This article focuses attention on 20 publicly traded, pure cannabis companies that on September 21, 2020, had the market capitalizations of at least $100 million. Gross profit, operating income and operating expenses expressed as percentages of total revenue before adjustment for biologicals are presented to shed light on company profitability and operating efficiency. Financial leverage and intangible plus goodwill assets are also presented to indicate company reliance on borrowings versus equity. These measures are presented to help identify the earnings capacity of these cannabis companies.

After looking at the aforementioned metrics, the share price of each company is then measured based on cash flow, net income after tax, book value, operating income, EBITDA, and total revenue. These measurements are designed to help identify which cannabis companies offer better shareholder value.

Cannabis Companies

Two companies with market capitalizations above $100 million that are often included in a list of cannabis companies are excluded from this study. Innovative Industrial Properties (IIPR) was excluded because it is a REIT, while Scotts Miracle-Gro (SMG) was excluded because it is not a pure cannabis play. On the other hand, GW Pharmaceuticals (GWPH) was included because it is a pure cannabis drug company and is the oldest publicly traded cannabis stock; and GrowGeneration (GRWG) is a supplier of products to cannabis growers.

Company Characteristics

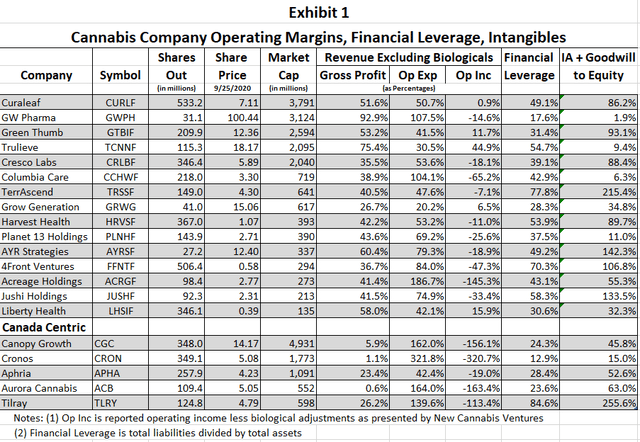

Exhibit 1 lists cannabis companies in descending order based on market capitalization as of the close on Friday, September 25. Five of the companies have been categorized as Canada centric, because they are officially Licensed Producers or LPs in Canada.

The metrics presented in Exhibit 1 were generally derived from data obtained from the most recent financial reports that companies filed with Sedar or the SEC. If a company reported its financials in Canadian dollars those were converted to U.S. dollars at an exchange rate of C$1.30 equals $1.00, which was the exchange rate prevailing on the day data were assembled.

Exhibit 1 shows the gross profit margin, which equals total revenue before biological adjustments but after excise taxes and cost of goods sold, expressed as a percentage of total revenue. Gross profit is obviously needed to cover all other company expenses for a company to make money.

Gross Profit Margins

The data show that gross profit margins among non Canadian companies ranged from a low of 26.7% for GrowGeneration to a high of 92.9% at GW Pharmaceuticals. Neither of these companies is your typical cannabis company; therefore, a comparison among the others is more meaningful and shows a low gross profit margin of 35.5% at Cresco Labs (OTCQX:CRLBF) and a high of 75.4% at Trulieve (OTCQX:TCNNF). Cresco and Trulieve are both full-fledged, multi-state-operators, MSOs, but Trulieve is just beginning to plant its flags on the map.

Trulieve has by far the highest gross profit margin among MSOs or Single State Operators, SSOs. AYR Strategies (OTCQX:AYRSF), a company formed through a special purpose acquisition corporation or SPAC, ranked a distant second at 60.4% followed closely by Liberty Health Sciences (OTCQX:LHSIF) at 58.0% then by Green Thumb Industries (OTCQX:GTBIF) at 53.2% and Curaleaf (OTCPK:CURLF) at 51.6%. No other cannabis company has a gross profit margin above 50%. Interestingly, the two cannabis companies with the largest gross profit margins are located in and derive most of their revenue from Florida's vibrant medical marijuana market.

Trulieve's outsized gross profit margin is attributable to economies of scale from it having 1.8 million square feet of cultivation in Florida. Its gross profit margin will likely come under significant downward pressure as its announced modest cultivation facilities become operational in Massachusetts, West Virginia and Pennsylvania.

Canadian Company Gross Profit Margins

The Canadian centric companies all have embarrassingly low gross profit margins ranging from an infinitesimal 1.1% at Cronos (CRON) to a meager 26.2% at Tilray (TLRY). I believe this is due to management and the investment banking community focusing the investing public's attention on gross profit after biological adjustments per the International Financial Reporting Standards (IFRS) as the primary yardstick for measuring company performance. This misdirection encouraged companies to grow as much cannabis as they could, since IFRS allowed them to include cannabis in revenue as it grew, even before it was sold! This revenue charade was facilitated by cannabis company accountants and regulators; and, it led directly to a C$1.6 billion write-down announced by Aurora Cannabis (ACB) on September 22, 2020.

In 2017 and 2018, investors in the large Canadian cannabis company stocks were told there would be a huge shortage of cannabis when Canada legalized recreational use in November 2018. That forecast turned out to be absolutely wrong; and, investors in the five Canadian LPs lost $77 billion in these five stocks since they peaked in late 2018 and early 2019.

There are people still hanging on to those broken stocks thinking that Tilray will get back to $300 and Aurora will trade at $150. The fact is those stocks have no chance of returning to their halcyon days. Part of the reason for the incorrect forecast was that the provinces, especially Ontario, were slow to allow the opening of dispensaries. Also, companies overexpanded and grew too much cannabis for the Canadian market.

Operating Efficiency

Exhibit 1 also shows operating efficiency by expressing operating expenses as a percentage of total revenue. If GrowGeneration and GW Pharma are excluded, then Trulieve is the most efficient operator since its ratio of operating expenses to total revenue is the lowest at 30.5%. A distant second in operating efficiency is Green Thumb with 41.5% followed by Liberty Health at 42.1% and TerrAscend (OTCQX:TRSSF) at 47.6%. All the others have operating expenses ratios of 50.7% or higher. The least efficient cannabis company is Acreage Holdings (OTCQX:ACRGF), which has operating expenses that represent an astonishing 186.9% of its total revenue.

Trulieve's operating efficiency ratio will likely decline as its operations outside Florida come online. Liberty Health's management expects its operating efficiency to improve beginning in the fourth quarter as new strains of cannabis are harvested and sold; however, they have a bad forecasting track record.

Canadian Operating Efficiency

Exhibit 1 shows that only one large Canada centric cannabis company, Aphria (APHA), has a double-digit operating efficiency ratio at 42.4%. The other four have disastrous ratios ranging from Tilray's 139.6% of revenue to Cronos' 321.8% of revenue. Incredibly, Cronos had operating expenses that were more than three times its total revenue before biological adjustment.

Operating Profitability

If the operating expense to total revenue percentage is deducted from the gross profit to total revenue percentage, the result is operating income before taxes as a percentage of total revenue. If the gross profit percentage exceeds the operating expense percentage, the result is operating income as a percentage of total revenue. If the gross profit percentage is less than the operating expense percentage, the result is an operating loss as a percentage of total revenue.

Exhibit 1 shows that only five (5) of the twenty (20) largest cannabis companies have gross profits large enough to cover their operating expenses and they were all non-Canada centric companies. Trulieve has the highest operating income before taxes as a percentage of total revenue at 44.9% thanks to the fact it has the highest profit margin and most efficient operation. Following Trulieve are Liberty Health at 15.9%, Green Thumb at 11.7%, GrowGeneration at 6.5% and Curaleaf at 0.9%.

Of the ten (10) non Canadian centric companies showing operating losses the one with the largest loss as a percentage of total revenue is Acreage Holdings which has an operating loss of 145.3% of revenue. Columbia Care (OTCQX:CCHWF) has the second largest operating loss at 65.2% of revenue followed by 4Front Ventures (OTCQX:FFNTF) at 47.3% and Jushi Holdings (OTCQB:JUSHF) at 33.4%.

Canadian Company Operating Losses

All five Canada centric companies show operating losses. Aphria fared the best with an operating loss equal to 19.0% of its total revenue before biological adjustment. Cronos is the worst of the five showing a loss of 320.7%.

These five Canadian companies are a stain on the cannabis sector. The fact that they still get featured coverage, especially on CNBC's Fast Money program, weighs heavily on the sector and gives it a bad name.

Financial Leverage

Financial leverage is the extent to which a company uses debt to finance its assets. In Exhibit 1 a company without any debt obligations would have a financial leverage ratio of 0%, while a company without any shareholders' equity would have a financial leverage ratio of 100%. A fundamental rule of financial leverage is that it magnifies gains as well as losses; therefore, it has to be used judiciously.

Of the 15 non-Canada centric cannabis companies, the two using the lowest financial leverage are GW Pharma at 17.6% and GrowGeneration at 28.3%. Among the other 13, the one with the lowest degree of financial leverage is Liberty Health, which has a liabilities to asset ratio of 30.6%. The company with the second lowest is Green Thumb with 31.4% followed by Planet 13 (OTCQX:PLNHF) at 37.5% followed by Cresco Labs at 39.1%.

Canadian Company Financial Leverage

Four of the Canada centric companies have low degrees of financial leverage compared to non-Canada centric companies. Cronos with a 12.9% ratio has the lowest degree of financial leverage followed by Aurora at 23.6% Canopy Growth (CGC) at 24.3% and Aphria at 28.4%. Interestingly, Tilray's liabilities to total asset ratio of 84.6% evidences the highest degree of financial leverage used by any of the 20 companies and is attributable to its rapid vaporization of shareholders' equity.

Intangible Assets

Growth of intangible assets and goodwill is often a warning sign of possible problems. Both are recorded on a corporate balance sheet when a company is formed or it acquires another company. Intangible assets are written off (amortized) over a period of years, while goodwill remains on the balance sheet in perpetuity unless company accountants decide the recorded amount of goodwill can no longer be justified, which is what happened at Aurora Cannabis. The accounting treatment afforded intangible assets and goodwill actually encourages cannabis companies to acquire other companies at prices that cannot be justified. These assets are often deducted from shareholders' equity to arrive at tangible book value.

The last column in Exhibit 1 shows intangible assets plus goodwill expressed as a percentage of shareholders' equity for each cannabis company. If GW Pharma and GrowGeneration are once again ignored, Columbia Care has the lowest percentage of capital tied up in intangible assets and goodwill at 6.3%. Trulieve is a close second at 9.4% followed by Planet 13 at 11.0% Liberty Health at 32.3% and GrowGeneration at 34.8%. All other non-Canada centric companies have percentages of 55.3% or more. The companies with the largest percentages of shareholders' equity in intangible assets and goodwill are the acquisitive TerrAscend at 215.4%, followed by AYR Strategies at 142.3%, Jushi Holdings at 133.5% and 4Front Ventures at 106.8%.

Intangible Assets at Canadian Companies

Among Canada centric companies, Cronos has the lowest percentage of equity in intangibles and goodwill at 15.0%. Tilray's ratio of 255.6% is the highest for any cannabis company in Exhibit 1. Aurora's ratio of 63.0% is down significantly from its prior-year ratio of 87.9%, because of its writeoffs.

The facts are that the Canada centric companies were able to capture an abundance of investor dollars early because they were the only publicly traded cannabis companies and they were heavily promoted by Canadian investment bankers who made fortunes selling such stocks. The company's investor relations departments were always issuing press releases to keep investor interest. As a recipient of these releases I was surprised I wasn't advised about what the CEO had for lunch!

All the cannabis hoopla in Canada certainly captured the attention of the once gifted Sands Brothers who decided to have Constellation Brands (STZ) invest $4 billion in Canopy Growth and Altria (MO) which invested $2.4 billion in Cronos. Canopy and Cronos would both be in the corporate graveyard if they had not raised those billions, since both would be showing significantly negative shareholders' equity.

Valuing Cannabis Company Stocks

It is generally accepted that the intrinsic value of a company equals the discounted value of free cash flow generated in the current and future years. It follows that the intrinsic value of a share of stock in a company will equal the total discounted cash flow generated by a company divided by the number of shares it has outstanding.

Once intrinsic values are calculated for companies in a sector then those companies can be compared with one another by expressing intrinsic values relative to share prices. Furthermore, aggregating company intrinsic values relative to share prices within a sector enables an analyst to determine relative valuations among sectors.

The Problem Valuing Cannabis Companies

A serious valuation problem occurs, however, when companies do not produce positive operating cash flow. In such instances, security analysts will use a host of other metrics to assess valuation and justify share prices. They will compare share price to earnings, sales revenue, book value, tangible book value, financial leverage, and EBITA for companies and sectors to determine relative values within and among sectors. By so doing, they seek to identify which company's stock is cheap or expensive compared to others within a sector and which sectors are cheap or expensive relative to other sectors.

The problem of identifying value is compounded when there is not much historical financial information. This is exactly the problem that faces investors in the cannabis sector, since it is only a few years old.

Valuation Metrics

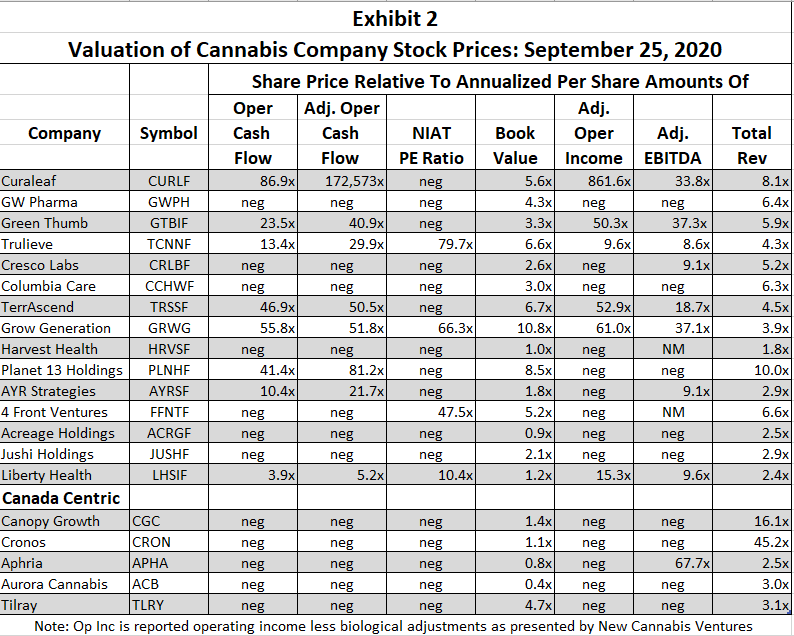

Exhibit 2 shows the stock price of each of the 20 cannabis companies as a multiple of the per share amounts of operating cash flow, adjusted operating cash flow, net income after taxes, book value, adjusted operating income, adjusted EBITDA, and total revenue. Data presented are based on the most recent quarterly filings and the closing stock prices on September 25, 2020.

Cash Flow Provided From Operations

Column 3 shows that only eight (8) of the 20 cannabis companies have positive free cash flow from operations and they are all non-Canada centric companies. In terms of operating cash flow, Liberty offers the best value, since its stock sells at 3.9x (times) operating cash flow. AYR Strategies is second at 10.4x followed by Trulieve at 13.4x Green Thumb at 23.5x Planet 13 at 41.4x TerrAscend at 46.9x GrowGeneration at 55.8x and Curaleaf at 86.9x.

Adjusted Cash Flow Provided From Operations

Column 4 adjusts operating cash flow to account for non payment of current taxes, since non payment has become common practice among non-Canada centric cannabis companies as a way to borrow money, conserve cash, and perhaps embellish their cash flow statements. Liberty continued to offer the best value even after adjusting for taxes, since its stock traded at only 5.2x adjusted operating cash flow. AYR Strategies remained second at 21.7% and Trulieve remained third at 29.9% even though their ratios more than doubled.

A comparison of columns 3 and 4 in Exhibit 2 shows that non payment of taxes had a material impact. In particular, Curaleaf experienced the greatest change as its stock price to adjusted cash flow ratio exploded to 172,573x from 86.9x. The reason is that in the six months ended June 30, 2020 Curaleaf reported net cash provided by operating activities of $21,814,000 million; however, it did not pay $21,803,000 in taxes it incurred thus its adjusted operating cash flow was only $11,000. In contrast to Curaleaf, GrowGeneration actually paid more in taxes than it incurred during its most recent reporting period; therefore, its stock price to adjusted operating cash flow ratio was lower at 51.8%.

Net Income After Taxes

Column 5 in Exhibit 2 shows that only four (4) of the 20 cannabis companies reported any net income after taxes (NIAT) for their most recent quarter. Liberty Health is the only one with earnings per share sizeable enough to report a respectable PE ratio of 10.4x. 4Front Ventures offers the second best PE value at 47.5x followed by GrowGeneration at 66.3x and Trulieve at 79.7x.

A large PE ratio is not necessarily alarming. In fact, companies with rapid growth rates will most often have high PE ratios. A PEG ratio is used to factor in growth and is calculated by dividing the PE ratio by the growth rate in earnings. A PEG ratio could not be calculated for Trulieve since its most recent quarterly sequential earnings growth rate is a negative 53%. Peg ratios could also not be calculated for 4Front Ventures and Liberty Health because their prior quarters produced net losses.

On the other hand, the PEG ratio for GrowGeneration is 0.15, since its growth rate in earnings of 436% far exceeds its PE ratio of 66.3%. Anything below 1.0 is considered good; therefore, it can be said that GrowGeneration stock is cheap on the basis of its PEG ratio. Unfortunately, that growth rate of earnings was only for the most recently reported quarter.

The fact that 16 of the top 20 cannabis companies lost money after taxes in their latest quarters is not a good sign. It is especially bad that only Liberty Health shows a respectable PE ratio, while GrowGeneration has a great PEG ratio.

Book Value

It is intuitively obvious that time-tested cash flow and net income measurements are unable to be used to rank these 20 cannabis companies, since only three (3) of the 20 have positive operating cash flow and income after taxes. With that in mind, column 6 in Exhibit 2 shows the ratio of stock price to book value for each company. Book value was obtained by dividing shareholders' equity by the number of shares companies reported on their filed income statements. Column 6 shows that among the 15 non-Canada centric companies stock prices range from Acreage's 0.9x book value to GrowGeneration's 10.8x.

If stocks selling near book value offer the best value then Acreage and Harvest Health (OTCQX:HRVSF) at 1.0x would be best buys. Interestingly, however, these two cannabis companies have horrible cash flows and are losing large amounts of money. Based on their most recent quarters, Acreage's annualized cash flow is a negative $78.6 million and its after tax loss is $148.8 million; and, Harvest's annualized cash flow is a negative $36.3 million and its after tax loss is $75.3 million. As earlier shown in Exhibit 1, Acreage showed operating expenses that were 186.7% of its total revenue. Buying these two companies based solely on book value would be foolhardy.

Before totally dismissing the use of book value at a metric for measuring the relative attractiveness of one cannabis stock over another, it is worth noting that Liberty Health stock is trading at 1.2x book value and earlier in this article it was ranked highly using a number of different measures. At the same time, Trulieve scored highly using earlier metrics and its stock is trading at 6.6x book value.

Canadian Companies' Book Values

The five Canada centric company stocks trade between Aurora's 0.4x and Tilray's 4.7x book value. The low price of Aurora's stock relative to its book value is the result of its recently announced massive C$1.6 billion write-down and the collapse in its stock price.

Tilray's 4.7x may reach infinity within the next six months, since at its current rate of loss it should soon run out of shareholders' equity. In the quarter ended June 30, it reported a loss of $81.7 million leaving it with equity of $131.5 million. It also showed it had $179.8 million in intangible assets and $156.4 million in goodwill which auditors may seriously question in view of Tilray's recurring losses. The outlook for Tilray certainly looks grim.

Diving deep into Canada centric cannabis company financial statements shows that using a stock's book value as a basis for investment is dangerous. The same principle applies to non-Canada centric cannabis companies.

Adjusted Operating Income

Alan Brochstein, a Seeking Alpha contributor and publisher of the New Cannabis Ventures newsletter, calculates adjusted operating income for most publicly traded cannabis companies. He defines this income as "reported operating income less any accounting adjustments for the change in fair value of biological assets companies might report under IFRS accounting rules."

Brochstein's adjusted operating income figure was annualized and divided by the number of shares outstanding to get adjusted operating income per share. The latter was then divided into a company's stock price to obtain a multiple.

Column 7 in Exhibit 2 shows the stock prices of all 20 cannabis companies expressed as multiples of company adjusted operating income. Values are shown for only six of the 20 companies, because all the others have adjusted operating losses. None of the six were Canada centric companies.

When viewed through this prism, Trulieve stock is the best buy because it sells at 9.6x adjusted operating income. Liberty Health is a relatively close second at 15.3x compared to Green Thumb at 50.3x TerrAscend at 52.9x GrowGeneration at 61.0x and Curaleaf at a distant 861.6x.

Adjusted EBITDA

Given the cannabis sector's inability to produce free cash flow from operations along with after tax profits, it is not surprising that cannabis companies and their investment bankers have dreamt up another performance metric. As profits and free cash flow failed to materialize, cannabis companies and investment bankers with increasing frequency started touting adjusted EBITDA as the metric investors needed to look at.

Charlie Munger, Warren Buffett's longtime partner, is a major critic of this metric. Munger has said "I don't like when investment bankers talk about EBITDA, which I call bullshit earnings. Think of the basic intellectual dishonesty that comes when you start talking about adjusted EBITDA. You're almost announcing you're a flake."

Column 8 of Exhibit 2 shows stock price as a multiple of adjusted EBITDA. Companies generally feature their adjusted EBITDA during quarterly earnings reports, since most other metrics are simply too embarrassing to mention. Exhibit 2 shows that among the 15 non-Canada centric companies only eight (8) were able to report positive adjusted EBITDA for their most recent quarters. Trulieve, an adjusted EBITDA fanatic, has a stock price trading at 8.6x, which is the lowest multiple. Cresco Labs and AYR Strategies tie for second lowest at 9.1x followed closely by Liberty Health at 9.6x.

Canadian Companies Adjusted EBITDA

Aphria is the only major Canada centric company able to produce positive adjusted EBITDA and its stock trades at 67.7x that amount. The others, especially Canopy Growth, are famous for telling everyone that they will turn EBITDA-positive in the near future. It just never happens!

Total Revenue

When management and investment bankers are unable to burnish a company's actual results they invariably focus attention on total revenue. The last column in Exhibit 2 shows the resulting multiple when a company's stock price is divided by its revenue per share.

Exhibit 2 shows that Harvest Health has the lowest multiple, since its stock is trading at 1.8x revenue per share. Liberty Health is a close second at 2.4x followed by Acreage at 2.5x then AYR Strategies and Jushi at 2.9x each. Planet 13 has the highest multiple at 10.0x followed by Curaleaf at 8.1x.

Canadian Companies Total Revenue

Canada centric companies exhibit quite a dispersion when their stock prices are shown as multiples of revenue. Aphria's stock has the lowest ratio trading at 2.5x sales followed closely by Aurora at 3.0x and Tilray at 3.1x.

Interestingly, Cronos and Canopy Growth have ratios that are well above all other cannabis companies with Cronos stock selling at 45.2x revenue and Canopy Growth selling at 16.1%. The outsized valuations for these companies are undoubtedly related to the fact that control of these companies is in the hands of two giant companies with high pain thresholds thanks to market capitalizations of $71 billion for Altria and $33 billion for Constellation Brands.

The stock prices of Cronos and Canopy Growth are down by more than 70% from their peak prices reached in early 2019 and shareholders in those two companies have lost about $16.9 billion in market value. The losses in these two stocks almost equal the total market value of the 15 largest non-Canada centric companies. It is not surprising that investors have a jaded view of the cannabis sector.

Conclusion

This article has shined a spotlight on the 20 largest publicly traded cannabis companies and showed most are not worthwhile investments. Data presented show a wide variation in performance among companies in the sector. Sadly, only five companies have large enough profit margins before biological adjustments to cover their operating expenses and earn an operating income. At the same time, seven companies have operating expenses that exceed their total revenue. Given these poor results, it should come as no surprise that investor enthusiasm for the cannabis sector has waned.

To identify which cannabis company stock offers the best relative value, companies were ranked from 1 to 10 in each of the 11 metrics. One (1) point was assigned to the company with the best metric, two (2) points to the company with the second best, three (3) points to the company with the third best, et cetera. Each measure was given equal weight and the points totaled. Accordingly, the stock of the company with the lowest score offers the best value relative to the other 20 cannabis companies.

Liberty Health Sciences has the lowest score with 19 points; therefore, it offers the best value. It achieved its score by ranking second in gross profit margin, second in operating income margin and third in operating efficiency. Liberty also had the least financial leverage as illustrated by the fact that it has the lowest ratio of liabilities to shareholders' equity. Furthermore, the percentage of its shareholders' equity supporting intangible assets and goodwill is the fourth lowest among the non-Canada centric companies.

Liberty's stock price trades at only 3.9x operating cash flow, 5.2x adjusted operating cash flow, and 10.4x after tax income thereby ranking its stock as the least expensive when these measurements are utilized. Liberty's stock price also trades at the second-lowest multiple of book value, the second-lowest multiple of adjusted operating income, the fourth-lowest multiple of adjusted EBITDA, and the second-lowest multiple of actual revenue.

Liberty is a SSO with 100% of its operations in Florida. Its headquarters and cultivation/processing facilities are located on 247 acres of usable land it owns in Gainesville, Florida. Liberty currently has 190,000 square feet of cultivation with a production capacity of 19,500 kg per year. It has announced plans to add an additional300,000 square feet by the end of calendar year 2021, which will bring its cultivation space to 490,000 square feet. It has 26 operating dispensaries and has plans to add another ten (10) before the end of 2020. A recent partnership with Seed Junky Genetics will produce its first harvest in late October 2020 with products expected to be on dispensary shelves by early November. Samples show a 4x multiple on dry yields as a result of this partnership.

The cannabis company whose stock ranked as the second best value among the 20 cannabis companies was Trulieve which tallied 37 points. Unfortunately, similar tabulations cannot be made for any of the other 20 cannabis companies, since all scored negative numbers for one or more metrics.

Trulieve has long dominated the Florida medical marijuana market where it has 59 dispensaries and accounts for about 50 percent of all sales. The large number of dispensaries along with its 1.8 million square feet of cultivation in Northwest Florida has allowed it to achieve economies of scale not possible in other states that limit the number of dispensaries and cultivation square footage. These economies of scale have enabled it to produce outsized margins compared to other cannabis companies.

The fact that the two companies with the best stock value both emanate from Florida is understandable. Florida has a permanent population of 22 million growing at a 3% rate and it has 20 million seasonal residents/snowbirds. All of these people can obtain medical marijuana cards if one of the 2,624 qualified physicians determines they suffer from almost any physical or mental condition. Florida now has 420,743 qualified patients with medical marijuana IDs and that number is growing by about 5,000 each week. A year ago Florida had 266,849 people with medical marijuana IDs, so the number of patients has increased by 57.6% in the past year.

Catalysts indicate the outlook for cannabis companies in Florida is very bright. Edibles were just allowed and are expected to immediately account for about $200 million in annual sales without robbing sales from flower, concentrates, tinctures, et cetera. There is also a growing belief that recreational consumption will be approved in 2022; and, with 130 million people visiting Florida every year, expectations are that sales would surge.

Liberty Health seems content to remain a SSO and focus 100% of its energy and financial resources on Florida. Trulieve, on the other hand, has set its sights on establishing itself as a full fledged MSO with a nationwide presence.

Investing in Liberty Health or Trulieve is not riskless. Both are thinly traded on the Canadian Stock Exchange, CSE, and the OTC, which are both notoriously dangerous markets requiring use of limit orders for self preservation. Also, despite its performance Liberty Health casts a dark shadow, because it trades at $0.38 and is officially labeled a "penny stock." Penny stocks have a long history of wiping out investors and a majority of investors will not consider investing in such stocks.

Investors have expressed concern about Liberty Health management's inability to produce consistent results. Management has said changes they are implementing will begin producing a significant increase in sales before the end of this calendar year. If management fails to achieve their forecasted sales growth, shareholders will be very disappointed.

Similarly, there are no guarantees that Trulieve will be able to translate its success in Florida to other states. In fact, shareholders dumped Trulieve stock immediately after it made two concurrent announcements on September 16, 2020. On that date Trulieve announced the sale of 4.715 million shares of stock at a price of $18.85, which was 7.9% below the $20.46 closing price of its stock at the time of the announcement thereby diluting shareholders. It also announced the acquisition of a 35,000 square foot cultivation/processing facility and three dispensaries in Western Pennsylvania at a price of as much as $141 million. The market reacted negatively to these announcements and within days the stock price fell to a low of $16.70 down 18.4% from the price immediately prior to the announcement.

Big changes in Trulieve's balance sheet, income statement, and cash flow statement will appear starting in Q4 2020. Its gross profit margin, operating efficiency, operating margin, and net income will all likely come under pressure in future quarters as it embraces the MSO model. Trulieve may also no longer generate positive cash flow from operations and could be forced to tap the capital markets.

Cannabis companies are clearly struggling to earn respectable income. Given mounting losses and large amounts of intangible and goodwill assets at many cannabis companies, significant write-offs like Aurora's can be expected on or before other cannabis companies publish their audited annual reports.

As a final note, conservative investors are encouraged to ignore cannabis companies that do not consistently produce after taxes earnings and tax adjusted positive free cash flow from operations. Until cannabis companies produce such positive results, it's caveat emptor for investors in cannabis company stocks.