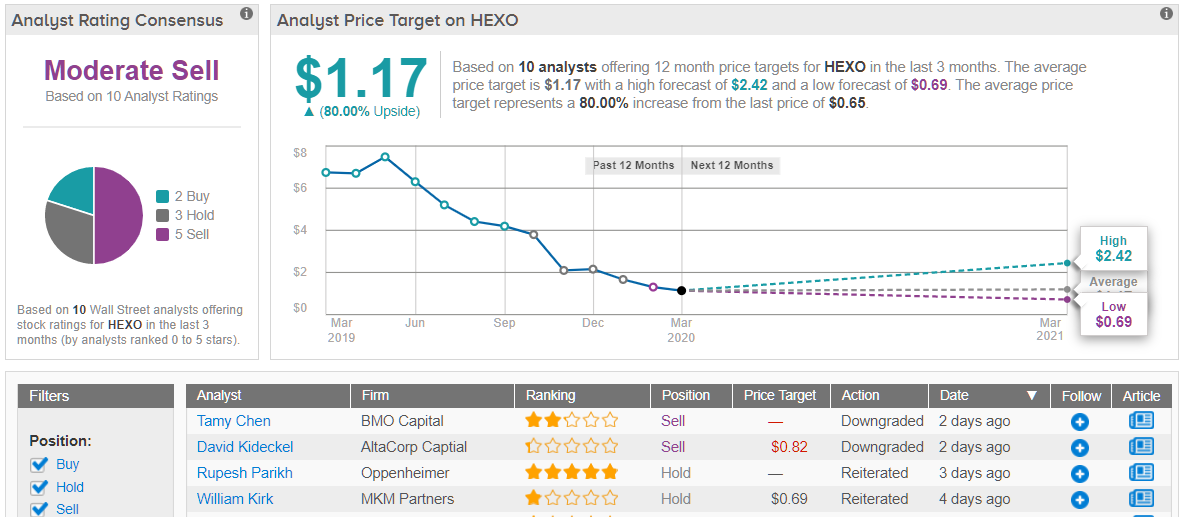

Consensus Verdict

The consensus price target of $1.17 shows a double-digit upside, but based on all the ratings received over the past three months, the consensus rating on HEXO is a Moderate Sell, at least according to TipRanks. While 2 analysts are on the Buy side, 3 say Hold and 5 advise investors to abandon ship.

Takeaway

The key investor takeaway is that HEXO got beaten to a pulp due to a delayed quarterly filing, but the company beat on key revenue figures. HEXO is clearly hitting a point where the company is finally achieving real momentum in the market.

As Canada gets beyond the coronavirus crisis that has already caused Canopy Growth to close stores, HEXO is a stock to own.