Aurora Cannabis (ACB) was once one of the favorite stocks of cannabis investors and analysts. Unfortunately, their results over the past eighteen months have been disappointing. The Canadian recreational pot market has lagged once-great expectations. Aurora has lagged behind the market further.

Aurora spends too much money. The company is cutting jobs to cut costs, replaced their CEO, is selling even more shares at-the-market ("ATM"), and is using a reverse-split to ensure its stock can keep its major-market listings. These moves are a good start towards remedying a disastrous balance sheet and horrifying cash burn, but are only a start. More work remains to be done.

Shares of Aurora trade at similar multiples to their peers. Given the challenges that management must still overcome, I will invest my money elsewhere.

Great Expectations

Aurora entered cannabis legalization with great expectations.

After announcing September 2018 quarter results, Aurora shares traded at nearly $7 per share with a market cap of over $7 billion. Many investors and Seeking Alpha writers were bullish. I sat on the sidelines, worrying about ballooning operating costs.

Analysts were optimistic. Martin Landry and Robert Fagan at GMP Securities projected Aurora sales of C$327 million in FY2019 (ending June 30, 2019) and C$804 million in FY2020. They further projected a staggering C$224 million of adjusted EBITDA profits in FY2020. This tremendous growth was to be built on the back of a strong Canadian recreational cannabis market and boisterous international growth:

| Aurora Cannabis sales | FY2019 | FY2020 | Growth |

| Canadian rec pot sales | C$181 million | C$515 million | 199% |

| Canadian medical pot sales | C$93 million | C$103 million | 11% |

| International medical pot sales | C$32 million | C$165 million | 408% |

Analysts projected strong growth in Canadian recreational pot sales and international sales.

Analysts did not bother to include balance sheet projections in their report. After all, why would the balance sheet matter? Aurora had a half-billion dollars of cash and securities, access to debt with interest rates below 6%, and euphoric markets to absorb potential equity offerings.

But the best-laid schemes o' mice an' men gang aft agley.

Hard Times

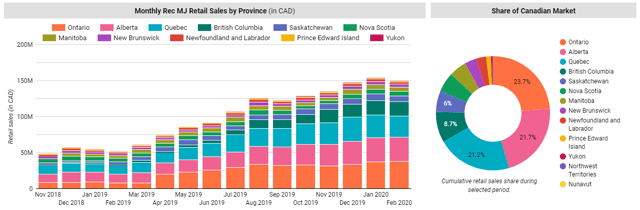

Canadian retail recreational pot sales have nearly tripled since their first full month in November 2018, growing at a CAGR of 133%

In its first full month of legalization, Nov 2018, Canadians purchased C$54 million of recreational pot. Sales have nearly tripled since then, with Canadians purchasing C$150 million in Feb 2020, growing at a CAGR of 133%.

Disappointing Canadian recreational market: Despite strong growth, the market has performed well below analyst expectations. Deloitte projected C$1.8-4.3 billion of legal recreational cannabis sales in 2019. Actual sales totaled C$1.2 billion. Deloitte's estimate was 2.6x higher than actual sales.

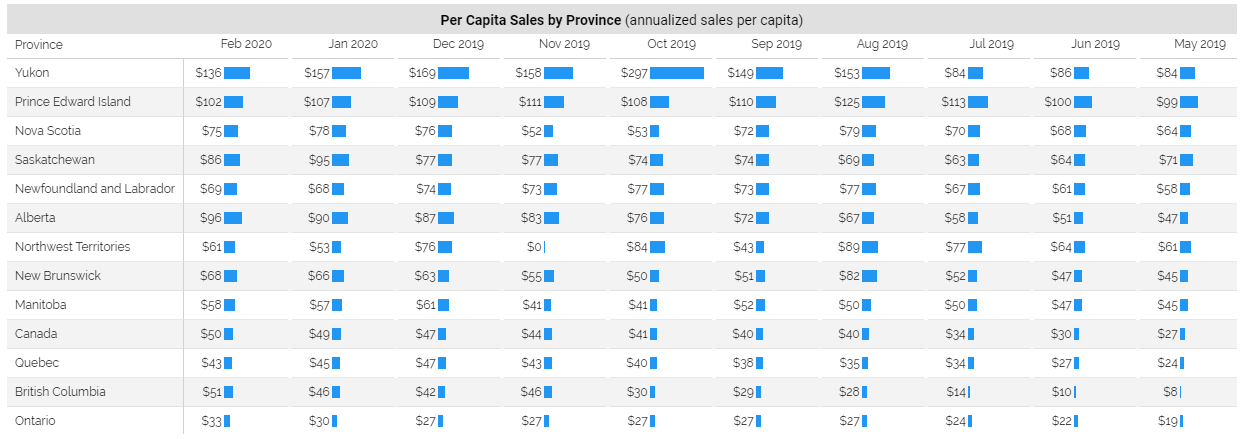

Canada's three most populous provinces have the three lowest cannabis sales per capita.

Many blame politics for these issues: Ontario for being slow to open stores and Quebec for banning vaping and raising the legal age for cannabis. Along with British Columbia, the three most populous provinces in Canada have the three lowest per-capita sales. This is not a recipe for success.

Regardless of the reasons, cannabis companies, investors, and stakeholders have suffered. Cannabis stocks (MJ) are down 59% since November 2018. Aurora shareholders have suffered even more: Aurora shares are down 89% in the same interval.

Aurora recreational cannabis sales, excluding the impact of returns, have lagged the growth of the Canadian recreational cannabis market.

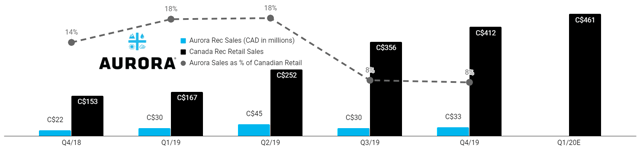

Aurora lags the market: Aurora's recreational cannabis results have been disappointing over the past several quarters.

Aurora reached a high ebb in recreational pot sales when they sold C$45 million of recreational pot (8.7 tonnes at C$5.14/gram) in the calendar second quarter of 2019. The comparison to Canadian retail sales is imperfect (wholesale vs retail, inventory build-up, etc), but Aurora's sales were 18% of the Canadian retail market.

Since then, Aurora sales have slumped. Most recently, Aurora sold C$33 million of recreational pot (4.8 tonnes at C$4.76/gram) into the Canadian recreational market--generating sales which were only 8% of those of the broader market. This figure excludes Aurora's C$11 million provision for returns, otherwise recreational pot sales were only 6% of those of the national market.

Analysts expected Aurora's FY2020 recreational sales to triple those of FY2019. Canadian retail sales in Aurora's Q2/FY20 (December 2019) grew 170%--nearly meeting analyst growth expectations. But Aurora's sales only grew 55% year over year, or only 6% if you include return provisions.

Aurora has disappointed analysts and investors.

Bleak House

Aurora spends as if there is no tomorrow. At this pace, there will not be a tomorrow.

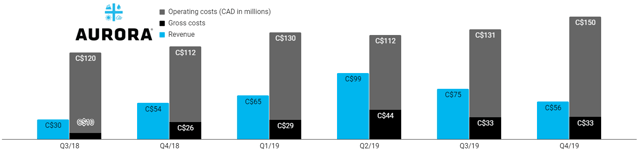

Unfortunately for investors, Aurora's poor sales growth is not the worst of the company's problems. Aurora has been spending cash as if there's no tomorrow. That prophecy may be self-fulfilling.

Over the past five quarters, Aurora has burned though C$932 million of free cash flow, with about two-fifths of that in operating cash burn and the remainder investing in cannabis facilities.

During the same period, Aurora has spent C$634 million on operating expenses while generating C$185 million in gross profits. Last quarter, management rewarded itself with C$9.9 million in compensation while shares fell 51% and the company incinerated C$263 million of free cash.

Aurora's once-safe balance sheet is in tatters

In September 2018, Aurora had C$495 million of cash and securities with C$291 million of debt--a net cash position of C$204 million. By December 2019, Aurora's debt had ballooned to C$602 million while cash flew to C$227 million--a net debt of C$375 million. Aurora shareholders also suffered through ~21% dilution as Aurora's issued share count swelled to 1.2 billion.

Dilution and job losses: Aurora has been slow responding to and adjusting for their debt crisis. However, their response is now occurring. In February and April, Aurora announced initiatives aimed at strengthening their balance sheet and lessening their cash burn, including:

- More dilution: Aurora announced a plan to sell US$350 million in shares under a new at-the-market ("ATM) program. These programs tend to limit share price appreciation due to the new shares entering the market and slowing upward momentum. Aurora's filed prospectus included only US$250 million in incremental ATM capacity. It is unclear why this disparity exists.

- Cost cuts: Aurora will lay off 500 full-time-equivalent employees, including cutting 25% of corporate staff. Aurora plans to reduce SG&A spending down to C$40-45 million per quarter by the end of the June 2020 quarter. In December 2019, the company spent C$99.9 million on SG&A, not including C$20 million of share-based compensation.

- New leadership: If the captain is steering the ship into an iceberg, perhaps it is time for a new captain. Aurora's long-time CEO Terry Booth departed in February, replaced by interim CEO Michael Singer. He plans to spend less profligately:

"I look forward to serving as Interim CEO and executing on our short-term plans, which include a rationalization of our cost structure, reduced capital spending, and a more conservative and targeted approach to capital deployment. These are necessary steps that reflect a fundamental change in how we will operate the business going forward."

Michael Singer, Aurora Interim CEO

In addition to these moves, Aurora announced a 1-for-12 reverse stock split. This is aimed at keeping the stock listed on the New York Stock Exchange. The NYSE requires a $1 minimum share price. This will reduce shares outstanding from 1.3 billion down to 109 million.

Thoughts

Aurora's moves are long over-due.

Frankly, the company has waited far too long to rationalize spending and replace free-spending management. Eighteen months ago, I lamented that Aurora's operating costs were too high. Rather than address the problem while Aurora still had C$500 million of cash and securities, Aurora instead chose to issue 350 million new shares, more than C$300 million in new debt, and spend nearly C$300 million of their cash and securities.

In short, management fiddled while share prices burned.

Aurora's cost-cutting measures are not yet enough. The company plans to reduce SG&A to C$40-45 million, cutting approximately C$55-60 million of costs per quarter. That's great, but Aurora lost C$100 million in EBITDA last quarter (or C$80 million if you "adjust" the EBITDA by pretending that dilution doesn't matter). Cutting SG&A costs will significantly reduce Aurora's losses, but will not stem the bleeding on its own.

Aurora trades at a multiple comparable to most of its Canadian peers.

Today, Aurora trades at an enterprise value of $1.2 billion USD. Analysts expect the company to generate forward revenue of $228 million USD, up only 7% from the past four quarters due to the decline of wholesale sales and continuing price pressure. The company is not expected to make an adjusted EBITDA profit for three more quarters.

This valuation is comparable to Aurora's peers. Given the challenges in front of Aurora, I see little reason why the company might deserve more of a premium over its peers. Given the tremendous values available all over the stock market, including in blue-chip companies with a history of profitability, I do not plan to invest my hard-earned money into this struggling Canadian pot stock.

Happy investing!