When I first began following the cannabis industry in early 2013, every single stock traded exclusively over-the-counter ("OTC"). Many of them didn't even file with the SEC! Fortunately, the market has evolved, and today most cannabis stocks trade on junior and senior exchanges in Canada as well as major exchanges in the U.S.

Those wishing to invest in companies that grow, process or sell cannabis but that are unwilling to invest in Canada or on the OTC face a very narrow universe, as major exchanges currently don't permit direct federally illegal cannabis companies to list. What this means is that those who want to buy a cannabis producer on the NYSE or NASDAQ are limited to Canadian licensed producers. This includes companies like Aphria (OTC:APHA), Aurora Cannabis (OTC:ACB), Canopy Growth (OTC:CGC), Cronos Group (OTC:CRON) and Tilray (TLRY), which each has a market cap in excess of US$1 billion. In total, the NYSE and NASDAQ have 10 companies listed that are direct cannabis producers.

While many may not be aware, there are a few companies that are leveraged to the American state-legal cannabis sector, providing ancillary goods or services, that trade on higher exchanges. These stocks have performed well in 2020, but I believe that they could continue to outpace the broad market as more investors become aware of them.

6 Ancillary Companies Trade on Major Exchanges

Akerna (KERN) is a relatively new company following MJ Freeway merging into a SPAC a year ago. The company, which was just added to the Russell 2000 index, has closed two acquisitions, and shareholders have just approved a third. For a company that has been around for a very long time providing essential software to the industry, it has generated disappointingly low revenue to date. The acquisitions add additional opportunity on several fronts, and I am hopeful that the company can continue to use its public currency to build a larger entity. MJ Freeway has had challenges in its Leaf Data business, where it serves Washington, Pennsylvania and Utah.

I follow Akerna, including it on my Focus List at 420 Investor. I also find the warrants (KERNW) to be quite interesting. The valuation is expensive in my view, and I would like to see stronger revenue growth. Before including the shares to be issued for the pending Ample Organics acquisition, the stock has a market cap of $112 million (based on fully-diluted in-the-money shares), which is more than 11X annualized revenue from fiscal Q3. The company got a reasonable price on the Ample Organics acquisition, and, while it will boost the market cap, it will also help on the revenue optics, as the company is generating substantial revenue.

Greenlane Holdings (GNLN) was a disaster of an IPO in 2019. It bottomed out in March at just 4% of its opening-day initial price! It's easy for investors to just write these busted IPOs off, but the company has been showing a lot of progress in the cannabis space, though it's buried by weakness in its JUUL business, which was down to just $4.4 million of the total $33.9 million in revenue in Q1. The company has several different lines of business and operates beyond the U.S., which makes it even more interesting. Greenlane services over 7000 B2B customers with its wholesale business, has a direct-to-consumer business, offers supply and packaging and also drop ships to third-party websites. It is increasingly developing its own brands as well.

I recently added Greenlane to my Focus List and find the stock to be quite inexpensive. The balance sheet and capital structure are quite clean, and it has ample cash from its IPO to grow its existing business. The stock, which is in the Russell 2000 index, trades at a reasonable valuation in my view, with a market cap of $152 million that is just 1.1X projected 2020 revenue and 1.7X tangible book value. The company is expected to generate $5 million adjusted EBITDA in 2021.

I have followed GrowGeneration (GRWG) since it began trading publicly in 2016. It traded on the OTC until late 2019, and it joined the Russell 2000 index last month. The company operates a chain of hydroponics stores. It estimates that approximately 75% of its business is from commercial growers. The business is very diversified geographically, and GrowGen has done an excellent job of supplementing strong organic growth with acquisitions.

After a recent capital raise as well as substantial selling by funds, the stock has pulled back from multi-year highs. With a market cap of $355 million, the stock trades at 2.5X projected 2020 revenue. It also trades at 15X projected 2021 EBITDA, which is expected to increase 66% from 2020. In April, I wrote about why I think it is a relatively safe cannabis investment, and, while the price has rallied somewhat, I remain optimistic that it will continue to perform well.

I have also followed Innovative Industrial Properties (IIPR) since its NYSE debut in late 2015. The company has raised and deployed substantial equity capital into the cannabis space, building a diversified portfolio. The management team has a record of success in the broader healthcare REIT industry, and they have executed very well to date, exploiting their position as the only large REIT to trade on the NYSE.

I find it challenging to assess the valuation and am aware of the risks of being a landlord to federally illegal tenants. Still, I understand why REIT investors would find it attractive. The stock trades at about 1.7X its tangible book value, which I find to be a bit high.

Power REIT (PW) is a relatively new entrant to the cannabis space. The company has most of its exposure outside of the sector, but it has several Colorado cannabis tenants and recently announced a $5 million investment into Maine.

Power REIT is tiny, with just 1.9 million shares as of April 24th, giving it a market cap of only $54 million, or about 5.5X tangible book value. This seems quite expensive to me, but I am not following the company closely and am not particularly skilled in assessing REITs.

Scotts Miracle-Gro (SMG) is a well known mid-cap. What's not widely known is that the company is a major powerhouse in the cannabis industry. Several years ago, it began acquiring hydroponics equipment suppliers and has assembled a business, Hawthorne Gardening Company, that generated sales in excess of $671 million in FY2019, with an operating profit of $53.5 million. Midway through FY20, Hawthorne has generated revenue of nearly $429 million, up more than 50% from the prior year and entirely organic. Operating margins have improved substantially as well. The company has provided full-year guidance suggesting Hawthorne revenue could be approximately $1 billion, citing strength in mature markets like California and Colorado as well as newer ones like Michigan, Oklahoma and Florida.

While Hawthorne is a large business, it is still a relatively small part of the overall company. Consequently, it's not a stock I follow too closely. It trades at approximately 22X one-year forward projected earnings, which doesn't appear to be a bargain in my view. I hope that the company will spin out the Hawthorne segment, creating a massive pure-play ancillary company.

Why Ancillary Companies Are A Good Option

One of the reasons why I expect investors to pay increasing attention to ancillary companies beyond the superior listing status is that it allows exposure to the industry without having to pick winners. It also gives exposure to the substantial private operators. I recently explained that it is unlikely that any MSO will gain dominant market share in the U.S. The investor base is very retail-oriented now, but, I expect that institutional investors will see these companies as a smart way to play the cannabis growth theme over the next few years.

As the cannabis sector develops, operators are forced to build very inefficient operations due to federal illegality that prohibits interstate commerce. Consequently, the operators are extremely capital intensive. Many are struggling right now due to inability to access capital, with names like Acreage Holdings (OTCQX:ACRGF), Harvest Health and Recreation (OTCQX:HRVSF) and MedMen (OTCQB:MMNFF) retrenching. The leading companies are better able to access capital, but it is quite expensive debt and sale-leasebacks, for the most part. Ancillary companies can be a lot less capital intensive, though clearly the REITs are an exception.

While they are less capital-intensive than direct operators, ancillary companies also have better access to capital due to their exchange listing status. Innovative Industrial Properties has raised hundreds of millions of dollars, including from two very recent deals. GrowGen just sold stock, raising $42 million. Akerna was able to sell a private placement convertible debenture to two institutional investors in June.

Another reason investors may favor ancillary companies is that there is an opportunity to consolidate. Akerna is already doing it, and most of the other ancillary companies are in a position to do so as well. GrowGen has executed many acquisitions to date, and Greenlane has as well. Unlike direct operators, who face state regulatory issues, there should be no barriers to consolidation for ancillary companies.

Good Performance Could Get Even Better

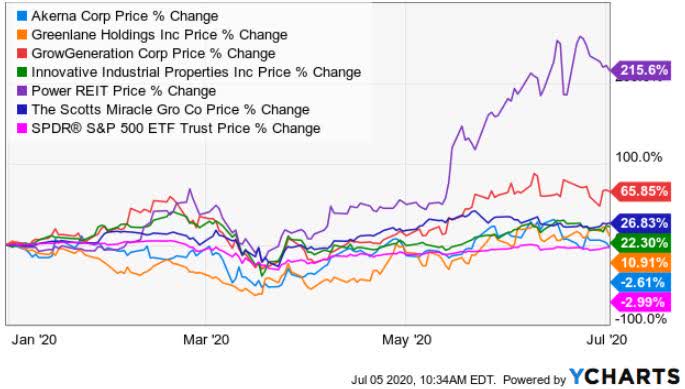

All of these companies have outperformed the cannabis sector this year as measured by the New Cannabis Ventures Global Cannabis Stock Index, which has declined more than 30% year-to-date. They have also all outperformed the S&P 500:

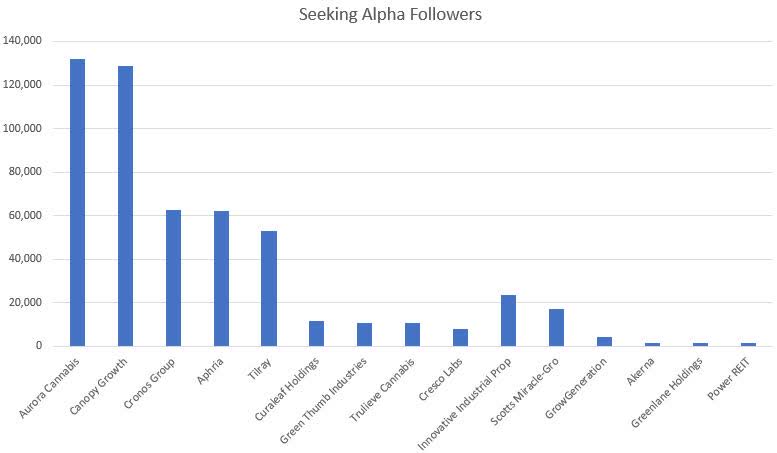

Cannabis investors seem to be overly focused on direct operators. This chart below compares Seeking Alpha followers of these six ancillary companies to five Canadian LPs and four American MSOs that all have market caps in excess of $1 billion. As I have suggested before, the Canadian LPs are substantially more followed than American MSOs. Only Innovative Industrial Properties seems widely followed when adjusted for market cap.

I recommend paying attention to the ancillary cannabis stocks, as they are performing well and are experiencing good or improving fundamentals for the most part. Investors seem to be waking up, but it seems early still. I am quite bullish on the American cannabis industry, and, if things play out as I expect, new investors who want to participate could find ancillary companies as the best way to invest given their superior listing status and other factors as well.