Introduction

Aurora Cannabis (ACB) reported fiscal 2020 Q3 results that showed progress on cost-cutting and stabilizing its cannabis revenue. While the company is doing everything it can to reduce cash outflow, it remains reliant on its at-the-market equity issuance program and recent share consolidation to maintain listing eligibility and liquidity. While this quarter shows stabilization, the company remains far from being profitable, and much more needs to be done to become self-sufficient without the dilutive equity program.

F2020 Q3 Review

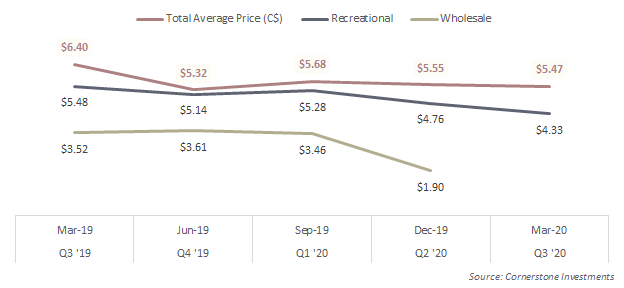

Aurora reported results for the three months ended on March 31, 2020, and the numbers looked better while showing stabilization of its operations. Aurora reported total revenue of $75.5 million which grew 35% after the 26% drop in Q2, returning sales to levels two quarters ago. The growth was driven by higher sales from the adult-use market which is consistent with what we saw at Aphria (APHA). However, gross margins remained weak at 42% before fair value adjustments which indicate continued pricing pressure due to an industry-wide oversupply. Management attributed higher sales to the launch of its value brand Daily Special and the beginning of sales of Cannabis 2.0 products. Despite the early days, it appears that 2.0 products have had a limited impact on revenue despite high expectations. We think most investors now expect the dry flower market to remain somewhat stable with moderate growth driven by an increasing retail buildout. Given the structural impediment to profitability based on current business models for most cannabis companies, 2.0 products offered hope for substantially higher revenue and better margins. So far, we have only seen a small amount of growth from LPs.

The revenue growth was entirely volume-driven in Q3 as pricing remained flat. We think the launch of 2.0 products that carry higher margins was offset by the launch of value brands. Without pricing improvement, there is no surprise that gross margin remained under pressure this quarter.

In summary, Aurora was able to stop the revenue decline which is positive. However, the 2.0 product launch has so far been underwhelming and there are few other near-term catalysts to drive higher revenue. Therefore, it is imperative for Aurora and other LPs to demonstrate their revenue potential in the next few quarters. Without revenue increases, cost-cutting alone will not be sufficient to achieve growth and create shareholder value.

Liquidity and Profitability

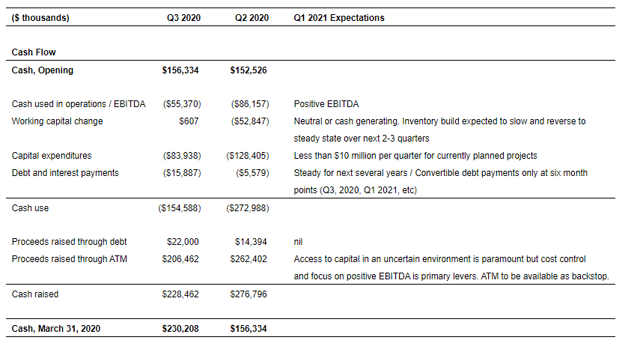

Aurora reported cash outflows from operations of $55 million last quarter, which is down from $139 million in Q2 and $95 million in Q1. The lower number was a result of aggressive cost-cutting and smaller build in working capital. In a bid to trim its deficits and right-size the operations, Aurora has been cutting costs across the organization. Management said that the company exited the quarter with $55 million in SG&A on a run-rate basis and is targeting a final number of $40-45 million including R&D. Given the level of cash burn in Q3, we think cost-cutting is an indispensable part of Aurora's plan to become EBITDA break-even for Q1 fiscal 2021. Aurora is also cutting back essentially all its capital expenditures and will target less than $10 million in spending each quarter which means no growth projects.

As Aurora focuses on cutting costs and reaching profitability, the company has been relying on borrowings and its ATM program for funding. Aurora had a total of $230 million in cash last quarter against total bank borrowings of $172 million. It also has US$345 million of convertible debentures issued in early 2019. The company issued a whopping $527 million worth of equity in the nine months of fiscal 2020 and share count increased 18.2 million (or 218 million shares before the 12-to-1 share consolidation). Clearly, the company would not have sufficient liquidity without the ATM program and it will have to continue relying on this dilutive instrument to fund its operations.

Financials and Valuations

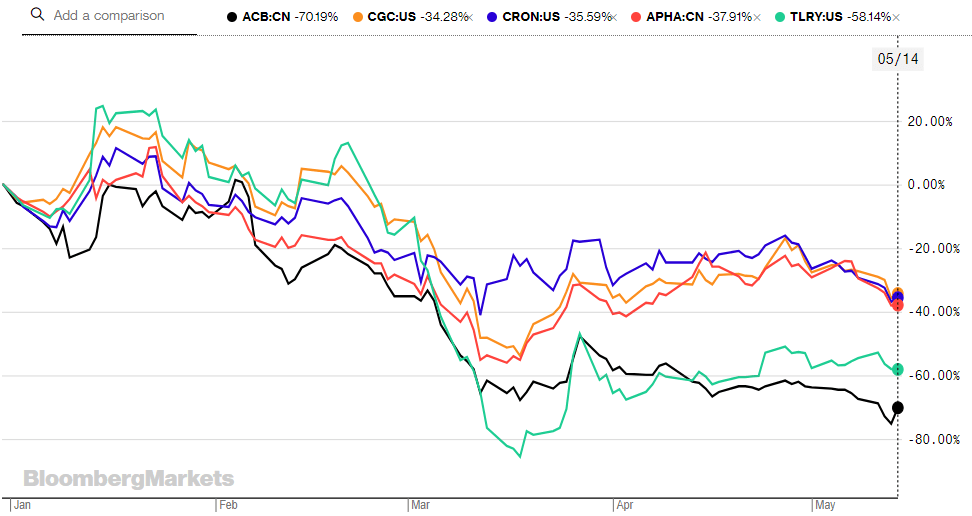

Aurora has a market cap of $1 billion which makes it the fifth-largest Canadian LP by market cap. The stock trades at ~5.1x EV/Sales which is at the low-end of its large-cap peers (cannabis-only sales): Aphria at 5.8x, Tilray (TLRY) at 9.7x, Canopy (CGC) at 14.3x, and Cronos (CRON) at 19.6x. We think the discount on Aurora's shares is justified given its unsustainable cash flow profile and heavy reliance on the ATM program for liquidity. In 2020, Aurora was the worst performer of the group and is down 70% so far.

Looking Ahead

Aurora's current issue can't be resolved overnight. The company overextended itself and spent aggressively on greenhouses that are under-utilized due to oversupply in the Canadian market. It is pulling back from previous expansions, including selling its hemp assets in the EU and Canada, and it has divested the majority of its equity investments in other companies. The company got too big but never had the revenue to support its cost structure. As a result, the current management is focusing on cutting costs while continuing issuing equity to fund its operations. Aurora issued 11.7 million shares during Q3 which equates to 12% of its total shares outstanding at the end of Q2. The constant share issuance in the public market will likely pressure its shares as long as the ATM program remains active.

While Q3 showed stabilization in revenue, the contribution of 2.0 products has been underwhelming thus far. Without a step-change in its revenue, Aurora could face an existential crisis due to a lack of liquidity and reliance on the equity market. As long as the ATM program continues, it is hard to conceive sustainable upward momentum on the stock. The key is to reach breakeven cash flow and that requires major improvements in its financial performance. For all these reasons, we think Aurora shares remain speculative and the risk/reward is heavily tilted towards the downside.