Summary

- As we enter 2021, it appears that Buffett had things upside down in 2020.

- The things which had gone up the most by the end of 2019, went up the most in 2020.

- We invest on behalf of clients who want to avoid stock market failure and history shows most investors are impatient and are like a car stalled on the railroad tracks.

"The stock market is a device which transfers money from the impatient to the patient."-Warren Buffett

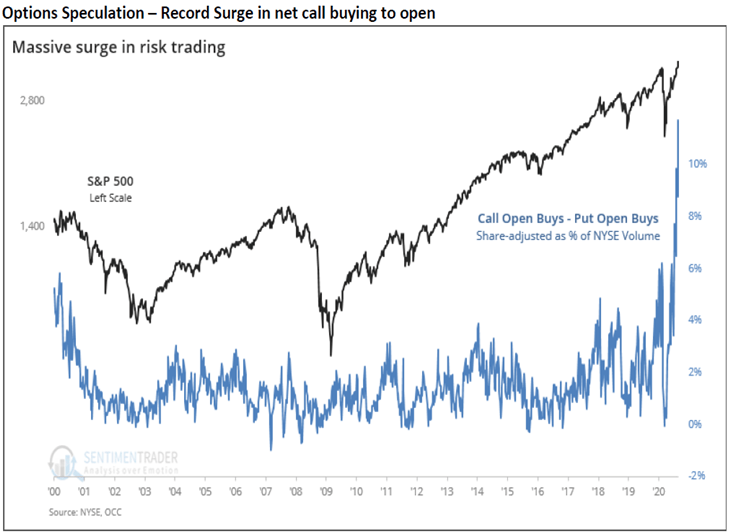

As we enter 2021, it appears that Buffett had things upside down in 2020. The things which had gone up the most by the end of 2019, went up the most in 2020. We invest on behalf of clients who want to avoid stock market failure and history shows most investors are impatient and are like a car stalled on the railroad tracks. A picture of the most impatient investors/option traders tells the story:

Fortunately, it is for these critical junctures in the stock market which disciplines like ours were created. First, we believe valuation matters dearly. It didn't matter in 2020, in fact, you were better off to buy the most expensive securities carrying the highest possible risk during the year. Historically, valuation is a driver of alpha and usually makes a roaring comeback when a "frenzy" (like Charlie Munger describes today's stock market) breaks and shifts the capital to those who are patient.

Second, we want to own companies for a long time. Our average holding period is about six years. This keeps trading costs down, capital gains taxes low and causes us to ride winners to a fault. Peter Lynch always talked about ten-baggers, stocks which go up ten times what you paid for them. He argued that you were the most likely to stay with a company that had something about them which stopped the shares from getting wildly popular and into impatient hands. His favorites were Philip Morris and Fannie Mae, one a vilified tobacco company and the other a misunderstood financial firm. We own some disrespected winners like eBay (EBAY), Amgen (AMGN), Bank of America (BAC) and Lennar (LEN), which fit that criteria.

Since 2011, when they started their dividend at 28 cents per quarter, Amgen (AMGN) has gone up from $52 per share to around $226 on December 31, 2020. Their dividend for next year is declared at $1.76 per quarter or $7.04 per share per year. This means a buyer at the time of the original dividend announcement at around $52 per share is getting close to a 14% cash on cash payout from dividends ten years later. From all you retirees out there, can we get an Amen? Did we mention that Amgen is trading for an incredibly reasonable 2021 estimated price-to-earnings ratio (P/E) of around 13 and has never been this cheap relative to the S&P 500 Index's forward P/E the entire time we've owned it?

Lastly, to hold for a long time, our companies must be very high quality. Among our eight criteria are wide moats, strong balance sheets, long histories of success in profitability and free cash flow generation. We also seek strong insider ownership and are very excited about the jockeys who are riding our long duration common stock horses. It's funny, but among the most popular stocks of 2020, people are very excited about their leaders (Bezos, Musk, Hastings, Cook, Zuckerberg, etc.).

"Envy is a really stupid sin because it's the only one you could never possibly have any fun at."-Charlie Munger

We remember the carnage leftover from the last euphoria episode in 1999-2000 and surprisingly are not envious of our growth fund/ETF competitors who wiped the floor with us in 2020. History argues that their potential stock market failure is in the nearer future rather than in the distant future.

This doesn't include the leaders of the most egregious IPOs, SPACs and glamour stay-at-home stocks like DocuSign, Peloton, Snowflake, Shopify, DoorDash, etc. Just tune into the stock market channels each day and another one of the CEOs of these wonder/frenzy stocks will be interviewed. They all should bring a bat with them to the interview, because rather than getting grilled, all the media throws these glam player CEOs are softball questions. If you want to talk hardball, just watch what they ask any value stock picker when they are on. They get nothing but questions like, "When is that going to happen?" Maybe, they should ask some of the whiz-bang CEOs when their bubble is going to break? We've ended 2020 at the polar opposite of Buffett's impatience quote, by glamourizing the impatience which the stock market normally crucifies!

In conclusion, our discipline trades at earnings multiples and dividend yields very similar to our strategy's history and gives us great confidence that these core tenets will play heavily in our favor over the next five to ten years as the capital moves from the impatient investors to the patient investors.