The total market capitalization of the top 100 cannabis stocks recently was $54,290,564,869, with Aurora Cannabis (ACB) alone accounting for $13.5 billion. Many investors look for industries that are growing exponentially, so that they can get into the proverbial "ground floor". Such industries can result from new technologies, such as the internet. Another source of exponential growth can occur when something that had previously been illegal becomes legal. Three major examples of such occurrences have taken place in the last 100 years. These were the repeal of the 18th Amendment, which ended prohibition in 1933, the expansion of casino gambling starting with the approval of casinos in Atlantic City, New Jersey in 1976 and the legalization of recreational cannabis by Colorado in 2014.

A year ago, if the word "epidemic" appeared in the news, it mostly referred to the opioid epidemic. Opioids were involved in 46,802 American overdose deaths in 2018. The nexus between the opioid epidemic and cannabis is that legalization of recreational cannabis has been shown to reduce opioid deaths by about a third. The legalization of recreational cannabis by Colorado in 2014 and other states since then, has provided enough data for academic researchers to determine that the reduction in opioid deaths resulting from the legalization of recreational cannabis is very statistically significant. This evidence would tend to support legalization of recreational cannabis in those states that have not yet done so. At least, among those who can be influenced by peer-reviewed scholarly research results.

An interesting result from the research is that just legalizing medical cannabis does not result in a statistically significant reduction in opioid deaths. An explanation for this result may be seen in the typical media accounts of particularly heart-breaking opioid overdose deaths. Many of the news stories involve someone who years ago had a drug abuse problem, but who had apparently been drug-free for many years. This person's friends and relatives were very proud that the person had turned their life around and now had a good job and family. Then the person is found dead on the floor from an opioid overdose.

The reason that researchers found that, after accounting for all variables, opioid deaths are so much lower in jurisdictions with legal recreational cannabis, is that some people who might otherwise use opioids are using cannabis instead. No one has ever died directly from a cannabis overdose. For someone trying to conceal their drug use from the world, getting a prescription for state-legal medical cannabis could be problematic. This raises the question of why the person in the story did not use cannabis instead of opioids? Presumably, who ever sold the illegal opioids to the person could likely have provided the person with illegal cannabis as well. However, illegal cannabis may not be a substitute for opioids for someone trying to conceal their drug use. Illegal cannabis is generally sold as flower to be smoked. Because of the smell and factors such as reddening of the eyes, smoking is difficult to conceal from those people close to one. State-legal recreational cannabis is sold either as flower or in edible form. Edible cannabis use is as easy to conceal as opioids. Thus, legalization of recreational cannabis can reduce opioid deaths by about a third, but legalizing medical cannabis has no statistically significant reduction in opioid deaths.

That the legalization of recreational cannabis has been shown to significantly reduce opioid deaths could be a positive for cannabis stocks. However, the COVID-19 pandemic may ultimately turn out to be more important for cannabis stocks. One thing that cannabis and alcohol after prohibition have in common, is the macroeconomic impetus to legalization. It is not a coincidence that the repeal of the 18th Amendment, which ended prohibition, occurred at the depths of the great Depression in 1933. In 1933 governments at all levels were desperate for tax revenue and the unemployment rate was above 20%. Prior to the enactment of the Federal Income tax in 1913, excise taxes on alcohol provided had about 40% of total Federal revenue. As tax revenues plummeted during the depression, the case for legalization and taxation of alcoholic beverages became much stronger. Arguably, the legalization of casinos in Atlantic City, New Jersey in 1976 was also a response by a government quest for additional taxes and jobs in a depressed jurisdiction.

One of the possible events that those bullish on cannabis stocks are hoping for, is legalization of recreational cannabis in New York. The governors of New York, and the other states that comprise the tri-state area, New Jersey and Connecticut, support the legalization of recreational cannabis. However, New York and to some extent the others have fallen into what might be called the "decriminalization trap". When simple possession of small amounts of cannabis is decriminalized, some of the impetus for legalization of recreational cannabis is diminished, as people are no longer imprisoned and burdened with criminal records for simple possession of small amounts of cannabis. Possibly more important is that decriminalization is the best of both worlds for criminal drug cartels and others involved in illegal cannabis. Under decriminalization 100% of the profits from cannabis go to the criminals and none to the government. Decriminalization also boosts sales for the criminals, since many of those who previously did not buy illegal cannabis out of fear that they could be imprisoned and burdened with a criminal record, now become potential customers for the criminals. Thus, the cartels and others involved in illegal cannabis have a powerful incentive to oppose legalization of recreational cannabis.

In the short-run, COVID-19 has hurt the American state-legal and the Canadian cannabis industry, as sales collapsed during the shutdowns of retail outlets. Legalization of recreational cannabis in New York and the rest of the tri-state area would be a great boon to cannabis stocks. COVID-19 and the severe economic downturn it caused, could provide the catalyst for legalization of recreational cannabis in New York and/or other states in the tri-state area. As was the case with casino gambling and lottery games, once something is legalized in one state, it eventually becomes legal in neighboring states.

New York Can Either Reduce Spending by $30+ billion or Auction 100 Cannabis Licenses

Estimates of the budget shortfall for state and local governments in New York caused by COVID-19 range from $30 to $60 billion. That does not count expenses and lost revenue resulting from recent protests and looting. Just the police overtime and lost revenue from boarded-up storefronts, would be a major budget problem for New York City in pre-pandemic times.

Ultimately, the biggest blow to New York state and local government finances, may be from the indirect impact of the Federal Reserve's dramatic reduction in interest rates. This vastly increases public pension obligations. Prior to that move, many state and local government pension funds were already underfunded. Moody's Investor Services had estimated that public pensions were underfunded by about $4.4 trillion. This is about the size of Germany's GDP. Aside from any impact on pension fund finances from lower investment returns, the lower risk-free interest rate vastly increases the present value of future obligations. As I said in Collateral Damage From Negative Interest Rates

…One can calculate the typical present value of a pension obligation, using the actuarial assumptions used in the New York City pension system for a 34-year old employee with 13 years of experience, and a salary of $80,000. If the current 7% expected rate of return and discount rate used by the New York City pension system is used and 2% inflation is assumed, the present value of the future pension benefits would be about $850K. However, now a better estimate of the risk-free interest, which is the correct way to discount the present value of future pension benefits, is about 1.75% rather than 7%. And if a zero-risk free interest rate is used, the present value calculation would be about $4.8 million. Were a negative risk-free rate of (1%) to be used, the present value calculation would be about $6.6 million…

Today, the risk-free treasury interest rate is much closer to zero, than the 1.75% that was the rate when the article was published. Ironically, in view of recent events, the calculation of the present value of that particular individual pension was prompted by a large settlement that New York City paid resulting from a death caused by a police officer's use of choke-hold. Comparison of the amount of the settlement paid by the city to the amount of present value of that particular police officer's pension, suggested that the city actually came out ahead since the gain to the city when police officer was mostly stripped of his pension benefits for his role in the choke-hold death, exceeded the multimillion settlement paid to family of the victim.

So far, most New York State and local officials' plans for dealing with the budget shortfalls seem to be, to hope for money from the Federal Government. Maybe. Governor Cuomo and some others have mentioned legalization and taxation of recreational cannabis as a possible source of funds to address the budget shortfalls. However, it is always with a caveat that it is a complex issue. One way of speeding up the much-needed revenue is to simply copy much of what Colorado has done.

Colorado legalized adult cannabis in 2014. In 2019 $302 million in cannabis taxes were collected by Colorado. New York has more than three times the population of Colorado. Thus, just copying Colorado's laws would be expected to bring in more than $1 billion in taxes in New York. It would be possible to sell municipal bonds secured with cannabis tax revenue, as has been done with the tobacco settlement payments. However, a better idea would be to auction cannabis licenses. This would allow New York State and local governments to both get immediate funds and also have all of the recurring revenue from taxing cannabis.

The easy way to allocate the auction revenue between the state and other entities such as New York City, would be to actually have two auctions simultaneously. In order to be in the recreational cannabis business, an entity would have to have a license from both the state and the local government. This would allow any of the counties in New York to opt-out from legal cannabis by simply not participating in the auction. Obviously, a license for New York City would sell for much more than for one, in a small upstate county.

Auctioning 100 state and 100 local cannabis licenses could easily bring in more than $30 billion. As with New York City taxi medallions, the licenses would be transferable and some understanding as to the limit on future issuance would be required. The tax rates on cannabis sales could be set at Colorado levels, again with some limit on future tax levels and those with the initial licenses. To maximize the proceeds, the Dutch auction method could be used. This encourages buyers to bid very high since all winning bidders pay the same clearing price. We are now in a frenzy of investors trying to get in on the ground floor of legal cannabis. This is similar to what happened with casino gambling, after Atlantic City was the first non-Nevada jurisdiction to allow casinos. As with the casinos, some investors did well with well managed companies. Some investors and lenders lost everything as with the Trump Casinos. The big winners were the governments who collected billions in casino taxes.

In New York and other jurisdictions, cannabis legalization has been delayed by the issue of social equity, which is the concept of reparations for those harmed by the war on drugs, many of which were minorities. My view is that, unlike slavery, where no direct victims are still alive, reparations for those harmed by the war on drugs should be handled with a commission like the 9-11 or Deepwater Horizon oil spill settlement. Those imprisoned for drug offenses, or that suffered in other ways, could receive certain payouts as could the children of those who suffered when their parents were imprisoned. The dire fiscal straits that New York and other state and local governments find themselves in, as a result of COVID-19, could hasten a resolution of the social equity issue and remove it as an impediment to cannabis legalization. This could be very good for cannabis stocks.

Previous Analogies and Parallels to Cannabis Investments From Gambling and Alcohol

Three major examples of legalizations spurring investment frenzies have taken place in the last 100 years. These were the repeal of the 18th Amendment, which ended prohibition in 1933, the expansion of casino gambling starting with the approval of casinos in Atlantic City, New Jersey in 1976 and the legalization of recreational cannabis by Colorado in 2014.

In each case there was a spectacular growth in the revenues for the firms involved in those industries. There was much speculative investment activity in the shares of the firms involved. Some of the investments did very well, others not so much. As with the dot-com bubble and subsequent bust, many speculative investments were terrible but some, such as Amazon.com, Inc. (AMZN) have done extremely well. Some analysts think that AMZN could be the first company with a $2 trillion valuation by 2023.

The dangers of investing in new companies taking advantage of the legalization of a good or service that was previously illegal, were shown dramatically in the 1930's with the downfall of Richard Whitney. He was the president of the New York Stock Exchange from 1930 to 1935. Whitney invested heavily in Distilled Liquors Corporation, which was organized to produce liquor as soon as repeal the 18th Amendment became effective. The Distilled Liquors stock rose from $15 to a peak of $45 in the spring of 1934. From there it declined and Whitney bought more on the way down. Eventually, when his firm, Richard Whitney & Co. failed, Whitney, his firm and its partners owned 93% of the outstanding shares in Distilled Liquors. Whitney embezzled funds to cover his investment losses. He was convicted of embezzlement and sentenced to 10 years in prison. On April 12, 1938, six thousand people turned up to watch as Whitney, a scion of the Wall Street Establishment was escorted in handcuffs by armed guards onto a train that delivered him to prison.

The legalization of alcoholic beverages provides some historical analogies and parallels, with regard to investing in the stocks involved, to the legalization of cannabis. However, the expansion of casino gambling outside of Nevada may be more relevant, in some respects. Repeal of prohibition took place at the Federal level, and mostly impacted much of the entire country at once. The expansion of casino gambling outside of Nevada, was done on a state by state basis, as is the case today with the state legalization of cannabis.

Once repeal the 18th Amendment became effective, developments at the federal level were not of much concern to investors in alcoholic beverage related securities. However, the fortunes of the gambling industry are still somewhat tied to policy and laws at the federal level. The status of sports betting and internet gambling has been in flux at the federal level for many years and is still evolving. Clearly, the biggest variable risks and opportunities regarding investing cannabis stocks are developments at the federal level. When he was running for president, Gov. Chris Christie said his administration would use federal rules that outlaw marijuana to clamp down on states that legalized recreational pot use. The risk that an administration could completely destroy the state legal cannabis industry still exists. Likewise, formal legalization at the federal level would give a big boost to cannabis stocks.

States and some local governments do have laws and regulations regarding the production and sale of alcoholic beverages. However, in most jurisdictions anyone can enter the liquor business, by applying and paying for the appropriate licenses. Alcoholic beverages can generally be imported into the United States and shipped across state lines. In contrast, each casino that opened outside of Nevada involved extensive legislation and sometimes litigation on the state and local level. In that respect, the rollout of recreational cannabis is much more like casino gambling, than the repeal of prohibition. Also, each casino operation outside Nevada generally required a relatively large capital investment. Capital barriers to entry in the retail sale of alcoholic beverages are low. The amount of capital to start a small winery or microbrewery is generally less than the all-in cost of entering the state-legal recreational cannabis business, especially when legal and related costs are considered. Thus, the expansion of gambling that started in the 1970s and then proceeded on a state by state basis is probably the most useful, when analyzing the cannabis industry.

Data on Potential Cannabis Growth From Previous Legalizations

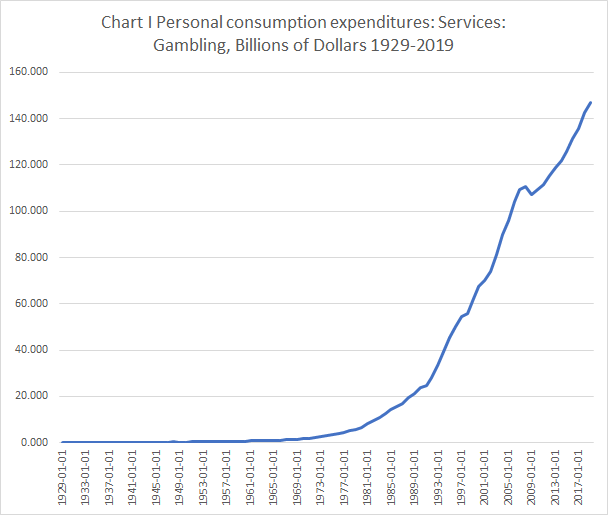

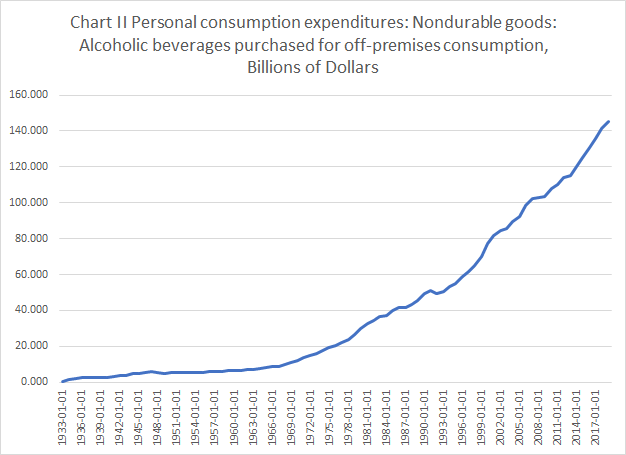

Various estimates have been made regarding the potential size of the cannabis market. The global legal marijuana market size is expected to reach $73.6 billion by 2027, according to a 2020 report published by Grand View Research, Inc. It is anticipated to expand at an annual growth rate of 18.1% during the forecast period. That seems reasonable. Historic data regarding gambling expenditures as additional states legalized new forms of gambling can give an idea of what can be expected from cannabis. Chart I below shows that in America alone, gambling expenditures reached $146.831 billion in 2019. Chart II below shows that in America alone, expenditures on alcoholic beverages purchased for off-premises consumption reached $145.147 billion in 2019.

The gambling expenditures data includes non-casino gambling, such as horse racing and state lottery games that also have grown. There is another national income and product account - "Total Revenue for Casinos Excluding Casino Hotels, Establishments Subject to Federal Income Tax," that would be more useful in isolating the impact legalizing casinos. However, that series is only available from 1998.

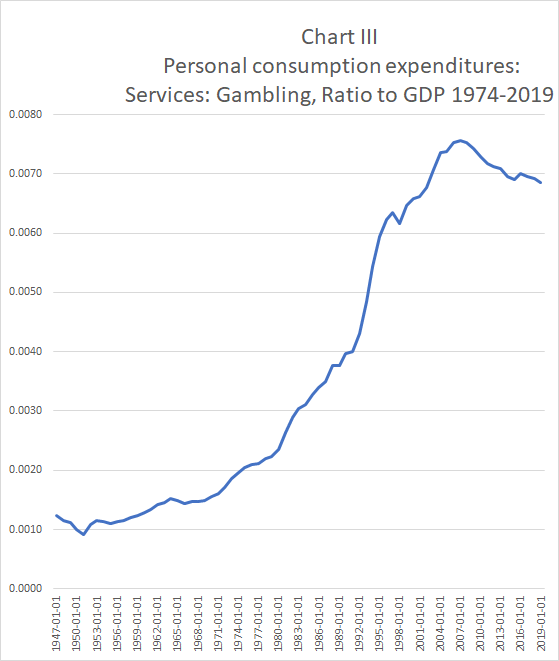

The dramatic increase in gambling expenditures from $0.036 billion in 1929 to $146.831 billion in 2019 was not all due to real growth in casino revenue. Some was from horse racing and lotteries. Of course, much of the increase was due to inflation and overall economic growth. There is not really a price deflator for gambling. However, to adjust for the overall increase in overall economic activity and focus on the impact that the expansion of casino gambling outside of Nevada that started in Atlantic City, New Jersey in 1976, we can examine the ratio of gambling expenditures to GDP.

Chart III below shows the ratio of gambling expenditures to GDP. That ratio grew modestly from 1947 to 1976. From 1976, as casinos proliferated growth was dramatic. However, it peaked in 2007 and has declined since then.

From an investment standpoint it can be useful to look at the total growth rate from when casinos outside of Nevada were first allowed, to when the market became saturated, the novelty wore-off in some areas and growth declined. The greatest profits from new industries are usually made by the earlier investors. As Warren Buffett famously said:

..there's a "natural progression" to how good new ideas go wrong. He called this progression the "three I's." First come the innovators, who see opportunities that others don't. Then come the imitators, who copy what the innovators have done. And then come the idiots, whose avarice undoes the very innovations they are trying to use to get rich.

Each progression cycle has its own specific characteristics. However, Buffett's model can be generally applied to everything from cryptocurrencies to casinos. Many investors did very well with casino securities. At the other extreme, everyone who ever bought any public stock or bond from any of Donald Trump's casinos, ultimately lost everything. That includes those who bought the mortgage bonds on Trump's casinos. It is quite unusual that mortgage bond holders have absolutely no recovery in a bankruptcy. I still own some worthless Trump Casino mortgage bonds. I also invested in the bonds issued by the casinos of the predecessor to Caesars Entertainment Corporation (CZR). After the Caesars bankruptcy, I received securities that are now worth more than the face value of the original bonds.

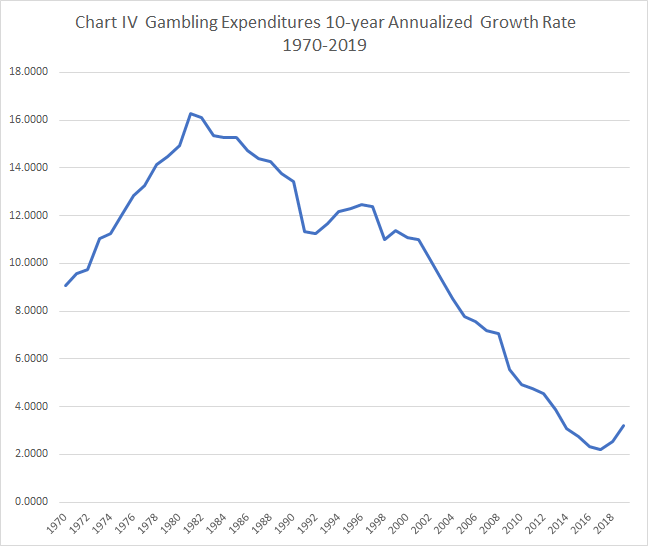

To see at what point an innovation or a legalization occurrence may be regarding Buffett's progression, it can be useful to look at the growth rates in revenue. Chart IV below shows the annualized growth rates in gambling expenditures over successive 10-year periods. As more and more states legalized gambling, the 10-year annualized growth rate peaked at 16.3% in 1981. After that, as the market matured, and the novelty may have worn-off, that 10-year annualized growth rate declined to 2.2% by 2017.

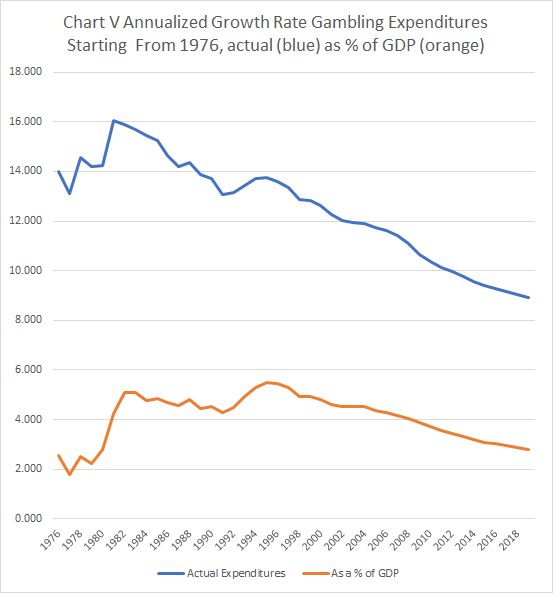

Another way of looking at what might be expected if cannabis stocks turn out to be the new casino stocks, is to examine absolute growth in the industry from just before the legalization occurrence. Chart V below shows annualized growth rate of gambling expenditures from 1976 to each subsequent year. This is proxy for the cumulative amount of growth of gambling from 1975 to each year up to 2019. This is shown both for the nominal amounts in blue and expenditures as a percentage of GDP, in orange.

The pattern is for rapid growth as additional states legalize new forms of gambling, then growth declines. Thus, from 1975 to 1981 gambling revenue grew at an annual rate of 16.1%. As a percentage of GDP from 1975 to 1981 gambling revenue grew at an annual rate of 5.1%. The wide variation in nominal GDP growth in the 1980's impacted the gambling as a percentage of GDP data. The growth of gambling as a percentage of GDP stabilized and peaked in 1995 around 5.5% and then gradually declined, but was still positive in 2019. Because of COVID-19, 2020 is likely to show a decline.

Conclusions and Recommendations

Cannabis is a product that has experienced rapid growth as a result of its legalization in various jurisdictions. If more states legalize recreational cannabis, further growth would be expected. However, there still exists considerable legal risks. There are numerous parallels between the cannabis industry and earlier legalization occurrences that may be informative for investors. During prohibition alcohol was legal in Canada but not in the USA. Today, cannabis is illegal in America at the Federal level, but legal in Canada. In 1933, the firms that were in the best position to profit from repeal of the 18th Amendment were based in Canada. Seagrams is an example. If New York and other markets open up, those cannabis companies already operating in other states or Canada will probably be in the best position to profit.

During prohibition legal exemptions were made for medicinal and sacramental alcohol. Today, alcohol sold for medicinal purposes is a miniscule part of the $145.147 billion expenditures on alcoholic beverages purchased for off-premises consumption in 2019. I think that medical cannabis will see a similar fate. Thus, I would avoid any company whose business plan depends primarily on medical cannabis on an ongoing basis. However, companies established in states where only medical cannabis is legal, may be in a good position to profit if those states were to legalize recreational cannabis, which is also referred to as adult-use cannabis.

The disparate results from investments in any of the Trump Casino securities, where investors lost everything, to the excellent returns from investments in well run casinos, suggest caution when investing in cannabis related securities. At this stage in the growth of cannabis, it may be too early to determine which cannabis stocks will be winners, just from analyzing financial results. At this stage selecting cannabis stocks may require looking for individual companies that have technological advantages. There are many patents that have been filed relating to cannabis. Actual patents and the owners of the patents, can be seen at US Patent Office website. As of June 9, 2020 there were 4,446 US patents issued relating to cannabis. I am in the process of reading patents and trying to see which of the public companies that those patents are assigned to may warrant further research as investment candidates.

This suggests diversification may be useful. With most brokerage commissions having been eliminated or negligible, even a small investor could invest in a large number of different cannabis stocks. There are also a number of cannabis ETFs. The table below lists nine cannabis related ETFs along with their total assets, average daily volume and recent price.

Those looking to get in very early on the next possible legalization investment, may want to be aware that recently a petition was submitted to the Oregon Secretary of State for a ballot initiative (IP 34) seeking to permit the use of the psychedelic drug psilocybin.

Cannabis ETFs

Symbol | ETF Name | Total Assets ($MM) | Avg. Daily Volume | Price |

$593.26 | 851814 | $13.75 | ||

$47.93 | 65488 | $10.74 | ||

$29.07 | 405 | $48.51 | ||

$21.08 | 48575 | $10.55 | ||

$12.30 | 27180 | $11.72 | ||

$10.87 | 8789 | $12.80 | ||

$10.21 | 4335 | $22.59 | ||

$8.37 | 526 | $41.76 | ||

$4.53 | 5040 | $11.34 | ||