Cronos Group (NASDAQ:CRON) is not worthy of investment consideration at this time for reasons detailed in this article.

Investment Thesis

Cronos Group, Inc., which is among the most widely-held Canadian cannabis stocks, had a lackluster 2019 and has been under continued selling pressure in 2020. The stock currently trades at $5.55, which is down more than 80% from its 52-week high of $21.51 per Seeking Alpha. As I stated in my article of 1/8/20, I strongly believe that 2020 will be a very frothy market for all of the Canadian cannabis stocks for a variety of financial and operational reasons. A recent report that CRON has received an SEC inquiry into the company’s revenue recognition is a matter of grave concern, as detailed herein, the primary reason that I titled the article as I did. HEXO Corp. (NYSE: OTC:HEXO), my first code blue alert, is also a Canadian cannabis company, and is down more than 50% since my article of 1/8/20. Let’s take a look at what I consider bellwether events that support my base case that CRON faces a challenging 2020 from both a macro and micro perspective based on the company’s 2019 stock performance and the current landscape of the Canadian cannabis industry. As a point of information to the readers of this article, I consider the potentially devastating effects of the coronavirus as a clear and present danger but well beyond the scope of this article. However it is important to note that CRON has stated, “no assurance can be given that the anticipated timing of filing will be met due to the impact of COVID-19, as well as the need for the Company’s auditors to complete their audit work, among other things.”

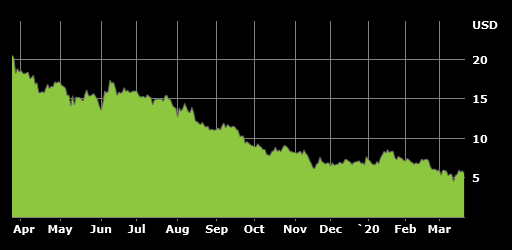

Cronos Stock Performance

The above chart shows that CRON was on a steady downward trend during 2019. This trend has continued in 2020, as the stock has declined more than 25% YTD. In the past month, the stock has eclipsed the 10M daily volume mark (about 15% higher than the 90 day average) 3 times. This metric is of value to me as I believe increased volume is an important component in determining future stock performance. And “the trend is your friend“ in this regard, especially on a short-term basis. In addition, as information about the SEC inquiry grows within the investment community, an increase in both volatility and volume will likely put additional selling pressure on CRON's stock. The degree of uncertainty about the company’s financial health will contribute to a loss of support going forward, which may prompt some institutional holders to trim their positions in Cronos Group. The bottom line is that CRON is on a “slippery slope” given the SEC inquiry and the company’s 3/17/20 disclosure that previously issued unaudited interim financial statements for the first, second and third quarters of 2019 "will be restated and reissued and should no longer be relied upon"

The Macro Bear Case

In my article on 10/27/19, I expressed my view that the challenges facing the cannabis industry were likely to increase at a faster pace in 2020 as the marked increase in supply impacted prices and a lower equilibrium price was determined by the marketplace. This “new normal” price would result in at least 75% of the 44 companies in the Global Cannabis Stock Index to be unable to continue operations within one or two years. As we approach the end of 2020 Q1, it appears to me that it is increasingly likely that there will be a pronounced acceleration of business failures for the remainder of 2020 due to the coronavirus pandemic and resulting downturn in economic activity.

In my article on 1/8/20, I stated that my modeling work indicated that Cronos Group Inc. was vulnerable to a short-selling attack. Since then, CRON has decreased from $6.64 to $5.55 or ~ 16%. I also said that there would be a domino effect price-wise on many of the largest marijuana/cannabis ETFs. I note that the 3 ETFs (MJ, CNBS and THCX) upon which my modeling is based, are each down significantly as this table indicates:

ETF Symbol | 2020 YTD |

MJ | -43% |

CNBS | -46% |

THCX | -49% |

CRON is the #1 “pure play” holding in each of these ETFs, and if they individually or collectively decide to trim their shares, there would be more downside risk to CRON's stock.

2020 Cronos News Releases

The company has issued several news releases in 2020 of interest, as summarized below:

24 Feb 2020

Cronos Group to Delay 2019 Fourth Quarter and Full-Year Earnings Release and Conference Call

TORONTO, Feb. 24, 2020 (GLOBE NEWSWIRE) -- Cronos Group Inc. [NASDAQ: CRON] [TSX: CRON] (“Cronos Group” or the “Company”) today announced that it will delay its 2019 fourth quarter and full-year earnings release and conference call, previously scheduled for Thursday, February 27, 2020. The Company has had a delay in the completion of its financial statements and will make a further announcement in a subsequent press release to schedule the date and time of the earnings conference call.

02 Mar 2020

Cronos Group Files Form 12b-25

TORONTO , March 02, 2020 (GLOBE NEWSWIRE) -- Cronos Group Inc. [NASDAQ: CRON] [TSX: CRON] (“Cronos Group” or the “Company”) today announced that it has filed a Form 12b-25 with the U.S. Securities and Exchange Commission providing the Company a 15-day extension of the due date for filing its Annual Report on Form 10-K for the year ended December 31, 2019 (the “Form 10-K”).

17 Mar 2020

Cronos Group to Restate Certain 2019 Unaudited Interim Financial Statements

TORONTO , March 17, 2020 (GLOBE NEWSWIRE) -- Cronos Group Inc. [NASDAQ: CRON] [TSX: CRON] (“Cronos Group” or the “Company”) announced today that the Company determined, on the recommendation of the Audit Committee of the Company’s Board of Directors and after consultation with KPMG LLP , the Company’s independent registered public accounting firm, that Cronos Group’s previously issued unaudited interim financial statements for first, second and third quarters of 2019 prepared in accordance with International Financial Reporting Standards as filed on SEDAR, and with the U.S. Securities and Exchange Commission on Form 6-K, will be restated and reissued and should no longer be relied upon. In addition, the company has submitted a number of 8-K and other filings to the SEC about the departure of a director, officers, and other pertinent financial matters which are available on the company’s website. I urge anyone who would like more detailed information to review these documents on the company’s website, which is thecronosgroup.com.

2020 Analysts’ Price Targets

According to a recent article, analysts’ average price target is $8.28, which translates to a 12-month return potential of ~50% based on CRON's closing price of $5.55 on 3/20/20. However, since the company has stated that their 2019 financial statements ”should no longer be relied upon,” it appears appropriate that this forecast may be revised downward

Random Thoughts Regarding the SEC Inquiry

Given the recency of the disclosure regarding this matter, it would be both premature and presumptuous to speculate to any degree of specificity about what may transpire going forward. That said, the CPA in me took serious note that “the company anticipates that it will report one or more material weakness in internal control over financial reporting when it files its Form 10-K.” This leads me to speculate that the SEC inquiry may involve an ASC 606 issue. Simply put, ASC 606 mandates an increased number of new disclosures, intended to provide greater transparency to investors about a company’s revenue contracts and related accounting policies and practices.

Conclusion

My due diligence in the preparation of this article included reviewing CRON news releases and SEC filings, Seeking Alpha articles and a recent company research report made available to select Fidelity Investments brokerage clients. This scrutiny leads me to conclude that there will be lingering financial and operational questions regarding the future direction of the company until there is much more clarity regarding the financials. Based on my “survival of the financially fittest” focus, Cronos Group, Inc. clearly does not meet this criterion, either on a macro or micro level as detailed herein. The SEC inquiry adds even more questions about the financial health and viability of CRON, and the time frame for its resolution is unknown. As a result, my view is that for the foreseeable future CRON's stock is simply not worthy of investment consideration for the foreseeable future due to the tsunami of uncertainty swirling around CRON like a pot of my aunt’s award-winning St Patrick’s Day cheddar whiskey fondue.