As the Canadian cannabis stocks continue to soar based on excitement over U.S. elections, the U.S. multi-state operators (MSOs) that stand to actually benefit haven't seen the same gains. Columbia Care (OTCQX:CCHWF) is one of the smaller under the radar names in the space that might eventually be attractive to a large Canadian company. This is one of the stocks investors should be buying on any enthusiasm over potential cannabis legalization in the U.S. due to the elections.

Big Opportunity

Back in early August, Columbia Care reported Q2 revenues reached $33.0 million while pro-forma revenues for 2020 were targeted at somewhere close to $250.0 million. Most investors probably haven't even heard of this smaller MSO while Aurora Cannabis (OTC:ACB) has far more analyst coverage while pro-forma results for the current year now have similar targets

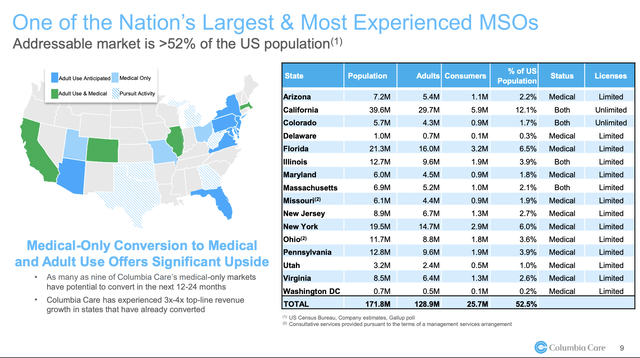

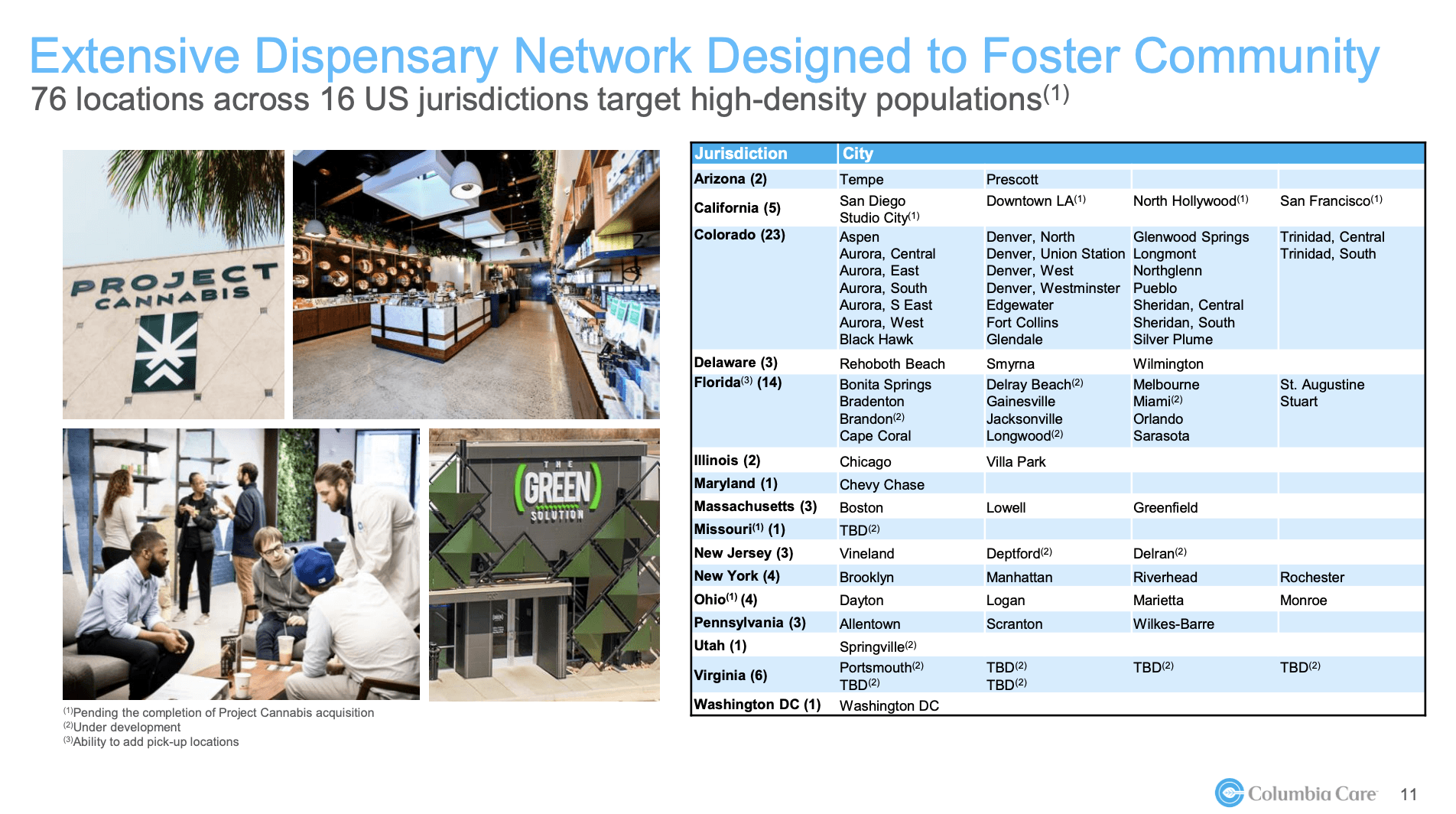

Columbia Care now offers an MSO with access to 97 dispensary licenses and 23 cultivation and manufacturing facilities over 16 states. The company is attractively positioned in states like Arizona and New Jersey that both just approved recreational cannabis providing substantial upside to existing sales levels. In total, Columbia Care has access to a total addressable market topping 52% of the US population while a company like Aurora Cannabis has a much smaller Canadian market with limited international medical cannabis exposure.

Outside of these new recreational cannabis markets, Columbia Care has stores in attractive markets like Florida, Illinois, New York (headquarters), Ohio and Pennsylvania. Of these key cannabis markets, only Illinois has already approved recreational cannabis providing further upside when these other states ultimately approve recreational cannabis in future years.

A lot of the revenue upside comes from closing the deal to acquire The Green Solution or TGS. The largest vertically integrated cannabis operator in Colorado offers a portfolio of 23 dispensaries and six cultivation and manufacturing facilities. TGS has 2020 revenue targets of $88.5 million and adjusted EBITDA of $18.5 million.

The deal only cost Columbia Care 33.2 million shares and $30 million in debt which amounts to only $163 million based on the current stock price of $4. The end result is some $22 million in quarterly revenues pushing the Q4 revenue target up to $52 million placing the company on par with most of the large Canadian cannabis operators that obtain far more media coverage due to trading on the major stock exchanges.

Basket Approach

When counting new dispensaries and acquisitions, analysts have the company pushing 2021 sales all the way up to $455 million. Not bad for a stock with a listed market valuation of only $1.1 billion and hardly known by the market.

One strategy to consider in the smaller MSO market is to take a basket approach. With higher risk stocks with limited operating histories, sometimes the best solution is to invest in multiple stocks to take out the risk of an individual company making missteps.

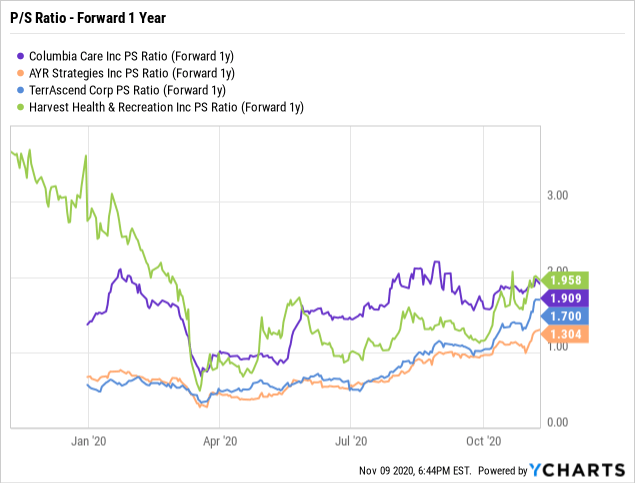

Investors can buy stock in multiple MSOs such as Columbia Care, Ayr Strategies (OTCQX:AYRSF), Harvest Health & Recreation (OTCQX:HRVSF) and TerrAscend Corp. (OTCQX:TRSSF) to spread out the risk, but participate in the potential upside here. All of these companies have 2021 analyst revenue targets topping $250 million with the P/S ratio below 2x.

In addition, anybody thinking a Biden team will legalize cannabis at the federal level should invest in U.S. cannabis stocks. These MSOs will likely be the direct target of Canadian cannabis companies looking to get into the U.S. cannabis space or other large public companies looking for an entry into the growing market. These companies offer market valuations in the $1 billion and below range more easily swallowed while potentially needing more access to deeper pockets and a strong partner to compete with the larger MSOs.

In the case of Columbia Care, the company lacks the scale to compete with Trulieve Cannabis (OTCQX:TCNNF) in Florida or Cresco Labs (OTCQX:CRLBF) in Illinois so a deal good provide a quick catalyst for the stock. Not to mention, access to public markets and further approvals of recreational cannabis would provide even greater upside potential for the stock.

These smaller MSOs could easily see the combined benefits on federal cannabis legalization hype in the U.S. of access to financial market followed by turning into acquisition targets. The end result would be much higher stock prices for cannabis stocks mostly unknown at this point, but companies that provide access to multiple states in one deal.

Takeaway

The key investor takeaway is Columbia Care is a prime stock to own for actual hype of federal legalization of cannabis with Joe Biden as President. The company would directly benefit from access to financial markets and further approvals of recreational cannabis at states with existing medical cannabis operations. The stock is too cheap at only 2x forward sales.