Despite a lot of fears, Curaleaf (OTCPK:CURLF) has generally done what the Canadian cannabis giants couldn't do. The U.S. multi-state operator (MSO) has turned acquisitions into a market-leading position and a large EBITDA profit while the others have faltered. My bullish investment thesis remains intact as the MSO is poised to become the first cannabis company to top $200 million in quarterly sales with plenty of runway ahead.

Grassroots Key

Closing the Grassroots deal was important for many reasons. First, the company staked the business on the importance of grabbing the retail licenses in Illinois and Pennsylvania. Second, the management team spent a significant amount of time and effort over the last year attempting to close this deal with reputation risk ensuing by not closing the deal.

Ultimately, what matters is that Grassroots has access to key states such as Illinois that just approved recreational cannabis on January 1. Curaleaf estimates that sales jumped from $27 million in Q1 to $45 million in Q2 with significant growth forecasted in 2H. In total, Grassroots adds 57 dispensary licenses and 250,000 sq. feet of cultivation space.

The big proforma guidance for Q3 relies heavily on growing revenues from Grassroots. In addition, the management team needed this deal to perform from the beginning after Select was such a disappointment. Considering the company only paid an adjusted 119 million shares for Grassroots, the deal appears a bargain now. At the closing price around $7 for Curaleaf, Grassroots costs about $830 million with a 2021 sales target topping $300 million.

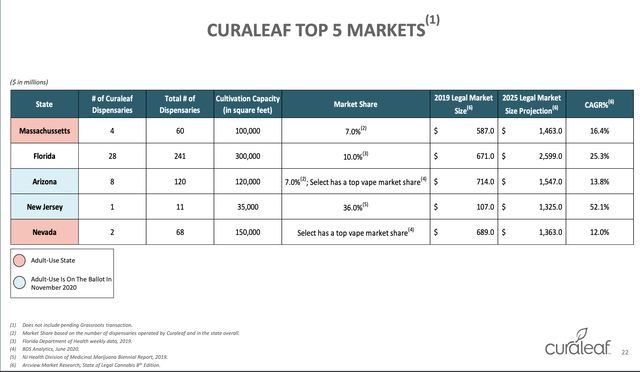

Even outside of the Grassroots expansion into Illinois and Pennsylvania, Curaleaf was poised to see substantial growth in other key markets such as Massachusetts, Florida and New Jersey. Their top 5 markets are forecasted to grow from 2019 legal market sales of $2.77 billion to a 2025 market of $8.30 billion for ~200% growth.

So the company has operations headed towards revenues of $210 million in the current quarter with massive growth ahead in key markets. Just about all of these markets such as Arizona, Florida and New Jersey are expected to approve recreational cannabis in the next few years.

In addition, the combined entity has 88 active locations with licenses for another 50 locations providing automatic growth. All while Curaleaf already has strong EBITDA profits. In Q2 alone, the MSO generated $28 million in positive EBITDA headed toward several hundred million in 2021.

Cannabis Value Play

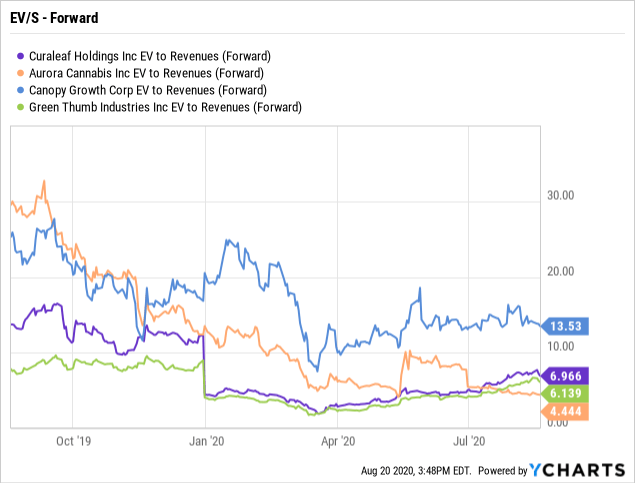

The cannabis market continues to love Canopy Growth (CGC), yet the real value is in the MSOs like Curaleaf or Green Thumb Industries (OTCQX:GTBIF). Currently, Curaleaf trades at about half of the Canopy Growth EV/S multiple of 13.5x. Aurora Cannabis (ACB) is an interesting valuation here, but the stock is still a higher risk having EBITDA losses and lacking access to the U.S. cannabis market.

Green Thumb is a slightly cheaper valuation here, but Curaleaf has the advantage of scale. Green Thumb just reported Q2 revenues of $119.6 million in comparison to the $210 million Q3 target of Curaleaf. Either stock probably does fine here, but my view is that Curaleaf uses size and scale to build a bigger brand awareness leading to higher long-term value.

My view generally aligns with the point from Executive Chairman Boris Jordan on the Q2 earnings call:

... aligns with our strategy to build nationally recognized brands. We take the long-term view that the cannabis industry will ultimately be much like traditional consumer packaged goods where trusted brands will be differentiating, defensible and value-creating in the long-term, continuing to capture higher margins and consumer wallet share.

Takeaway

The key investor takeaway is that Curaleaf still remains a bargain stock despite tripling off the COVID-19 lows. The MSO has substantial growth catalysts ahead and should trade at an industry premium having the largest revenue base.