Investors are constantly searching for the next big winner. We mean the stocks that are on track to see explosive growth, handsomely rewarding the investors that managed to get onboard at the right time. But how are investors supposed to know when it’s time to snap up the right stock?

When first approaching this task, investors will often turn to names during or on the heels of an impressive rally. However, Wall Street analysts note that this isn’t always the best move. Instead, the Street’s seasoned pros tell investors that compelling investments can be found among names that have stumbled lately. Rockiness in share prices can present a unique opportunity to get in on the action before the stock heats up.

Taking this into consideration, we used TipRanks’ Stock Screener tool to pinpoint 3 tickers with strong growth narratives that remain intact despite recent weakness. If this wasn’t promising enough, each of the names has received enough bullish calls in the last three months to be given a “Strong Buy” consensus rating.

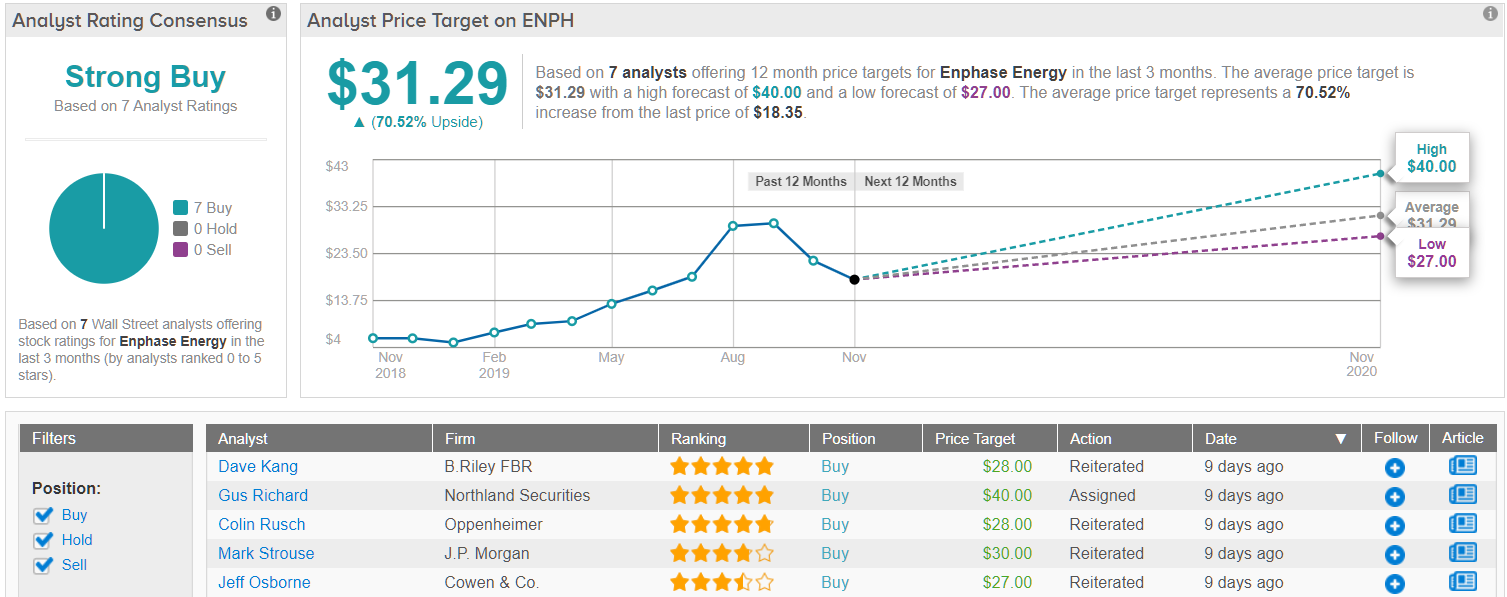

Enphase Energy (ENPH)

Investors are desperately trying to understand what’s going on with Enphase Energy. Known for being the leading provider of solar microinverters, the company has seen shares tank following a period of massive growth in the first half of the year. Nonetheless, one analyst states that concerns regarding ENPH have been blown out of proportion.

Roth Capital’s Philip Shen points to a report published by Jcap as the partial source of recent shakiness. The primary assumption made in the report is that ENPH has seven months of inventory left in the channel. Shen responded by calling this claim “simply nonsensical”, with his estimates putting the actual inventory levels at 3-4 weeks.

Adding to the good news, the analyst wrote in a note to clients that the U.S. residential market is expanding much more quickly than previously expected.

“We continue to believe the U.S. resi market will be up 25% YoY in 2019 AND in 2020 vs. consensus view of mid-teens YoY growth after a fresh round of checks this week. Overall, ENPH is ramping capacity at the right time to grow with an accelerating market,” the analyst commented.

As a result, Shen advocates buying the dip in ENPH shares, as reiterates a Buy rating along with $30 price target, which implies shares could soar 65% in the next twelve months.

Like Shen, other Wall Street analysts are impressed with the energy tech company. As ENPH has earned 100% analyst support over the last three months, the word on the Street is that it’s a ‘Strong Buy’. Additionally, its $31.29 average price target indicates about 70% upside potential.

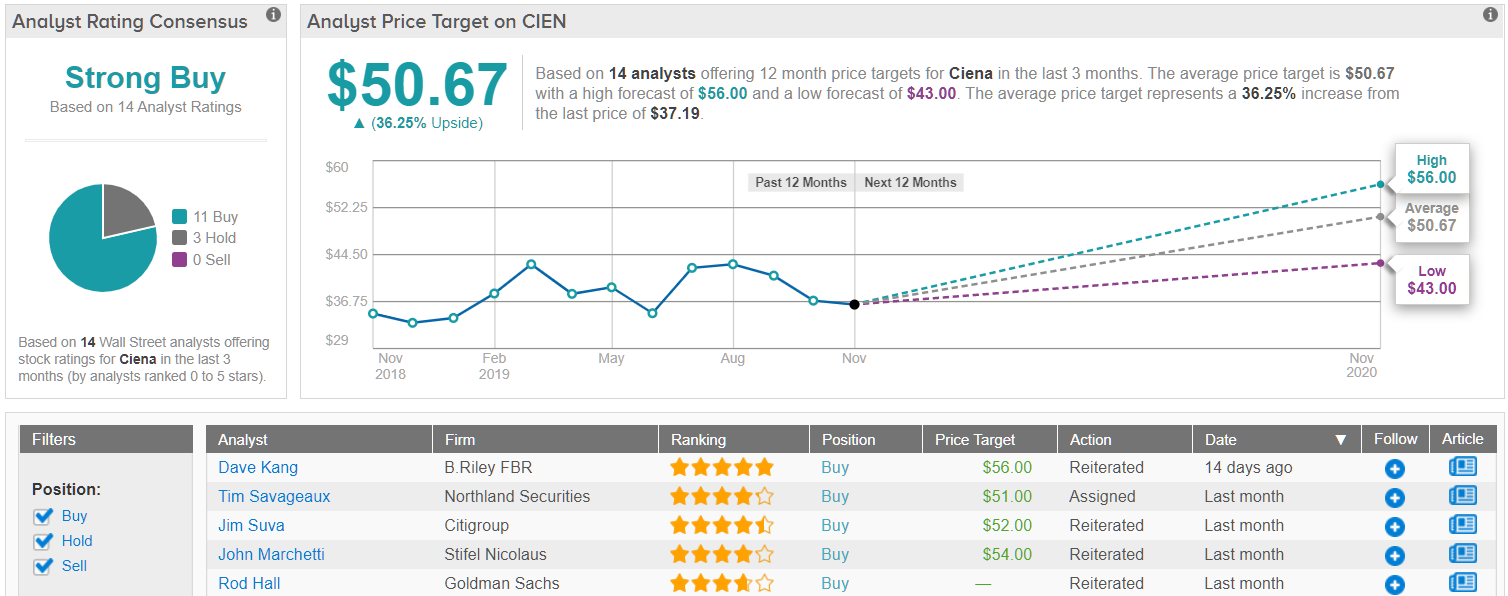

Ciena Corporation (CIEN)

Ciena supplies telecommunications networking equipment and software as well as provides various services. While it’s no question that shares have taken a beating over the last three months, several analysts maintain that big gains are in store.

The company is on track to meet its full-year 2020 revenue and margin guidance thanks to its continued focus on revenue diversification. This diversification has been witnessed not only across geographic regions, but also across customer segments.

On top of this, CIEN has successfully taken market share, becoming one of the top two players in the optical systems space. The other giant in the industry, Huawei, has been crippled given the fact that it’s still on the U.S. Commerce Department’s entry list, preventing the company from accessing the U.S. supply chain.

This lends itself to Cowen & Co. analyst Paul Silverstein’s conclusion that the pullback represents an attractive entry point. “Significant broad-based rev diversification, ongoing share gains and focus on profitability, not just rev growth, is driving far better and more consistent, earnings power and cash flow. Investor expectations have yet to catch-up making for highly attractive risk-reward,” he explained. With this in mind, the five-star analyst remains bullish on CIEN. He even sees upside potential of 47%.

In general, the rest of the Street is also in favor of CIEN. 11 Buy ratings and 3 Holds assigned in the last three months add up to a ‘Strong Buy’ analyst consensus. At an average price target of $50.67, the potential twelve month gain comes in at 36%.

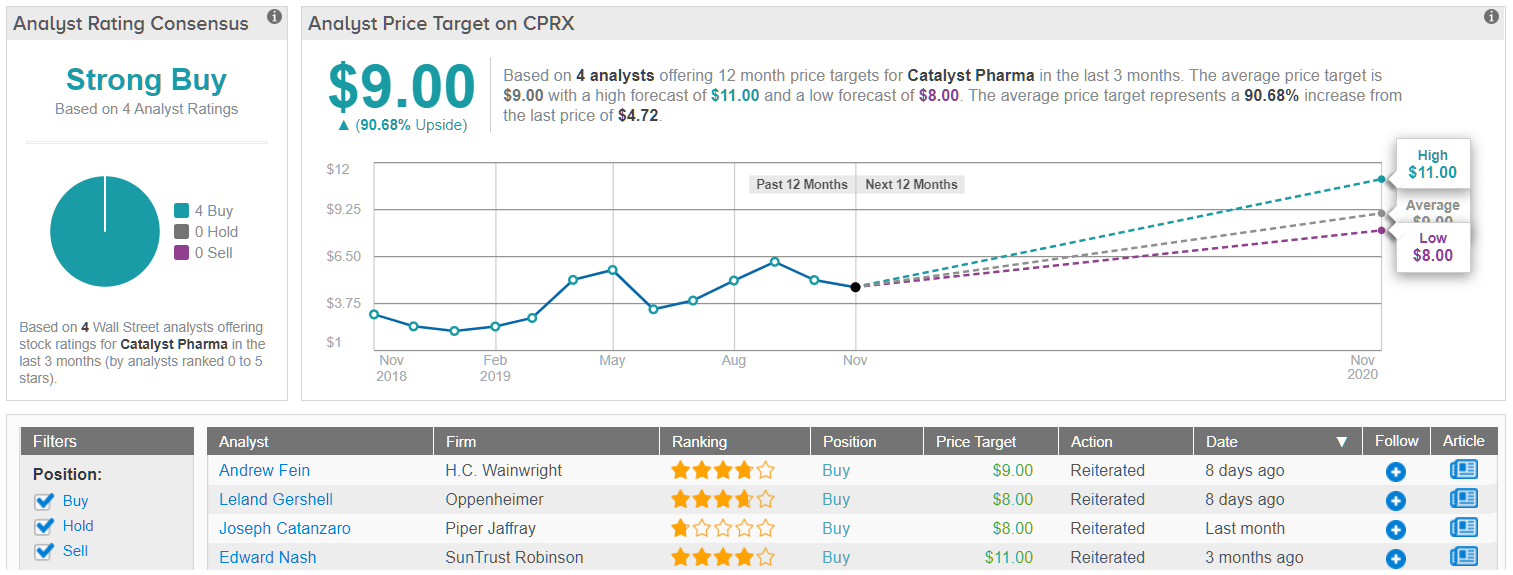

Catalyst Pharmaceuticals (CPRX)

Catalyst is a biopharma name that develops treatments for people affected by neuromuscular and neurological diseases including Lambert-Eaton myasthenic syndrome (LEMS), MuSK antibody positive myasthenia gravis (MuSK-MG), congenital myasthenic syndromes (CMS) and spinal muscular atrophy (SMA) Type 3.

Analysts remind investors to look past recent weakness as its Firdapse drug, its FDA-approved therapy for LEMS in adults, still has the potential to heal share prices. Share prices are hurting partly as a result of unfavorable clinical data.

On October 30, CPRX broke the news that Firdapse fell short of its primary endpoints during the Phase 3 CMS-001 study evaluating its ability to treat CMS, a group of conditions known for causing muscle weakness. Even though shares fell 13% in reaction to the findings, SunTrust Robinson analyst Edward Nash points out that this result was somewhat expected. “We are not surprised by the results give more than 50 subtypes of CMS with only 16 pts randomized in the study,” he commented.

The four-star analyst adds that the drug is likely to demonstrate improved performance in treating MuSK-MG, which is set to see study enrollment completion by the end of the year. This would make top line data available in the first half of 2020, possibly driving big gains for CPRX.

With Nash noting that the FDA could take a favorable stance on CPRX due to the difficult nature of the patient population, it’s no wonder he reiterated his bullish recommendation and $11 price target. This target conveys his confidence in CPRX’s ability to climb 135% higher over the next twelve months.

As 4 Buy ratings have been issued in the previous three months compared to no Holds or Sells, CPRX is a ‘Strong Buy’. In addition, the biopharma’s $9 average price target brings the upside potential to 91%.