With legalization of marijuana complete in Canada, currently making strong progress in the U.S., and the passing of the 2018 Farm Bill, the cannabis market is positioned to become a behemoth of an industry on every level. With a rapidly growing sector like this, however, comes growing pains consisting of increased competition, lower margins, and heightened regulation. This paves the way for seed-to-sale cannabis companies focused on providing governments and companies with the necessary tools to keep up. One company that is on track to become one of the leaders amongst seed-to-sale companies is Akerna (KERN).

Akerna is a cannabis compliance technology provider and developer of the cannabis industry's first seed-to-sale enterprise resource planning software technology. KERN aims to be the backbone of the cannabis industry by providing local governments with regulatory compliance software through its Leaf Data Systems software and providing cannabis companies with commercial inventory management through its MJ Platform. The company generates revenue through both platforms along with a consulting business targeted towards companies entering the cannabis industry, however, their bread butter has always been its MJ Platform.

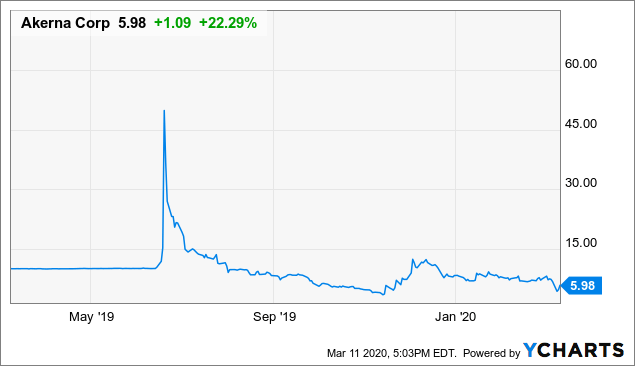

As the first cannabis compliance technology company to be publicly traded on the NASDAQ, Akerna had an interesting path to the public markets that investors should be aware of. KERN went public through a SPAC (Special Purpose Acquisition Company) led by Scott Sozio called MTech Acquisition Corporation. MTech Acquisition completed its acquisition of MJ Freeway in June of 2019 and quickly jumped to a high of $72.65 from $10 a couple days after trading began, with a huge sell off bringing the company to a low of $3.16 with current trading at a price level of ~$6. The extreme volatility was due to the company's small 4.5 million float and 11 million shares outstanding along with the mass hype of it being the first U.S. SPAC for an ancillary cannabis business.

With the float and outstanding share count only slightly increased from the time it went public, warrants priced at $10 & $11.50 attached to the SPAC still in place, and economic uncertainty due to the Coronavirus cases, investors should expect volatility in either direction. However, I believe that the company's business fundamentals and prospects in the cannabis industry will weather the storm over the long run and give investors a great return on their investment.

Investment Thesis

Many investors are on the edge of taking a leap of faith with Akerna due to external variables and others believe they are overvalued relative to their current business model. In my view, the company's long term bullish case relies on these various factors:

Great potential for disruption in the cannabis space. Akerna is only one of two publicly traded cannabis seed-to-sale companies and the only company trading on the NASDAQ, with Helix TCS (OTCQB:HLIX) as the other competitor. Their technology platforms, such as MJ Platform and Leaf Data Systems, are on the path to becoming a standard for state governments and commercial companies as the industry matures in the U.S. and around the world.

Steady growth in a time of industry shake ups. Akerna recently came out with its Q2 2020 earnings and sported solid top line growth of 28% to revenues of ~$3.3 million led by the expansion of their MJ Platform and consulting segment. The ability of the company to continue its growth during a rough patch for the cannabis industry shows the necessity for its technology. Growth can only go up from here as de-regulation and consumer adoption for cannabis improves.

Future benefits to come with recent acquisitions. In the past couple of months, Akerna has gone on a spending spree by acquiring and making strategic investments into companies that will further push their growth throughout 2020 and beyond. KERN acquired Ample Organics for $45M, acquired a majority interest in privately held Solo Sciences, and made a strategic investment in ZolTrain. I will discuss the benefits of each company later on.

Undervalued relative to the rest of the market. KERN is currently trading at a 3.7x revenue multiple, far below the average tech company when considering how fast the industry they are serving is growing. Based off FY2020 financial projections and growing adoption of their products, investors could conservatively see share prices double in the near future.

In order to understand KERN's growth potential, it's important to take a deeper dive into their recent 10-Q.

Q2 Results

Shares of Akerna dipped slightly on the day of announcing their Q2 2020 earnings but has stayed trading in relatively the same price range as it was before as investors are still trying to make sense of their results and how it will translate to future price appreciation.

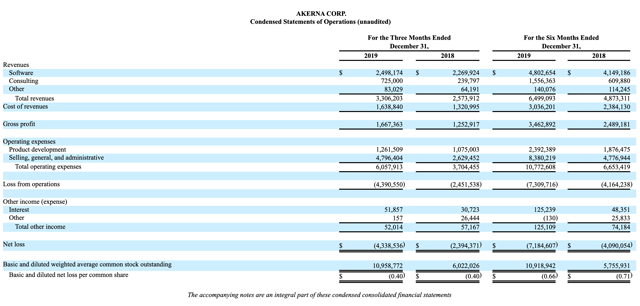

KERN's revenues grew ~28% Q/Q to $3.306M for Q2, led by a 202% increase in fees from its consulting service. Akerna provides consulting to cannabis industry operators interested in integrating their platform with MJ Platform, which will vary over time as marijuana becomes legal on a federal level but has provided a strong cushion for its revenues as the company is focusing on its acquisition strategy that will provide for rapid growth. The Leaf Data System was flat Y/Y but should give Akerna great revenue growth in the coming years as more states begin to adopt legal medical and recreational marijuana laws. A strong feature of this revenue growth can also be attributed to the industry's adoption of their MJ Freeway software as revenues from that were up 29%. The company saw a strong gain in this commercial software due to increased volume of new business, including new clients and upgrades from existing clients, all while investing in new technology to further expand their offerings.

KERN's gross margin increased slightly to 50% for the quarter showcasing the company's path to internal cost efficiency on their software products and consulting business. Total loss from operations expanded to -$7.31 million for the six months ended December 31, 2019, compared to a total loss from operations of -$4.16 million for the six months ended December 31, 2018. The expanding losses might scare many investors, especially as the rest of public companies involved with cannabis are constantly losing money with no path to profitability, but this will work in an investor's favor as the majority of the losses were due to increased costs in product development behind the MJ Freeway and Leaf Data Systems software. It's important to remember that Akerna functions as a technology company providing services to an industry that has yet to realize its full potential so the increased R&D spending along with unprofitability will be a normal feature in the near future. Where investors can really get in early and watch it grow is when the company is focused more on improving current products and expanding new ones rather than focusing on profitability, which is now.

KERN also has a healthy balance sheet compared to competitors in the cannabis and technology sector, with roughly $18 million in cash on hand as of December 31, 2019, a current ratio of 7.20, and zero debt. It's as clean as it can possibly come and is miles ahead of other capital structures from competitor's such as Helix TCS. Take a look at some balance sheet metrics from the two (not including goodwill and intangible assets):

| KERN (as of 12/31/19) | HLIX (as of 9/30/19) | |

| Cash | $18.7M | $655K |

| Total Assets | 22.3M | 4.7M |

| Total Debt | - | 2.8M |

| Current Ratio | 7.20 | 0.43 |

They haven't raised any equity capital since going public in June and having $18 million in cash on hand should be sufficient to get them through the year, based off the assumption that they will continue their cash burn of $3 million per quarter with some wiggle room if they make any more acquisitions or increase operating expenses. This puts them in a position where they don't have to go out and dilute their shareholders through a large raise, keeping their share price in a tight range with the only equity market risk being the overhang of their warrants and issuance of stock with their acquisitions.

Akerna's CEO, Jessica Billingsley, notes the strong financial performance for the quarter along with the strategy behind their acquisitions and how that will lead to the company becoming a powerhouse amongst all the other seed-to-sale cannabis companies. Per Billingsley's remarks:

Our results for the quarter ended December 31, 2019, continue to be illustrative of the continued adoption of both MJ Platform and Leaf Data Systems by cannabis enterprises and government entities. With cannabis legalization continuing to expand and our recent acquisitions of both solo sciences and Ample Organics, Akerna is well positioned to serve the increasing compliance needs of enterprise cannabis companies, governments, and consumers. Transparency remains critical, as regulatory requirements will only grow to ensure public, product, and patient (or consumer) safety."

Although KERN has a small float and the volatility in the cannabis and overall market has increased in the past month or so, share prices haven't really been affected by their Q3 earnings. Investors are still trying to weigh in the risk to reward potential on Akerna after posting decent Q2 results but I believe they should take all the numbers with a grain of salt and put more diligence on their growth with the business model and future of the cannabis industry. There is a great buy opportunity in place for investors looking at longer term gains (1-2+ years) but should proceed with caution as well due to its nature of being in growth phase right now.

Acquisitions

Throughout the past couple of months, Akerna has gone out and made some really beneficial acquisitions and investments that will help expand product offerings, implement new additions to its commercial and regulatory software, and help the company expand into new countries. To understand the benefits, I'll discuss these three acquisitions and investments: Ample Organics, solo sciences, and ZolTrain.

-Ample Organics: Ample Organics is a seed-to-sale Canadian cannabis company that serves over 70% of the Canadian market and was recognized as the 19th fastest growing company in Canada by The Globe and Mail in 2019. Ample Organics is on track to generate revenues of $8.7 million for FY2020 which could potentially launch Akerna into profitability by offsetting their costs associated with R&D. KERN has a definitive agreement to acquire them in a cash and stock transaction valued at $45 million. With Canada being the largest national market so far, KERN is now in a great position to penetrate that market and will have one of the largest market shares in the region. This acquisition is also the beginning for Akerna to expand its footprint globally and create an interconnected network and supply chain for the cannabis market. Once the deal officially closes, I believe Akerna will be in a position to be at the forefront of seed-to-sale cannabis technology companies, both on a quantitative and qualitative level.

-solo sciences: On January 21, 2020, Akerna completed its majority interest in solo sciences. solo sciences a privately held company that develops patented anti-counterfeiting and consumer engagement technologies, with solo*TAG being their main product. solo*TAG is marketed as being the alternative to the traditional, expensive RFID technology used by states for their state tracking system and is also more secure and less expensive that traditional RFID technology. The technology will be implemented into both the MJ Freeway and Leaf Data Systems platform, but will most likely be more useful in helping KERN win contracts to provide states with their Leaf Data Systems technology. solo*TAG's implementation with Leaf Data Systems is going to tighten up security for the state's tracking system of cannabis which ultimately adds a sense of comfort for the state. For example, Akerna won its contract with Utah's Department of Health and Department of Agriculture through its collaboration with solo sciences. Keeping the regulatory environment constant, we should see a boost in revenues from the Leaf Data System throughout this year and next year.

-ZolTrain: In October of 2019, Akerna made a strategic investment into ZolTrain, a training platform for the mobile world. It will be implemented into the MJ Freeway platform with the goal of putting cannabis brand training under control of the budtender at dispensaries and provides information at the point of sale through the software. Budtenders are the middle man on the retail level, as they are the link between brands, compliance, and sales so ZolTrain through the MJ platform will now allow bud tenders to be able to quickly learn about a specific brand and have access to the product information through the software. Dispensaries and retail brands will love this because bud tenders will now be able to make the best recommendations to customers and drive loyalty all while keeping track of compliance. This may not seem like a major change, but it is the small stuff like this that will separate Akerna from its competitors over the long run.

So with these three acquisitions and investments being completed within the past couple of months, KERN will have some of the best seed-to-sale softwares for both companies and regulators and will begin to service the international cannabis markets as well. Over time, investors will slowly start to see an increase in both top line growth and brand recognition amongst the cannabis community. Akerna's aggressive expansion mode with these acquisitions is something investors should definitely consider when looking to buy KERN stock.

Valuation

At present share prices around ~$6 and 10.9 million shares outstanding, Akerna trades at a market cap of $65.4 million. After netting out the $18.7 million of cash and no debt on KERN's balance sheet, we are left with an enterprise value of $46.7 million.

With the prospects of a large-cap company and becoming a leader in one of the fastest-growing markets, Akerna is now considered a micro-cap company based on their current equity and enterprise value. They currently trade at 3.7x LTM EV/Revenue while the majority of technology companies trade between 8-15x LTM EV/Revenue.

Assuming a conservative projected FY2020 revenue of $12 million plus $8 million in projected revenue from the Ample Organics acquisition, KERN is currently trading at 2.4x FY 2020 EV/Revenue further showcasing how undervalued this company is just based off its multiples relative to their industry. Factoring in its rapid growth that will coincide with the rest of the cannabis industry, a 10x EV/Revenue multiple, in line with other technology stocks, would equate to a price target of roughly $20. This is not factoring the dilution that could occur from the 5.8 million warrants priced at $11.50. Nevertheless, these conservative numbers and valuations present a 100%+ upside from current share prices and investors could potentially see their investment triple or quadruple over the next couple of years.

Akerna's low valuation relative to their competitors and the future growth of the cannabis industry leads me to believe that the company is currently extremely undervalued. Even with the future dilution from their warrants along with the stock issued in their acquisitions, KERN prevents a great buying opportunity for every investor. And if the coronavirus and overall market conditions send the company's share prices lower, you'll know that the buying opportunities will only get better and provide a beefier return for long term shareholders.

Risks

Although every aspect of Akerna's business fundamentals, industry growth, and share price lead me to believe the company is extremely undervalued with the potential for huge upside, there are risks surrounding the company currently.

One main risk for Akerna moving forward is their Leaf Data Systems' ability to win state government contracts, as competitors Helix TCS and Tiger Global-backed Franwell's Metrc are on the same playing field as KERN. Helix TCS is currently serving 10 states and Franwell's Metrc is serving 13 states. If Akerna is not able to continue beefing up their regulatory software, they might not be able to keep up with the competition and could see a decline in revenues. This would be a major hit as 39% of KERN's FY 2019 revenues came from its Leaf Data Systems' software.

Another risk to shareholders and potential investors is the overall market environment and volatility due to the Coronavirus, COVID-19. The Coronavirus has now been classified as a worldwide pandemic by WHO and has been disrupting supply chains all across the globe. Schools, sporting events, and workplaces in the U.S. have begun to take a hit from this pandemic and we could potentially see the economy head into a recession over the next year or so. On top of that, the Dow Jones Industrial Average has touched into bear market territory and the volatility in the markets has taken KERN's stock on a ride over the past week. If these overall economic conditions continue and take a hit on the cannabis industry, I will re-consider my bullish thesis on Akerna as their growth will begin to slow down as well.

Conclusion

I believe that Akerna is a great company that is early on its growth phase. Their MJ Platform and Leaf Data Systems software will become the backbone of the cannabis industry throughout the world and will be further complemented with the acquisitions and investments they make. Shares are currently undervalued with the potential for huge upside so investors that are looking for growth stocks with long term potential should definitely take a look at KERN.