Canadian licensed producers finally broke a twelve-month streak of monthly declines during April, with the Canadian Cannabis LP Index rising 7.6% to 265.65, slightly lagging the S&P/TSX Composite, which rose 10.5%:

Over the past year, the index has declined 75.5%:

The index remains substantially below the all-time closing high of 1314.33 in September 2018, just ahead of Canadian legalization. In March, it posted a new 52-week closing low of 196.10, a level not seen since late 2016, and it closed 35.5% above that level. The index has declined 32.5% from its close of 393.78 at the end of 2019:

The index, which included 32 publicly-traded licensed producers that traded in Canada at the end of March, with equal weighting, is rebalanced monthly. Each of the members is also included in a sub-index, with 9 in the Canadian Cannabis LP Tier 1 Index, 9 in the Canadian Cannabis LP Tier 2 Index and 14 in the Canadian Cannabis LP Tier 3 Index during the month. Please note that at the end of 2019 we began excluding companies with a price below C$0.20 unless they generate quarterly industry revenue in excess of C$1 million. There are currently almost two dozen publicly traded LPs that fail to qualify.

Tier 1

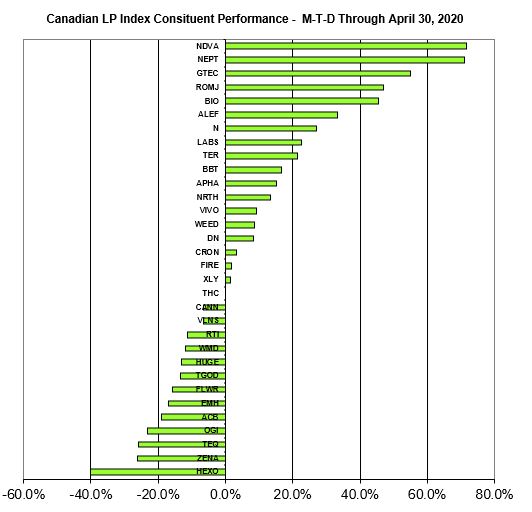

Tier 1, which included the LPs that are generating cannabis-related sales of at least C$10 million per quarter (in 2018, we used C$4 million as the hurdle), declined during the month, falling 5.7% to 371.95, which followed a 2019 decline of 38.5%, when it ended the year at 642.23. Tier 1 has declined 42.1% so far this year. This group included Aphria (TSX: APHA) (NYSE: APHA), Aurora Cannabis (TSX: ACB) (NYSE: ACB), Canopy Growth (TSX: WEED) (NYSE: CGC), Cronos Group (TSX: CRON) (NASDAQ: CRON), HEXO Corp (TSX: HEXO) (NYSE American: HEXO), MediPharm Labs (TSX: LABS) (OTC: MEDIF), Organigram (TSXV: OGI) (NASDAQ: OGI), Radient Technologies (TSXV: RTI) (OTC: RDDTF) and Valens Company (TSXV: VGW) (CSE: VGWCF). HEXO, Organigram and Aurora Cananbis all declined by more than 19%, while MediPharm Labs and Aphria were the only double-digit gainers.

Tier 2

Tier 2, which included the LPs that generate cannabis-related quarterly sales between C$2.5 million and C$10 million, posted a positive return but lagged the overall market, rising 1.4% to 410.58. In 2019, it lost 44.3% in 2019 after closing at 569.54 and is down 27.9% in 2020. This group included Aleafia Health (TSX: ALEF) (OTC: ALEAF), Delta 9 (TSXV: DN) (OTC: VNRDF), Emerald Health (TSXV: EMH) (OTC: EMHTF), Heritage Cannabis (CSE: CANN) (OTC: HERTF), Supreme Cannabis (TSX: FIRE) (OTC: SPRWF), TerrAscend (CSE: TER) (OTC: TRSSF), VIVO Cannabis (TSX: VIVO) (OTC: VVCIF), WeedMD (TSXV: WMD) (OTC: WDDMF) and Zenabis Global (TSX: ZENA) (OTC: ZBISF). Aleafia and TerrAscend posted double-digit gains, while Zenabis, Emerald Health and WeedMD posted double-digit declines.

Tier 3

Tier 3, which included the 14 qualifying LPs that generate cannabis-related quarterly sales less than C$2.5 million, soared 20.1% as it closed at 70.06. It ended at 96.76 in 2019, declining 45.0%, and is down 27.6% in 2020. Indiva (TSXV: NDVA) (OTC: NDVAF), Neptune (TSX: NEPT) (NASDAQ: NEPT and GTEC Cannabis (TSXV: GTEC) (OTC: GGTTF) all rallied by more than 50%, while just one namefell by more than 20%.

The returns for the overall sector varied greatly, with 12 names posting double-digit gains, while 11 declined by more than 10%, with the entire group posting a median return of 2.5%, well below the 7.6% average return:

For May, the overall index will have 35 constituents, as we have added CannTab (CSE: PILL) (OTC:CTABF), Rapid Dose Therapeutics (CSE: DOSE) (OTC) (RDTCF ) and RMMI (CSE: RMMI), all of which join Tier 3. Additionally, Cronos Group has moved from Tier 1 to Tier 2 and TerrAscend from Tier 2 to Tier 3, while Zenabis has moved to Tier 2 from Tier 1.