Over the last week, Aurora Cannabis (ACB) and Aphria (APHA) apparently discussed a merger with talks falling apart. A merger would've made the new entity into a global giant in the cannabis space after the Canadians have lost a ton of market leadership to U.S. firms in the last year. The synergies alone could make this a no brainer deal as Aurora Cannabis already had made an impressive transformation on costs making the long-term investment thesis on the stock more bullish.

Deal Rumors

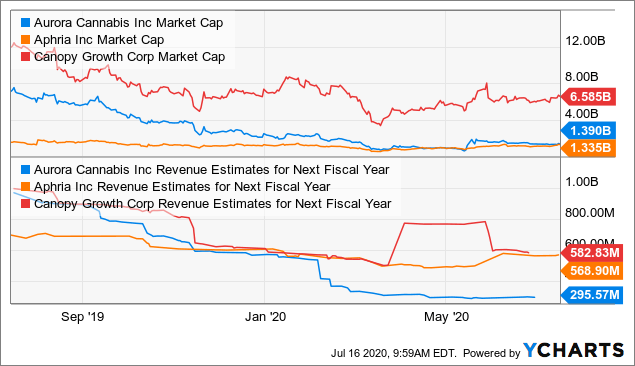

According to BNN Bloomberg, a deal between Aurora Cannabis and Aphria would value the companies at similar levels. With similar market caps, the deal would suggest a merger of equals vs. any premium for one of the stocks.

The proposed deal has some reported key terms:

- Aphria CEO Irwin Simon as the CEO.

- C$200 million in cost savings.

The news would be good for Aurora Cannabis looking for a new CEO with Chairman Michael Singer working as the interim CEO now. Mr. Simon took over Aphria back in 2019 when the company was facing a crisis and has turned the company into a leader in the Canadian cannabis sector while maintaining a positive net cash balance from building facilities with discipline.

The combined entity is now worth only $2.7 billion while Canopy Growth (CGC) had a market valuation in excess of $6.5 billion as a standalone company. Analysts forecast the companies generating $865 million in forward revenues with $220 million from the medical distribution company leaving about $645 million in the more valuable cannabis revenues. Canopy Growth is only at $583 million in revenues for FY22 ending in March.

The stock would trade at ~4.3x cannabis revenues and closer to an EV of 4.7x those cannabis revenues considering somewhere around $300 in net debt due to high debt levels at Aurora Cannabis. Aphria has a cash balance of $380 million and a net cash position of $120 million providing Aurora Cannabis with access to cash without requiring further dilution.

Investors are more focused on cannabis revenue as Aphria has C$88 million in low-margin distribution revenue from their German operations. In the most recent reported quarters, Aurora Cannabis had C$70 million and Aphria C$56 million in cannabis only revenues for an estimated 30% market share of the Canadian cannabis market.

These cannabis revenues would place the new entity on par with cannabis revenues from the largest multi-state operators in the U.S. and easily surpass the target for Canopy Growth to not even top C$100 million in the current quarter.

Efficiency Questions

The biggest question is whether the companies can actually achieve the estimated C$200 million in efficiencies, or synergies. For one reason, Aurora Cannabis just reduced their SG&A annual operating expenses to below C$190 million. Aphria has a similar SG&A run rate suggesting the deal would basically eliminate half of the current operating expenses unless a large percentage of the efficiencies comes from production costs.

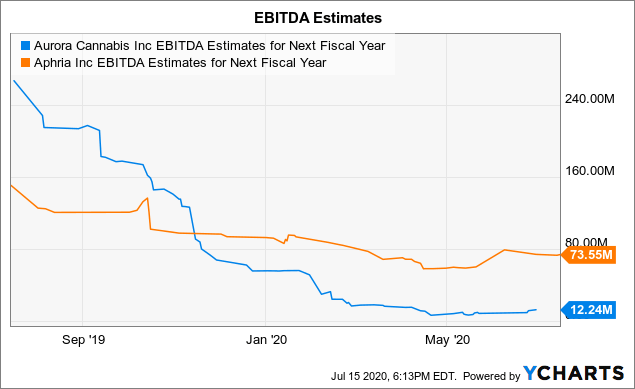

The ability to reduce costs by C$200 million would add substantial value to individual businesses both expected to reach EBITDA positive in the current quarters. For its part, Aphria was C$6 million EBITDA profitable in the March quarter and had forecasted a C$40 million target for the year as recently as January before the virus crisis.

The one potential area of strong efficiencies could be in production capacity. Aurora Cannabis just closed five production facilities to lower production costs while Aphria just opened their new Aphria Diamond facility at the end of 2019.

Over the last few quarters, Aurora Cannabis has produced far more cannabis than actually sold. In FQ3 alone, the company produced 36,207 kg of cannabis while only selling 12,729 kg while Aphria sold 14,014 kg. The combined companies only sold 26,743 kg or nearly 9,500 kg less than Aurora Cannabis alone produced.

The combined entity should be able to better match production with end user demand, but efficiency gains from controlling production levels is a small benefit and not value generating. The market already had expected Aurora Cannabis to ultimately better match production with demand. The company writing off C$140 million of inventory on a regular basis while turning small EBITDA profits in the future wouldn't even make the stock worth $1.3 billion.

The cost efficiencies could center on these production costs where the industry constantly over produces. In this case though, the ideal efficiency scenario isn't being met by a facilities-based producer merging with a strong brand lacking production scale. The companies are just using more scale to better align production with demand which was expected to occur as standalone companies.

Even just C$100 million in efficiencies, the combined entity could be looking at C$200 million in EBITDA profits before long. The stock with an EV of just $3.0 billion would have an attractive valuation and could easily see upside from 15x EBITDA estimates.

Assuming the C$200 million cost savings drop to the bottom line, the new entity could generate over C$315 million in FY21 EBITDA or $230 million. One could easily envision the stock trading at 20x EBITDA estimates providing a market cap of $4.6 billion or about 50% upside to the current stock valuations.

Takeaway

The key investor takeaway is the Canadian cannabis space has long needed consolidation. Lots of questions exist on whether Aurora Cannabis and Aphria will ultimately make a deal, but the numbers clearly support a big rally on a merger with the listed synergies. Investors should watch for consolidation in the space to generate value for the companies involved in non-cash deals.