The cannabis industry is seeing more interest from investors after the major sell-off over the past year. A lot of new companies emerged during cannabis legalization in Canada all wanting to cash in on ‘Green Gold’. Collectively, these companies produced far too much cannabis for what few Canadian dispensaries existed. Cannabis companies reeled from overbuilding and oversupply and subsequent lack of demand for their respective products. As mentioned, there was a major sell-off of these company’s respective stocks.

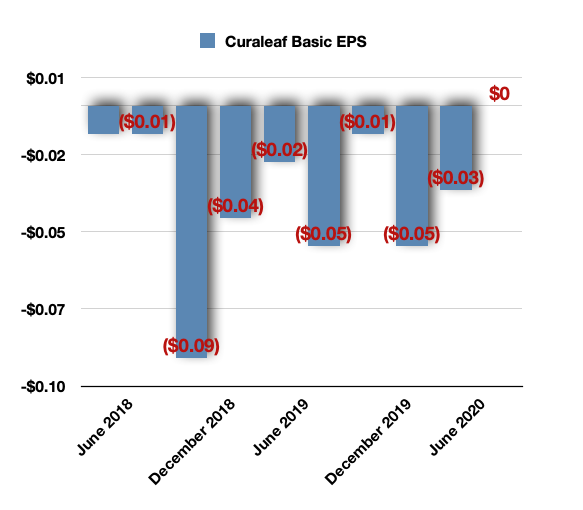

But, not all companies did poorly during that period of time. Notably, Curaleaf (OTCPK: CURLF) a company whose stock sold off during the past year is one of the largest producers of cannabis in the United States. They have operations in 14 different states in the country so did not get overextended during the Canadian build-up; they have no operations in Canada. They are a company that focuses on wellness aspects of cannabis and CBD, not necessarily the adult-use side of the business; albeit they have some products in this vein. Last quarter, the company achieved a break-even level and are poised to grow its revenue beyond the break-even point and become profitable.

Curaleaf stock will move higher.

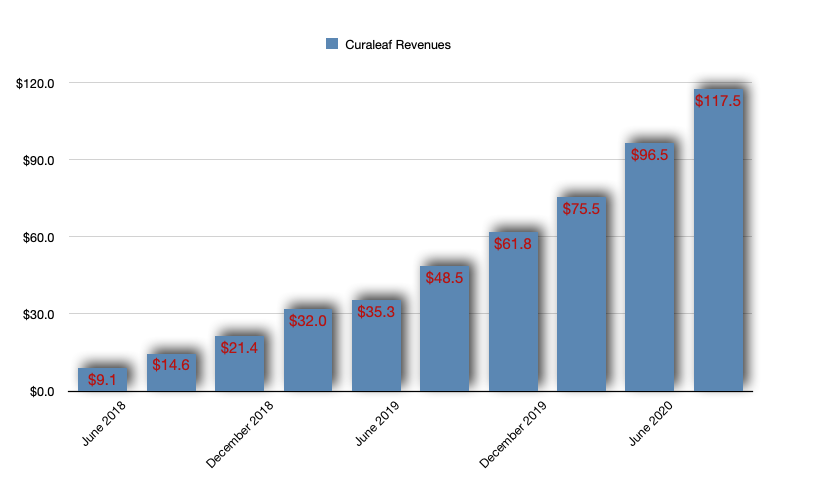

A Look At Revenue:

Revenues continue to grow upward with Curaleaf. This is good news as the company’s profits continue to get closer and closer to above break-even:

I will get into the EPS in just a second, but I wanted to point out a few things regarding this revenue. First, as someone who studied mathematics (Statistics) at the University of Denver, this is an impressive, near-perfect upward trajectory. You don’t see this often in finance. You definitely do not see this kind of revenue increase during a pandemic where the country was effectively shut down for retail business for a couple of months.

The quarter saw GAAP EPS at $0.00 which beat expectations by $0.03 per share. Also, the revenue of $117.48M was up 142.3% YoY and that beat expectations by $7.79M. Adj, EBITDA was $27.99M vs. $4.41M in 2Q19.

Mind you, the company achieved its break-even earnings as well as pushed its revenue upwards some 22% QoQ during the headwinds of the COVID shutdown. Now that the majority of the shut-downs have ended I expect this growth to continue.

However, there are two variables at play right now with COVID. First, Pfizer announced a drug with a 90% efficacy rate but, at the same time, a lot of governments are considering shutting down cities, counties, and states as they did before because of the large resurgence of COVID cases. Information to weigh.

However, the company continues to guide for further growth:

Even as the country continues to experience hotspots related to COVID-19 pandemic, we continue to expect significant and profitable growth in the second half of 2020. A key driver of building momentum into the second half of 2020 and into 2021 is material investments we have been making in expanding our cultivation capacity across our key markets.

Another thing that I want to point out is that there were a few other election victories that are notable in the United States that may help out any cannabis companies here in the states.

- Arizona approved recreational cannabis

- Mississippi approved medical cannabis

- Montana approved recreational cannabis

- New Jersey approved recreational cannabis

- South Dakota approved medical cannabis

This shows the acceptance of cannabis is becoming more widespread. And, with companies like GW Pharma (GWPH) and Charlottes Web (OTCQX:CWBHF), the former of which has FDA approved medication, gaining a great deal of ground with consumers and medical professionals, companies such as Curaleaf that deal with wellness cannabis will continue to see their revenues move higher and higher.

Curaleaf has operations in 14 states

Currently, Curaleaf has operations and/or dispensaries in these states:

- ARIZONA

- CONNECTICUT

- FLORIDA

- MAINE

- MARYLAND

- MASSACHUSETTS

- NEVADA

- NEW JERSEY

- NEW YORK

- NORTH DAKOTA

- OREGON

- PENNSYLVANIA

- UTAH

- VERMONT

Both the Arizona and the New Jersey passages will potentially affect Curaleaf immediately as they already have operations and can increase offerings. I’m looking at that as a potential major plus for Curaleaf.

Simultaneously, there is a lot of talk regarding the Biden victory and its effect on the cannabis industry in the United States. There is data - and an interesting presentation - that supports legal cannabis in the United States to reach $35B in the next five years. In 2019, the country spent some $80B on legal and illegal cannabis, of which $66B went to the illegal side with just $14B being legal. That would be a very respectable increase in revenue should the call come to fruition.

First, it was not a sweeping victory. Furthermore, the Senate is still up in the air. Because of that Senate “issue”, where McConnell may very well block any new changes to the Schedule I legalization, I am not exactly popping open corks on champagne bottles just yet. There are still a few more steps to take.

The country is not going to know the outcome of the Senate until the January run-off in Georgia. So, I do not see the Biden victory as anything all that intriguing just yet. Still, it is a step in the direction of continued legalization throughout the nation of which I am a big proponent.

Curaleaf stock fell along with most other companies in the cannabis industry in 2019. However, their stock did not fall as much, nor did it take too long to reach its previous highs. Here’s a look at the stock movement over the past two years:

Looking at this chart, you can see the selling that transpired in early 2019 and ended just a few months ago in March - April of this year, which occurred during the COVID shutdown.

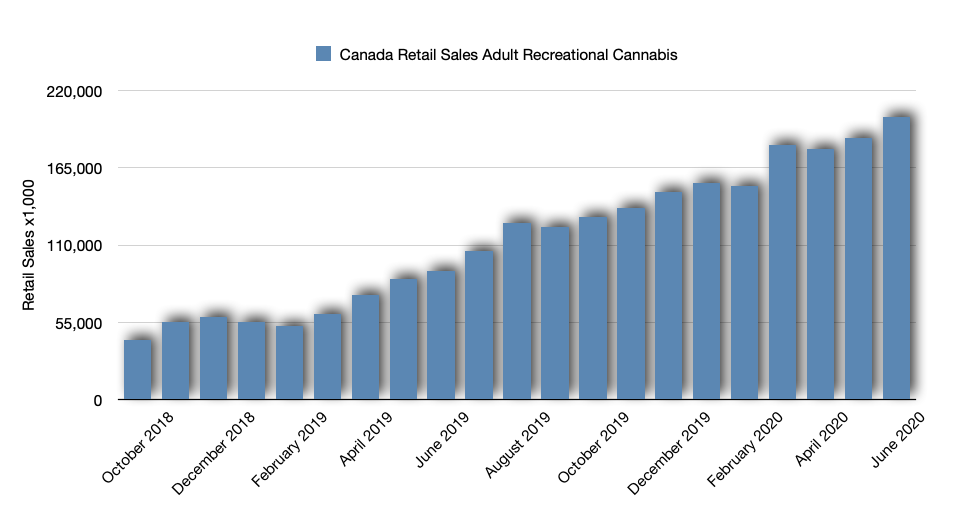

I mentioned that there is new interest coming into the cannabis sector once again. Companies are starting to see increased revenues, especially in Canada. The reason is simple: Canadian dispensaries are starting to roll out more and more as these dispensaries have cleared their regulatory hoops. Retail sales of Canadian cannabis are moving higher and higher.

Because of the increases in retail sales in Canada, this is translating into surprise upside earnings and revenues for Canadian companies. This interest is going to get investors back into the sector and I believe that we are already seeing that interest translate into a higher stock price for Curaleaf. Mind you, this chart is impressive for Canadian retail sales of cannabis. But, Curaleaf has no operations up in Canada. They are, however, in the overall sector. In fact, they are one of the largest producers in the United States and have the second highest capitalization just behind Canopy Growth (CGC).

Conclusion

With continued revenue growth as well as near break-even profitability, Curaleaf is in a very strong position. The company persevered through the pandemic-induced shutdown and came out with record profits. The legalization of recreational cannabis several more states where Curaleaf already has operations will provide the company with additional revenue potential. The idea that there is some potential legalization on the federal level may have legs, but I believe that is a ways off. Nonetheless, it represents a continuous pattern of acceptance by the country with the eventuality of total legalization.

I see a lot of reasons to own Curaleaf, a company that is poised for continued growth and on the verge of profitability. For these reasons, I am very bullish on the stock for a long-term holding.