As Aurora Cannabis (ACB) flounders below $1 now, the negative atmosphere surrounding the stock shouldn't completely overshadow the opportunities for the Canadian cannabis market in 2020. The company has substantial catalysts in 2020 including additional retail stores in Canada, the rollout of Cannabis 2.0 products and global expansion including the U.S. CBD market. This article is the second in a series of articles discussing the 2020 catalysts for Aurora Cannabis with a focus on the Cannabis 2.0 products.

Cannabis 2.0 Market Size

The research community has generally pegged the global cannabis market at nearly $200 billion within a few decades with the opportunity within Canada of around $8 billion. For now, most of the global market is limited to the North America markets of Canada and the U.S.

The Cannabis 2.0 market is a large portion of the opportunity in Canada that was restricted until December 17. Deloitte surveyed 2,000 Canadians to derive at an edibles and derivatives market of C$2.7 billion. The firm broke down the estimates by category as follows:

The numbers provide two key conclusions. The estimates don't include key vapes and edibles account for nearly 60% of the market opportunity. Cannabis-infused beverages add another C$529 million to the total opportunity leaving very limited sales for products beyond vapes, edibles and beverages.

The U.S. market provides an example of where vapes account for roughly 35% of the market with the rest of the edibles and derivative products down below 20%. Colorado is a prime example with nearly 50% of the market sales are in flower and pre-rolled joints while concentrates (mostly vapes) accounts for 32% of sales and eatables is near 16% of sales.

Based on the research of Deloitte and the problems encountered by Canopy Growth(CGC) with cannabis-infused beverages, Aurora Cannabis appears headed into the right categories. The company launched Cannabis 2.0 with 23 SKUs focused on vapes and edibles with gummies, chocolates and baked goods.

Aurora Cannabis has a large amount of SKUs to tackle the Cannabis 2.0 sector. The biggest question remains whether these products are aligned with consumer demand. The company has dark chocolate bars listed for C$10.20 each with THC infused in the chocolate limited to the 10mg government restriction.

The recent launch of Daily Special and indication that the Canadian consumer shops for cannabis-based on value suggest the company might struggle long term. According to analyst Jerome Hass of Lightwater Partners Ltd. after the launch of Cannabis 2.0 products, the illegal market offers far better values with more THC within products than the restrictions by Health Canada.

People are already talking about how expensive [the 2.0 products] are and that’s going to have to come down because people can do the math pretty quickly. When you buy a chocolate bar in five portions with 2 milligrams of THC in each portion, that won’t appeal to an experienced user.

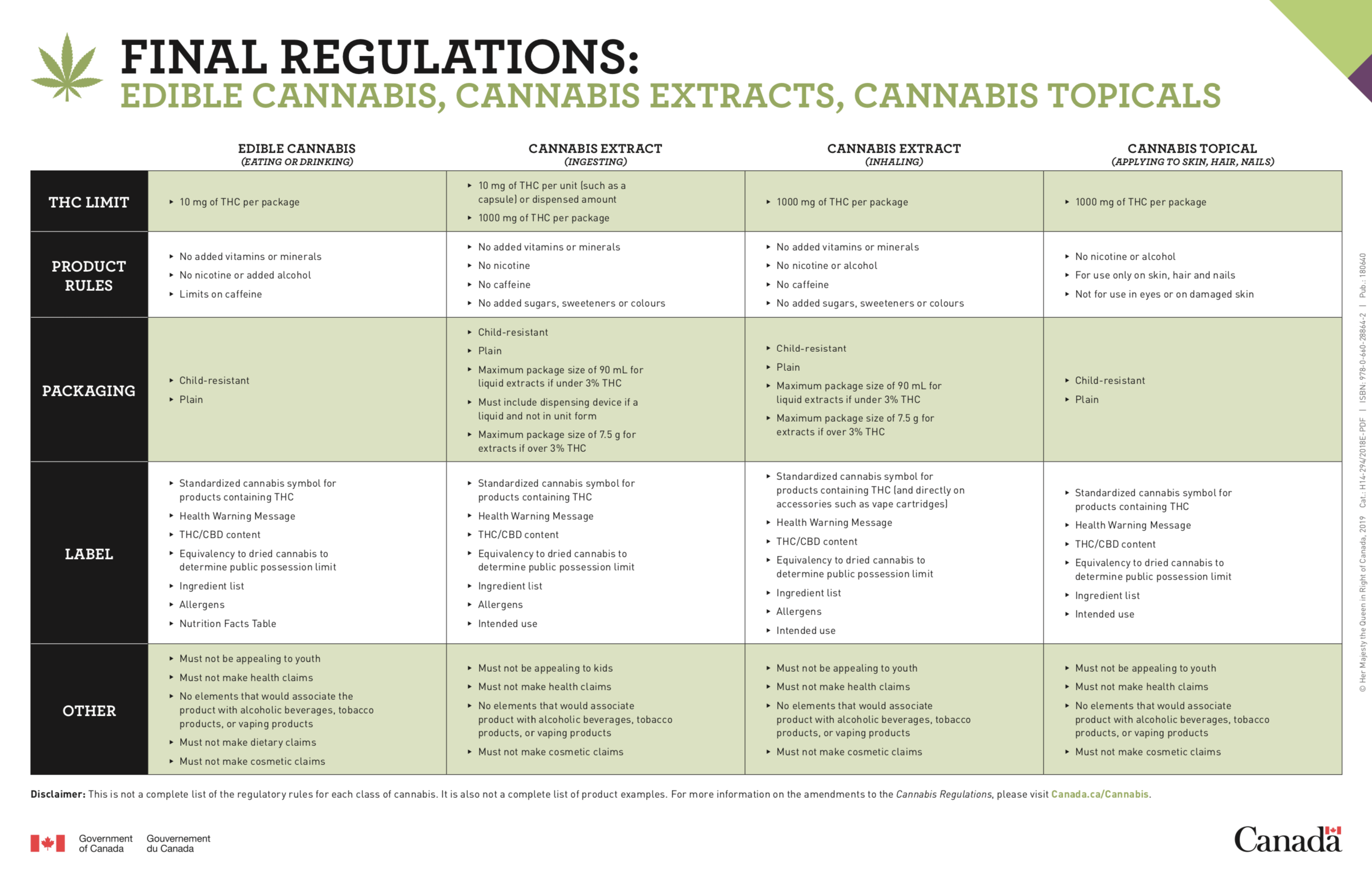

Per regulations from Health Canada, Aurora Cannabis isn't able to use more than 10 mg of THC per chocolate bar package. Some major highlights of the specific restrictions from Canada are as follows:

What the company can do is lower the price per bar by using more value brands. The consumer is likely consuming the edibles for the THC, not so much the chocolate.

Solid 2.0 Start

While my doubts exist on the long-term upside of Cannabis 2.0 products until companies alter product selections towards value options, Aurora Cannabis appeared to get off to a good start. During FQ2 that only included a few weeks in December, the company generated C$3 million in revenues.

Better yet, the forecast for FQ3 was for Cannabis 2.0 sales to account for 20% of recreational cannabis sales in the quarter. During the December quarter, Aurora Cannabis generated C$34 million in quarterly Canadian recreational sales (before provisions) and growth to C$35 million in the current quarter would lead to C$7 million in Cannabis 2.0 sales.

The problem here is the lack of meaningful growth despite the boost of both more retail stores and the addition of Cannabis 2.0 products. The big issue was the lack of a value brand during the quarter until February. Aurora Cannabis was losing market share as premium sales were shifting towards value brands so all the Cannabis 2.0 gains were lost in other areas.

The same issue could happen with the Cannabis 2.0 products where Aurora Cannabis hasn't launched value brand products. The company could again be faced with a loss of market share in a promising sector where the market shifts on the company.

The opportunity exists for a 10% to 20% market share in edibles to add C$160 million to C$320 million in additional revenues for Aurora Cannabis. More retail stores are still needed in Ontario and Quebec to reach this full potential.

Takeaway

The key investor takeaway is that the market impact from coronavirus could hit Aurora Cannabis hard. The company has a difficult liquidity position and any cannabis retail store closures would hurt a stock like Aurora Cannabis the most.

The consensus estimate is now for FY21 (June) revenues of only $325 million. Long term, the company has the potential to add nearly this amount of revenues from edibles alone.

At $0.70, the stock would actually offer some appeal with a market valuation around $1 billion due to the operating expense cut to C$45 million quarterly, but Aurora Cannabis has too many questions around capital and the weak sales environment keeps us on the sidelines until some resolution of Covid-19.