Those who follow me know that I am long-term bullish on the cannabis space. But that does not mean I am bullish on every stock in the industry, like Tilray (NASDAQ:TLRY). While TLRY stock has done a great job bouncing off the 2020 lows, that alone does not mean it’s a buy.

In fact, investors who have been long this name may consider the recent rise an opportunity to exit the stock. Similarly, they may consider the more recent pullback in the short term as a buying opportunity to buy other cannabis plays.

In that regard, I am referencing stocks like Aphria (NASDAQ:APHA) or one of my favorites in Canopy Growth (NYSE:CGC).

Tilray Stock Lacks on Fundamentals

The cannabis industry as a whole has been going through a difficult stretch. However, some stocks are better equipped than others to make it through to the other side.

Take a look at Canopy Growth, which has a potent balance sheet and a more clear strategy for long-term success. It even has a potential acquirer in Constellation Brands (NYSE:STZ), which continues to exercise its rights to increase ownership.

In fact, when you think about those with the stronger balance sheets, they usually have a big-time, well-known company involved. Notice how Tilray doesn’t lean on its balance sheet strength.

While there is not an immediate concern that Tilray will be able to meet its short-term obligations, there is virtually no concern for Canopy Growth to meet its obligations.

Tilray has current assets of $338.9 million vs. current liabilities of $171.3 million. The former is about twice the size of the latter. However, compare that to CGC, which has current assets at more than six times the size of its current liabilities.

Is Growth Enough?

For a regular company, Tilray’s growth profile would be incredible. Analysts expect 42% revenue growth this year and an acceleration up to 55% growth in fiscal 2021.

However, recall that Tilray used to have fantastic growth. Just last quarter the company reported 126% sales growth. In prior quarters, 200% to 300% growth was present. So to see growth estimates of just 42% is rather disappointing — even as saying “just 42%” feels absurd.

That’s on top of the company continuing to lose money. Analysts expect Tilray stock to report a loss of $2.27 per share this year. While that would be better than the $3.20 per share it lost in FY 2019, it’s not something to brag about.

That’s particularly true as free cash flow continues to trail in the red. Unfortunately, this figure is moving in the wrong direction. In fiscal 2017, Tilray had free cash outflow of $17.4 million. In 2018 that figure ballooned up to $100 million before more than tripling to a free cash outflow of $336.8 million in 2019.

So is the growth enough? Not in my mind. Perhaps if cannabis becomes legal at the federal level, then these companies can start to really fly. But for now, the industry is struggling and I want to avoid its weakest players, like Tiray stock.

Bottom Line on Tilray

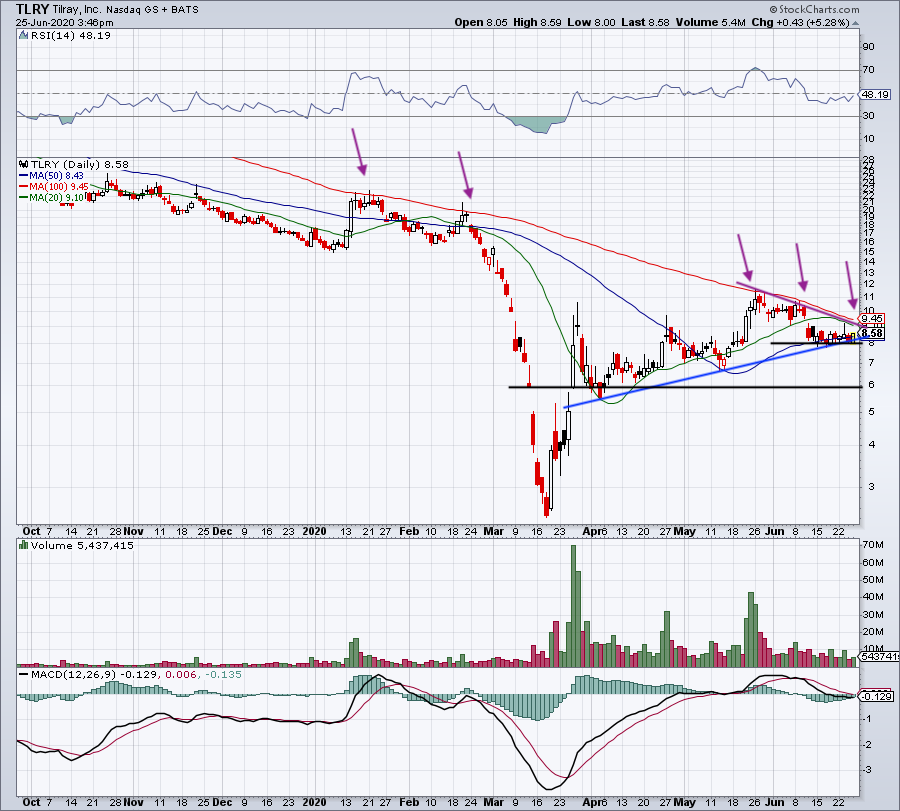

Surprisingly, Tilray stock has been trading in a tight range, spending the last two weeks between $8 and $9. But friends, remember this stock hit $300 at one point. While that move was mainly driven by a short squeeze, the fact that TLRY stock is down some 97% isn’t a sign that there are a bevy of buyers looking to scoop up shares.

The 100-day moving average continues to squeeze Tilray stock lower. It’s currently riding uptrend support while struggling to hold the 50-day moving average.

A close below $8 will be a very bearish development, potentially putting $6 or lower back on the table. Conversely, a close over the 100-day moving average is bullish. It would put the June high in play at $10.68, followed by the May high at $11.60.

Either way, the fundamentals aren’t bullish enough for me as the industry is in a period of struggle. Combined with muddy technicals (at best) and I will continue to avoid Tilray stock.