On a profitability, growth, solvency, and liquidity basis, Aphria (APHA) demonstrates itself to be the strongest company operating in the Cannabis business. Despite strong operating metrics, Aphria trades at a discount relative to its comps group across several different valuation multiples. While Q1 earnings were slightly below estimates, the stock price greatly overreacted. This gives investors an opportunity to enter the best stock in the space at an attractive price with 30-70% projected upside as suggested by my multiples valuation analysis or via selling cash secured puts to capitalize on high volatility.

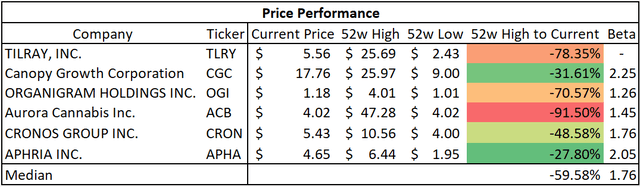

While equity markets have rapidly recovered since March and April lows, the cannabis sector at large has only traded in one direction since the onset of the pandemic: down. The S&P is up roughly 16% over the past year, while ETFMG's Alternative Harvest ETF (MJ) is down more than 44% over the past 12 months. Much of this negative price pressure has been driven by the overall unwinding of the bubble in the cannabis space. In late 2018, we saw hot marijuana stocks like Tilray (TLRY) and Aurora Cannabis (ACB) trading with multi-billion dollar market caps with very little to show for it (both now down 90%+ from their 2018 highs). While some might be tempted to go dumpster diving for deals, I urge caution: some of these companies are trading for next to nothing for a reason.

From the above table, it's clear that Aphria, while still down in the past year, has fared the best out of its competitors. Despite being the best performing bunch of the group, Aphria stock crashed on October 14th's Q1 earnings upon missing sales estimates and higher excises taxes year-over-year. However, long-term investors should see this as an opportunity to gain from a short-term market overreaction. The fact is that relative to Q1 of last year, Aphria still grew revenue to $145mm CAD this year from $126mm CAD; the former of which was accomplished in peak pandemic and shelter-in-place. While missing estimates, I see the fact that revenue still grew while only narrowly missing profitability (-3.4% Q1 2020 profit margin) in the middle of a global pandemic as an accomplishment, especially when comparing it to key metrics of its competitors, which are spectacularly bad:

From a business strategy perspective, Aphria is unique in that it's focused on growing its core business in Canada while also planting operations internationally in order to build out their distribution network as regulatory approval is cleared for international operations. Aphria currently has operations in Germany, Italy, Malta, Colombia, and Argentina in addition to key business relationships in Israel, Poland, and Denmark. While other Cannabis companies might be eager to burn cash (especially two years ago), Aphria shows discipline in their approach, emphasizing maximizing growth as well as profitability and cash flow in their Q1 MD&A.

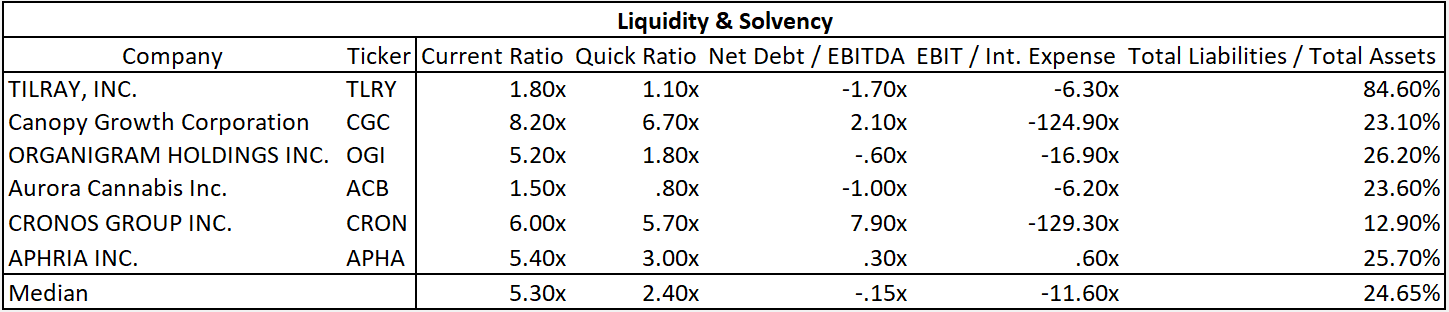

The Cannabis space is a bet on growth; there is little value to be found in companies with triple (or quadruple) percent negative net income margins. Aphria is the only company from its comps group to successfully straddle the line between growth and profitability. While the growth-at-all costs strategy might pay off in some cases in the technology world, the fact is that the companies in the marijuana space generally offer only slightly differentiated products. It's more of a commodity business than a business featuring distinguished products; thus, a clear road to profitability is critical for long-term survival. Aphria demonstrates higher-than-median year-over-year revenue growth all while proving the most profitable (or more accurately, least unprofitable) among its peers. Note that Cronos' large positive net income margin is from a derivative liability revaluation in 2019 (i.e. meaningless). Aphria is also the only company in the group to demonstrate positive gross margins and positive EBITDA margins. Given the importance of high gross margins in a commodity-type business (keeping more dollars for every dollar sold), Aphria is the clear winner when it comes to growth and profitability metrics. Looking next to liquidity and solvency, Aphria yet again shows its strength:

Looking at its liquidity, Aphria has one of the highest current ratios (its current assets cover current liabilities more than 5 times). On a quick ratio basis (same as current ratio but taking out inventory from current assets), Aphria still has better-than market liquidity, able to cover its current liabilities more than three times on a quick ratio basis. In COVID times, cash in hand is a key safety net for any company, especially those struggling to remain profitable (or operational) in the cannabis space. Looking at solvency metrics like net debt/EBITDA and EBIT/interest expenses are meaningless for many of the companies listed here due to negative EBIT and EBITDA, so I do not see this as a metric suitable for comparison. However, on a total liabilities to total assets basis, Aphria's capital structure shows leverage that's in range with the industry median. Given its exponentially better operating metrics, if anything Aphria has capacity for more leverage relative to its competitors if it wanted to do so. From a liquidity and solvency perspective, Aphria yet again shows to be the best of the bunch.

However good Aphria may be, what matters at the end of the day is valuation. Yet again, Aphria delivers:

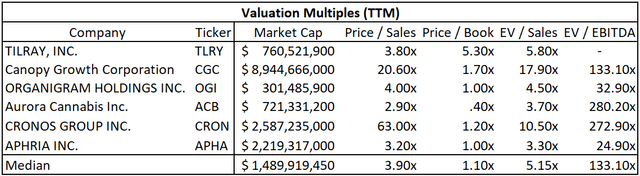

Starting off with Price to Book multiples, Aphria is trading just under the median industry P/B multiple. A price to book multiple is price per share divided by equity per share. Essentially, it's what you're paying for a dollar of net assets (equity). While Price to Book might make sense when valuing industry with heavy assets (i.e. freight, railroads), many of the Cannabis competitors listed might have near-zero equity numbers due to years of losses. Therefore, price-to-book produces relatively meaningless multiples. Similarly, EV/EBITDA struggles as a reliable valuation matric in the cannabis space due to many companies with negative or extremely small EBITDA figures, thus inflating the multiples to meaningless levels.

The two most meaningful valuation multiples I see for the industry are Price to Sales and EV to Sales. Given similar cost structure to many of the firms in the space, I see a multiple based on sales as the most reliable given the relative stability of sales versus volatile (and often) negative earnings figures. On a price to sales basis, Aphria trades at a discount relative to its comps group, all while demonstrating better operating performance. Today, you'd be paying $3.20 for every dollar of revenue Aphria generates, which is a steal relative to its competitors and especially relative to other growth-focused businesses (for example, in software you might see revenue multiples of 15x+).

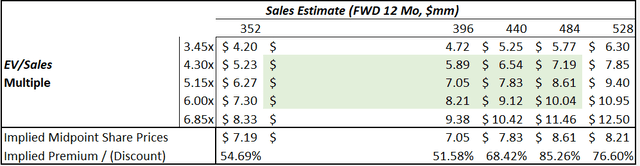

An EV/Sales multiple is similar, except EV includes both equity and debt (less cash and cash equivalents). Thus, companies with attractive P/S multiples but with huge amounts of debt will see inflated EV/Sales multiples (in other words, EV/Sales helps verify whether the price to sales multiple is driven strong operations or debt). On an EV to sales basis, Aphria demonstrates even more of a discount relative to the group median at 3.3x versus the 5.15x median, showing its attractive valuation is driven by its core business operations, not inflated debt levels.

The valuations speak for themselves: Aphria is selling for cheaper than its competitors while showing much stronger financial performance. I see this as a market mispricing to take advantage of.

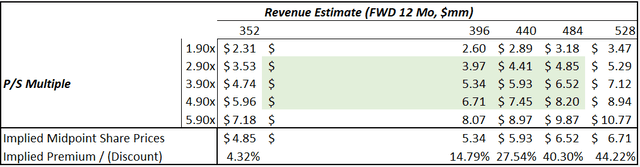

Using my own sensitivity analysis, I project Aphria's implied share price on a price to sales and EV to sales basis:

Q1 2020 revenue was $145mm CAD, or $580mm CAD annualized. Converting that to USD is $440mm and serves as the midpoint of my sensitivity analysis. Using $440mm USD as forward 12 month revenue is a relatively cautious estimate, as it assumes the company will experience no growth in the next 12 months (I'd see the right side of the table as more realistic, although I try to be conservative in my projections). Taking the current median market Price to Sales multiple of 3.9x, we arrive at an implied share price of $5.93 - almost 30% upside from where we are today (assuming zero revenue growth going forward). On an EV/Sales basis, the upside is even more attractive:

Assuming the median EV/Sales multiple and the no-growth forward revenue scenario, the implied equity upside is nearly 70% for a share price of $7.83 USD (assuming midpoint multiple and revenue estimate).

From the sensitivity analysis, it's clear that despite its share price holding steady relative to its peers over the past month, key market multiples are suggesting undervaluation and implied upside of 30%-70% on a price to sales and EV to sales basis.

While directly investing in the shares is a great opportunity, the risk and uncertainty of investing in the cannabis space must be noted. Given Aphria's beta (systematic risk) of over 2 relative to the S&P 500, some more risk-averse investors might find selling puts on Aphria as a more attractive way to gain exposure to the company. Given generally elevated market volatility (VIX > 25) and implied volatility of the stock, option premiums are relatively high right now. Given the low share price of Aphria (single digit), selling puts can be a win-win for the everyday long term investor in this market. If the stock increases, you keep a nice premium, and if the stock dips you purchase the equity at an even more attractive cost basis.

Given the market undervaluation, strong operating metrics, and solid liquidity and solvency, I see Aphria as a strong buy as of today's prices, either directly in the stock or via selling cash-secured puts.