We penned an article on how we view gold's long-term and short-term cycles at present. At present, we believe gold is trying to confirm a new daily cycle which will most likely be the last daily cycle of this broader intermediate cycle. This pending ICL (which should go a long way in resetting sentiment) should be the next long-term buying opportunity in the metals (at least until the next yearly cycle low).

We reiterate our standpoint that the best way to play this bull market is to hold a core set of long positions until the bull market is over and add to these positions on weakness. Another strategy that active traders can deploy is to trade mining stocks which have plenty of volatility. Strategies such as the covered call nullify the cycles approach to a large degree because one can have both long and short deltas working in the respective trade simultaneously.

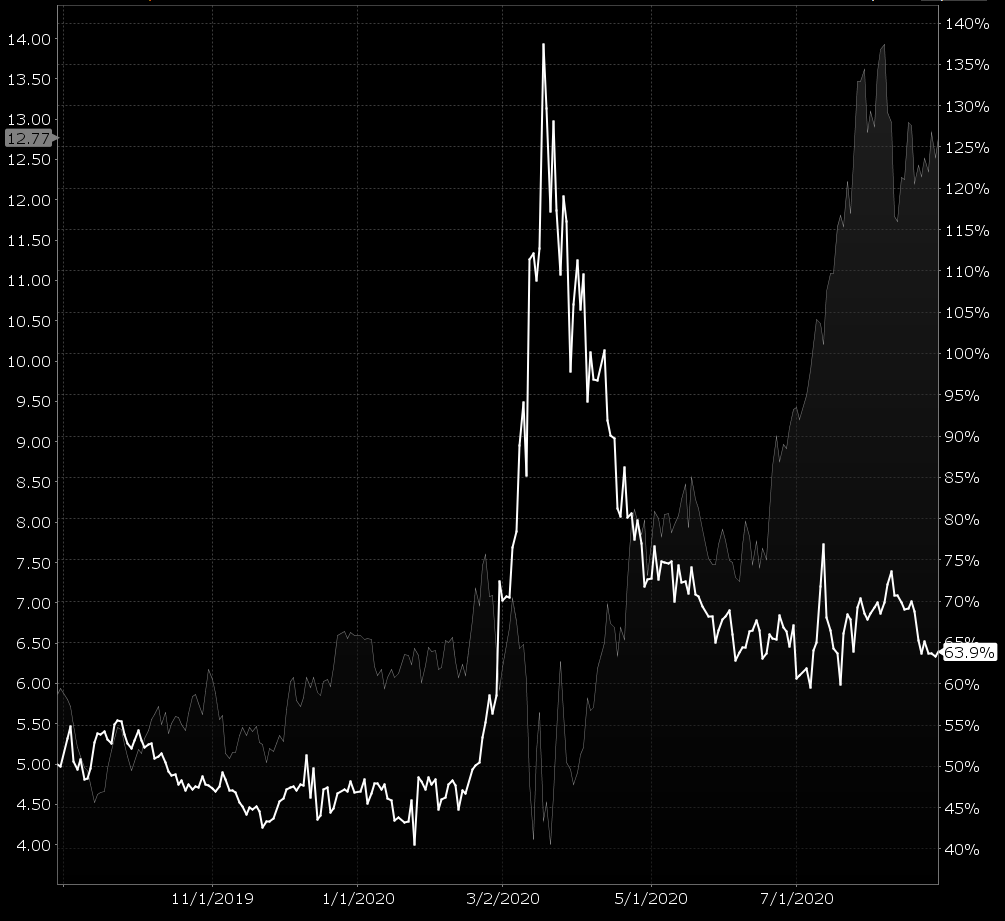

One such stock in this space, which is ripe for selling option premium as this bull market matures, is Gold Fields (GFI). As we can see from the chart below, its present implied volatility is well above the 60% mark. A number as elevated as this gives traders the opportunity to sell option premium which, in turn, results in positive theta. Remember, all option contracts become worthless at expiration which means option decay automatically works on a daily basis in favor of the option seller and works against the option buyer.

With a covered call, although one is collecting premium from the option sales, the downside is still associated with holding stocks. Therefore, let's delve into Gold Fields to see if there are potential downside risks here over the medium to long term.

First, we turn to Gold Field's valuation. Although Gold Fields continues to generate plenty of cash flow, its assets (P/B of 3.84) and sales (P/S of 3.14) are well above the averages in this sector. Since earnings growth is the primary driver of share price growth, the book and sales multiple are the most important valuation metrics for the following reasons.

- Assets or essentially mines in this sector are what essentially create earnings. The cheaper one can buy Gold Fields mines, the more potential for earnings growth

- Sales also have a huge impact on earnings. When there are plenty of sales, cost-cutting makes a favourable impact on the bottom line.

However, we would make the case that the valuation of firms (in a clear bull market) is not the potent ally that many believe. On the contrary, investing in "value" makes tons of sense when investing in firms that the market is clearly punishing. Gold Fields though is up 90% since the start of the year and 96% over the past 6 months alone. Shares, clearly, have momentum on their side where 52% bottom-line growth is projected this year followed by 69% growth in 2021. These are excellent expectations as gold finishes its bull run.

From a profitability standpoint, Gold Fields also compares favourably with its peers. EBIT margin of 28.7% over a trailing average is one of the highest in this sector. The miner's return on total capital (TTM) of 11.7% is also an excellent number. The ROC metric is used best not merely from a standalone basis but also against other miners in this industry (4.63% is the average). This profitability metric is essentially a read on how well Gold Fields has been converting its capital into profit.

One thing that value investors should remember is that mature companies with mature mines normally find it much easier to increase earnings due to the infrastructure on-hand. Therefore, it will be interesting to see how effective management will be with the significant amount of cash flow expected to be spun off over the next 12 months.

Therefore, to sum up, as we finish out the end of this bull run, it will not necessarily be the cheapest stocks with the strongest balance sheets for example which will outperform in our opinion. Alternatively, it will be the firms that are growing their earnings robustly. In fact, if one still wants to be ultra-conservative with their mining picks, Gold Fields does not look that expensive when one looks at the firm's much cheap forward multiples. Our focus remains on liquidating positions at gold's 8-year cycle high. We will make a decision here shortly.