Cash Flow and Bank Lending

For a ten-year period beginning about 1970, I traversed the nation speaking about the importance of cash flow to bank loan officers. At that time, bank lenders relied heavily on the four C's of credit: character, economic conditions, capacity, and collateral. Character was the single most important factor, and a borrower with a known bad reputation was unlikely to receive a loan. The second most important C was collateral, since an abundance of collateral assured a loan would be repaid. Economic conditions were never certain, so it was seldom given much weight in granting a loan request.

The capacity of a commercial borrower to repay the principal and interest on a loan in a timely fashion was not easy to determine in the pre-computer era where there was a paucity of financial information. Loan officers, therefore, relied on a company's balance sheet and income statement to gauge capacity.

Lenders generally used a company's net income as a measure of funds available to repay principal and interest. Frequently, those figures were taken directly from tax returns, which bankers figured probably understated the true net income of a business.

Commercial lenders in the mid-1970s began to add depreciation to net income to measure the capacity/ability of a business to repay. This refinement was introduced because of a belief that depreciation required no cash outlay. Corporate lenders considered cash flow to be equal to net income + depreciation well into the late 1980s.

The introduction of microcomputers and spreadsheet software in the 1980s opened up a whole new way for lenders to make loan decisions. Businesses suddenly became able to keep more accurate records and were able to produce refined financial reports on quarterly and even monthly bases. Furthermore, businesses discovered they were able to do proforma statements to better determine their future loan needs. Bank lenders and bank examiners were quick to jump on the emergence of this new technology and soon began requiring proforma statements on borrowers under varying economic conditions.

Thanks to computerization, capacity soon emerged as the most important factor in measuring risk in a loan portfolio. Character, however, remained the number one reason to decline a loan, since no amount of cash or collateral could offset a bad reputation.

Cash Flow and Stock Investing

In making investment decisions fifty years ago, stock investors examined a company's history, the demand for its products, its market share, the price of its stock relative to reported earnings, its dividend, book value, and assorted ratios. The amount of financial information available at that time was spartan, expensive to obtain, and not very timely. Some elder investors, affectionately referred to as old timers, would spend all day sitting in a brokerage office and watching the ticker tape to get a feel of the market and individual companies. Others would spend hours in the library pouring over generally old financial reports and making calculations by hand on paper.

The few investors who examined financial statements focused on net income as a measure of profitability. In general, investors sought out companies with high dividend rates, stock prices below book value, and those with high growth rates. Some academics armed with university computer power began to search for the Holy Grail that determined a stock's value, while other academics embraced the Random Walk Theory, which focused on proving that investors would be as well off by simply throwing darts.

Academicians and investment professionals ultimately decided that the discounted cash flow model, DCF, was the correct way to value any stock. This theory states that the intrinsic value of any stock today is equal to the net present value, NPV, of future cash flows to be received by a stock owner. In the earliest application of the DCF model, the cash flow of a company was measured as NIAT + depreciation.

EBITDA

Anyone today who believes that NIAT + depreciation is cash flow probably also believes in the tooth fairy. People who recognized the shortcoming of this cash flow measure sought to refine it by adding interest, taxes and amortization and calling their measure EBITDA, which stands for earnings (net income) before interest, taxes, depreciation, and amortization.

EBITDA is as prevalent today as NIAT + depreciation was during the 1960-1990 period. Legions of proponents now view EBITDA as the best measure of cash flow "AND" profitability. Furthermore, they state it is the best metric to use in valuing a business.

Wouldn't it be wonderful if you could count crops as income while they are growing and selectively capitalize expenses? Well, that is exactly what outside auditors and IFRS allow cannabis companies to do.

Cash Flow and Adjusted EBITDA

Within the cannabis space, the single measure highlighted by every CEO and CFO is their company's Adjusted EBITDA. Cannabis company CEOs invariably state this metric is the single best indicator of how well their company is performing, and they generally feature it in their guidance. They imply their adjusted EBITDA is superior, since theirs should not be compared to identically named metrics presented by other cannabis companies. The connotation is almost as if they have found the secret to success in one measure.

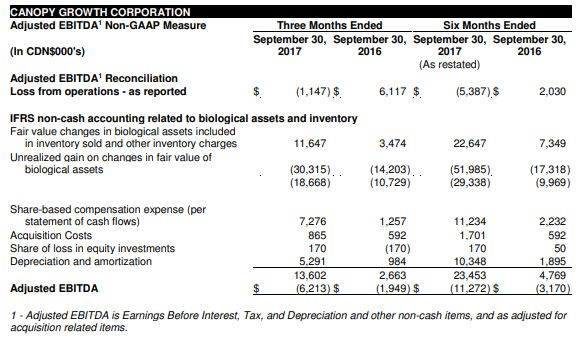

CEOs also point out their Adjusted EBITDA measure does not meet United States Generally Accepted Accounting Principles, GAAP, or International Financial Reporting Standards, IFRS. In its SEDAR filings, Canopy Growth (CGC) makes the following statement.

"Adjusted EBITDA is a Non-GAAP metric used by management that does not have any standardized meaning prescribed by IFRS and may not be comparable to similar measures presented by other companies. Management defines the Adjusted EBITDA as the Income (loss) from operations, as reported, before interest, tax, and adjusted for removing other non-cash items, including the stock based compensation expense, depreciation, and the non-cash effects of accounting for biological assets and inventories, and further adjusted to remove acquisition related costs. Management believes Adjusted EBITDA is a useful financial metric to assess its operating performance on a cash adjusted basis before the impact of non-cash items and acquisition activities."

The above qualifying statement, which is made by all other cannabis companies, is enough to set off alarm bells for any loan officer or investor. The fact is that EBITDA, whether it is adjusted or not, is neither a good measure of profitability NOR a good measure of cash flow for a cannabis company.

Canopy introduced its Adjusted EBITDA for the first time in its SEDAR filing for the quarter ending September 30, 2017. The following screenshot shows the actual presentation Canopy made in that 2017 filing.

Other cannabis companies were quick to follow in Canopy's footsteps, since it was the largest publicly traded company. Adjusted EBITDA is just another example of financial imagineering that has allowed cannabis companies to bury shareholders. The emphasis CEOs place on this metric steers attention away from a cannabis company's comprehensive balance sheet, income and cash flow statements which are carefully prepared to telegraph success and failure.

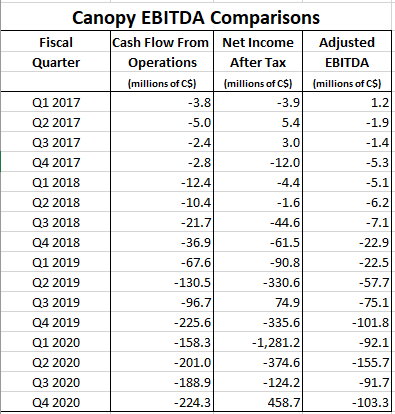

The following table shows Canopy Growth's quarterly cash flow from operations, net income after tax and Adjusted EBITDA for the past four years. The data reveal that Canopy has reported increasingly negative cash flow and Adjusted EBITDA every quarter for the past FOUR YEARS! Equally appalling is the fact that Canopy reported net losses in 12 of those 16 quarters.

These are tearful result for a company that carried the dreams of so many investors and the hopes of a nation. Totaling the above data shows that the Canopy produced a combined net loss of $2.1 billion, operating cash losses of $1.4 billion, and $749 million in Adjusted EBITDA losses during the past four years. I could have presented Aurora (NYSE:ACB), Tilray (NASDAQ:TLRY), Acreage (OTCQX:ACRGF) or virtually any other cannabis company, and the data would have painted the same bleak picture.

Conducting regression analysis on the above data is beyond the scope of this article; however, such a study would certainly reveal a poor correlation between cash flow from operations, net income and adjusted EBITDA for Canopy. A similar absence of correlation would surely be also observed for most other cannabis companies.

Cannabis CEOs who highlight EBITDA are either Sophists intent on making a bad case look good or simply unable to understand accounting. Charlie Munger, Warren Buffett's longtime partner and Berkshire Hathaway's Vice Chairman, has said EBITDA is ridiculous and has called it "bullshit", and I agree.

EBITDA Flaws

Virtually, all cannabis companies began life like Canopy Growth as Canadian corporations listed on the Canadian Securities Exchange, CSE. In that process, they decided to adopt IFRS accounting, which enabled them to record cannabis as revenue while it grew and to selectively capitalize expenses. Neither of these practices would be allowed if the cannabis company used GAAP.

The fact is that CEOs of cannabis companies such as Canopy Growth, Aurora, Aphria (NASDAQ:APHA), Tilray, Cronos (NASDAQ:CRON) and others realized that IFRS allowed them to increase revenue simply by cultivating more cannabis plants. If revenue was going to fall short, no problem, just cultivate more plants, and that would boost earnings. As revenue grew, it was easy for the Canadian investment bankers to sell more and more stock and bonds to clueless investors.

Cash Flow and Canopy Growth

I vividly recall participating in a Canopy Growth earnings conference call in the spring of 2018 and asking Bruce Linton, Canopy's CEO at that time, the following two questions:

- When do you expect Canopy Growth to show an after-tax profit?

- When do you expect to have positive operating cash flow?

After several seconds of absolute silence, Linton remarked that, like Amazon (AMZN), Canopy was laser-focused on growth, because he expected a major shortage of cannabis when full legalization was introduced later in 2018. He then added he expected Canopy to be EBITDA positive within several months. I was left with the impression he never thought about profits or cash flow.

Neither the surge in cannabis demand nor the forecast of positive EBITDA occurred. Instead, in the quarters following that conference call Q&A, Canopy continued to burn Constellation Brands (NYSE:STZ) billions without ever showing net income, positive operating cash flow, or even positive EBITDA. Canopy's cash burn rate began to accelerate in the last half of 2018, and then, it simply went parabolic along with its net losses.

The height of Linton's delusion was reached in early 2019 when he bestowed $300 million on the shareholders of Acreage Holdings for an option to acquire 100% of that company at a price that equated to about $3.4 billion. At the time of the announcement, Linton said Acreage was the leading MSO in the USA, which could not have been further from the truth.

Forensic accountants will probably date the peak in the MSO market within hours of that Canopy/Acreage arrangement. Importantly, however, the transaction, which amounted to flushing $300 million down the toilet, did not affect Canopy Growth's EBITDA. Today, it would cost only $212.5 million to buy 100% of Acreage Holdings, and it is so short of cash that it just borrowed $15 million at an interest rate of 60%.

IFRS Benefits

A cannabis company CEO does not have to be an accounting genius to play IFRS and EBITDA like a fiddle. They can produce revenue without having to sell a product; they can avoid expensing salaries and wages by capitalizing them; and they can throw cash away on stupid ventures.

The problems with IFRS are well understood by accountants and easily taken advantage of by cannabis CEOs, who falsely claim they are required to use that system of accounting. The truth is that cannabis companies incorporated in Canada are not required to use IFRS. They can switch to GAAP, but they prefer not to do so because they want to be able to play games with their income statements. They also want to continue to feature their Adjusted EBITDA numbers, thereby, drawing attention away from their deteriorating balance sheets, income statements, and operating cash flows.

The focus on EBITDA has allowed balance sheets to become cluttered with goodwill, intangible assets, leases, debt, and growing accumulated deficits. It has also enabled cannabis companies to acquire marginal assets with lengthy and questionable payback potential.

The cannabis company CEO playbook is very simple. Acquire other companies and/or licenses at elevated prices and account for such transactions by increasing fixed assets, goodwill, and intangible assets. Acquisitions increase adjusted EBITDA, since additional fixed assets increase the amount of depreciation and additional intangible assets increase the amount of amortization. It's a simple playbook; acquire more companies and licenses until you run out of other people's money to spend.

Despite the incessant focus on adjusted EBITDA or maybe because of it, very few of the 200+ cannabis companies are able to show positive operating cash flow or positive net income after taxes. Even companies with positive operating cash flow and net income fail to demonstrate that they can consistently increase the amount of cash flow and net income. They seem to reach a stage where management feels compelled to get rid of it and cannabis CEOs have shown a unique ability to waste or misallocate their cash.

Approximating cash flow and net income may have been acceptable before the introduction of computers and the explosion of financial information. Today, however, with extensive financial reporting required, there is no excuse for using approximations in the cannabis business.

The cash flow statement now required in audited financial statements is a true presentation of the cash received and expended in the operations of a cannabis company. Adding back actual interest payments in the calculation of EBITDA creates the impression that interest payments can be ignored as if they did not exist. Adding back depreciation and amortization ignores the fact that a portion of these expenses represent actual purchases of fixed and intangible assets made during the time period being reported. Importantly, the cash flow statement highlights that well over 95% of all cannabis companies burn cash and stay alive only because they are able to obtain external financing.

The following table shows Canopy Growth's quarterly cash flows, income, and adjusted EBITDA for the past four years. The data reveal that Canopy has never reported a positive operating cash flow and its negative cash flow has clearly tended to increase. That same trend is evident in its EBITDA, but that measure shows more variability. Canopy's net income exudes the greatest volatility and shows it actually reported a profit in four out of its most recent 16 quarters.

Conducting regression analysis on the above data is beyond the scope of this article; however, such a study would reveal a poor correlation between cash flow from operation, net income and adjusted EBITDA for Canopy. A similar absence of correlation would surely be observed for other cannabis companies.

Conclusion

Cannabis company CEOs have deluded themselves and bamboozled their stockholders into believing that adjusted EBITDA is the all-encompassing metric of company performance. Adherence to this metric as a measure of profitability, AND cash flow is, in fact, a clear sign that a company is on a slippery slope leading to a graveyard littered with cannabis investors.

The cash flow statements of virtually every publicly traded cannabis company have been sending SOS signals, since they were first published. All these companies mistakenly believed they would be able to obtain funds through financings ad infinitum. Now, those same companies are trying to survive by selling assets, delaying bill payments, diluting equity, and borrowing at astronomical interest rates. The fact is these companies are finished as going concerns and their stocks are worthless.

A cannabis company is like a car on a treacherous road with bad brakes and no shock absorbers. The slightest mistake could send the car careening down the mountainside.

A cannabis company without abundant surplus cash is like that car. A sudden loss of revenue due to catastrophic weather, pandemic, fire, crop failure, or other calamity would create an immediate need for cash that could last for an extended period of time. Unlike most other businesses, cannabis companies do not have lines of credit available to tide them over such periods, since banks refuse to lend to cannabis companies. A lack of cash is the Achilles heel of a cannabis company. Publicly held cannabis companies touting their growing cash position funded from operations are to be prized, while those touting their adjusted EBITDA need to be viewed with a degree of suspicion.