Aphria (APHA) continues to make smart moves to position the company for catalysts ahead for the Canadian cannabis market. Government regulations continue to restrict the growth potential of the market, but the country is slowly opening the market up for several catalysts by midyear. The cannabis company opportunistically raising more cash should prove wise in a market where competitors will likely face liquidity crunches right as the market improves.

Equity Raise

Aphria was already in a strong capital position with one of the highest cash balances in the Canadian cannabis space. Investors were probably surprised to see the company raise more funds with some skepticism of the reasons.

The company announced a deal with a strategic institutional investor to raise C$100 million by selling 14,044,944 units at C$7.12 per share. Each unit gives the investor one common share of Aphria and one-half of a warrant to purchase shares at C$9.26 per share.

The stock price comes out to $5.46 with Aphria ending the prior day at $5.77. The stock is selling off on the news along with the general market weakness due to fears over the coronavirus in China.

Aphria now has C$600 million in cash on the balance sheet. Only Canopy Growth and Cronos Group have larger cash balances in Canadian cannabis space after making large strategic deals prior to the market peak in 2019.

Also worth noting, the company has C$490 million in debt outstanding so the net cash position is only C$110 million now. The current market valuation is ~$1.5 billion so the equity raise of $75 million comes out to an ~5% share dilution to improve the balance sheet.

Poised For Market Share Gains

The big issue facing the Canadian LPs are the timing of 2020 catalysts. Aphria such announced vapes available for all of the provinces allowing their sales, but Ontario, Alberta and Quebec all have various restrictions that will reduce sales via a combination of restrictive regulations or a lack of retail stores.

The strong cash balance sheet allows Aphria to aggressively use the new production from the Diamond One facility to grab market share. The new facility should have product on the market in March allowing for market share gains in the FQ4 quarter that ends in May.

The real upside from all of these catalysts isn’t likely until the August quarter. Either way, analysts have quarterly revenues reaching C$160 million in the May and August quarters. These revenues targets are up from the C$121 million just reported for the November quarter.

The company cut revenue targets for the year to a low of C$575 million while analysts now have estimates down below C$535 million for the year ending n May. The risk here is Aphria actually needing to cut estimates for the year again, but the company should now have the resources and the market opportunity with new Ontario stores hitting the market along with Cannabis 2.0 products to grow revenues sequentially.

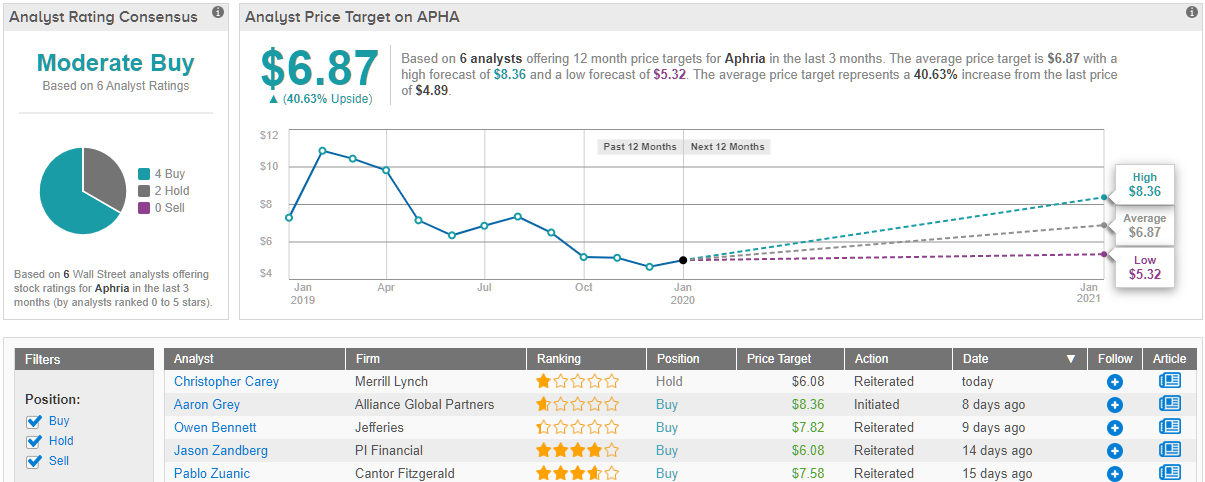

Wall Street's Verdict

Wall Street’s analysts are sanguine about this stock’s ability to gain going forward. Aphria's Strong Buy consensus rating is based on 4 Buys and 2 Holds. It doesn’t hurt that its $6.87 average price target puts the potential twelve-month rise at ~40%.

Takeaway

The key investor takeaway is that Aphria has the cash position to survive and thrive the regulatory hurdles temporarily slowing cannabis sales in Canada. The current cash balance above C$600 million and the new Aphria Diamond facility provides the assets to take market share while competitors struggle with liquidity. The company has the financial flexibility to grow revenues going forward making the stock the best buy in the sector near $5.