Introduction

Charlotte's Web (OTCQX:CWBHF) reported disappointed 2020 Q1 results that showed persistent headwinds facing the company. As the CBD market becomes crowded and saturated, CWEB is struggling to return to its growth path. We are turning cautious on the stock and will remain neutral until there is a clear sign of growth rekindling in the company.

2020 Q1 Review

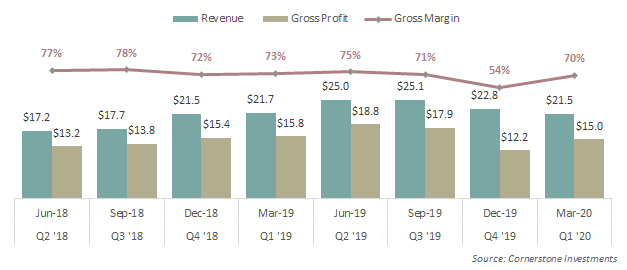

Charlotte's Web reported 2020 Q1 results that depicted a picture of itself struggling to rekindle growth amid a chaotic market. The company saw its revenue decline 6% sequentially to $21.5 million which was the revenue it reported in Q4 2018, indicating a significant setback in its growth strategy despite the legalization of hemp cultivation in the U.S. and the entry of F/D/M retailers into the market. While CWEB has remained disciplinary in its pricing and gross margins remained strong at 70%, the company is losing market share to other competing products that have flooded the CBD market.

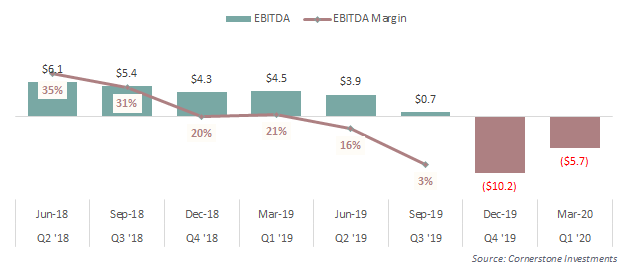

Although CWEB has managed to maintain strong gross margins, the company is incurring heavy losses due to an increase in general and operating expenses and investment in new capacities. In Q1 2019, the company reported SG&A of $8.5 million and sales and marketing of $4.6 million; in Q1 2020, SG&A has almost doubled to $16 million while sales and marketing grew substantially to $6.5 million. Under the new CEO of Deanie Elsner, it is expected that the company is making investments to add new talent to the management team and expand its capabilities to serve increasingly more sophisticated and demanding customers, but revenue has all but stalled which is a recipe for disaster on the bottom line. The key to fix the worsening profitability is not to stop investments for the future but rather find ways to drive accretive growth while spending appropriately to avoid stretching the balance sheet.

CWEB has been making investments to prepare for its next phase of growth. As we discussed in "Investing Now For The Future", the company is building a 137,000 sq ft production facility which will support up to $2 billion of annual revenue. The firm has also hired a number of executives from other industries to round out its management team. The significant increase in SG&A and sales and marketing costs are a direct result of these investments. However, despite the early signs of promise, the CBD market is looking very crowded and CWEB has seen declining sales in two quarters in a row now. We suspect that management will begin to cut costs and reduce investments in order to improve liquidity. The company reported $53 million of cash on hand at the end of Q1 which decreased $15.5 million from Q4 2019 due to $14.8 million of negative operating cash flow and $1.5 million of capital expenditures, offset by a small amount of option exercise proceeds. If the cash burn continues for a few more quarters, we could see the need for additional capital raise which will most likely exert downward pressure on the share price.

Valuations

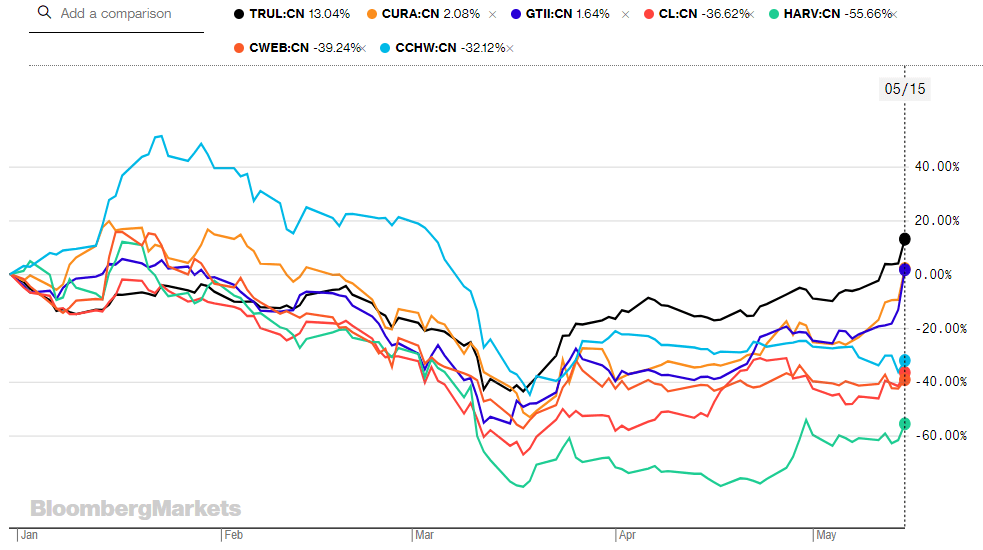

CWEB has underperformed its peers in 2020 so far as recent poor financial performance resulted in deepening investor concerns. The stock has dropped 39% this year which is the second-worst performer in this group only behind Harvest Health (OTCQX:HRVSF). CWEB currently has a market cap of $500 million and trades at an EV/Sales (Q1 Annualized) of 5.2x which is in-line with most peers. The stock used to boast some of the highest trading multiples in the sector but that premium has eroded as its early-advantaged was replaced with recent struggles. CWEB was one of the early growth stories in the cannabis sector with its strong brand awareness among consumers and recognition for its product quality. However, as other operators expanded, the hemp producer is facing increasing competition due to the low barrier of entry in its industry. After the legalization of hemp cultivation, coupled with the abundance of cheap hemp raw materials, the consumer market is littered with all kinds of CBD products. Consumers are facing a wide array of product choices in addition to cheaper products with similar ingredients. Despite strong consumer awareness, CWEB is facing too much competition to continue growing in today's CBD market which will persist for the foreseeable future.

Looking Ahead

Charlotte's Web was once one of the premium names in the U.S. cannabis sector due to its established brand, high-quality products, and superior financial performance. However, after the 2018 Farm Bill eliminated the barrier to entry for CBD products, the market has become saturated and increasingly competitive. As a result, CWEB has struggled with declining sales as revenue has stayed flat since Q4 2018. Moreover, management embarked on an ambitious investment phase including a new facility and talent acquisitions. Margins took a massive hit as a result of these investments and cash flows are negative, threatening its medium-term financial stability. Due to all these reasons and deteriorating financial metrics, we are turning more cautious on the stock in the near-term.