On July 29, Canadian cannabis producer Aphria (NASDAQ: APHA) released its fourth-quarter results. Unfortunately, they didn't impress investors. Although the company was happy with its performance, the same can't be said for Wall Street, as the stock's been falling since the release of the results. On earnings day alone, the stock fell by a mammoth 19%.

The quarterly performance wasn't abysmal -- Aphria continued to show progress and increase its sales. But there were some troubling numbers that likely didn't sit well with shareholders. Here are three likely reasons the results weren't what investors were hoping for.

1. Aphria's sales growth was underwhelming

In Q4, Aphria's total net revenue came in at 152.2 million Canadian dollars. That was an 18% improvement from the prior-year period, during which the cannabis producer brought in CA$128.6 million. However, it was only a 5% improvement from the third quarter, in which net revenue totaled CA$144.4 million.

It's a bit disappointing, especially given that during the pandemic, there's been a spike in marijuana sales in Canada. Monthly adult-use sales were hovering at about CA$150 million before the pandemic hit, during Aphria's fiscal third quarter. In the months that followed, monthly sales have been about CA$180 million, which is about a 20% improvement.

The company's cannabis sales of CA$65.5 million in Q4 were only slightly above the CA$64.4 million it recorded in Q3. This suggests that the company is losing market share, because its revenue is not rising in tandem with a surge in cannabis sales in the country.

2. It incurred impairment losses, like many of its peers

One thing that's likely irked investors in recent earnings results is that cannabis companies tend to incur impairment charges, weighing down their results. In May, Aphria's rival Canopy Growth released its fourth-quarter results, which included impairment and restructuring expenses of CA$843 million.

In February, Aurora Cannabis announced that it had incurred writedowns totaling CA$1 billion. HEXO incurred a more modest CA$250 million impairment in its second-quarter results, which the company released in March.

Aphria recorded an even smaller impairment charge of CA$64 million in Q4. It was the company's only blemish during the fiscal year, but it's a 10% increase from the CA$58 million impairment charges that Aphria incurred in the previous fiscal year.

Although the amount is relatively low compared to some of its rivals, these charges still serve as a reminder to investors that as well as the company's performed, Aphria faces many of the same industry challenges as its peers. One of the reasons investors gravitate toward Aphria is that it's generally seen as a safer (and better) buy than other cannabis companies. But an impairment charge of its own has put the stock back into a more negative light.

3. It recorded a steep loss compared with last year

Perhaps most disappointing was that Aphria incurred a loss of CA$84.6 million for the full fiscal year. Even if you factor out the impairment loss, the company would've still reported a net loss of about CA$20.7 million. Either way, that's higher than the CA$16.5 million loss Aphria incurred in the previous fiscal year (which also included impairment charges).

Although the company touted Q4 as the fifth straight quarter in which it recorded positive adjusted earnings before interest, taxes, depreciation, and amortization (EBITDA), the negative stock performance could indicate that investors are looking for more than that. The adjusted EBITDA results were 49% higher than the previous quarter's -- the kind of growth that would normally garner a much more positive response from investors.

Should you buy Aphria stock?

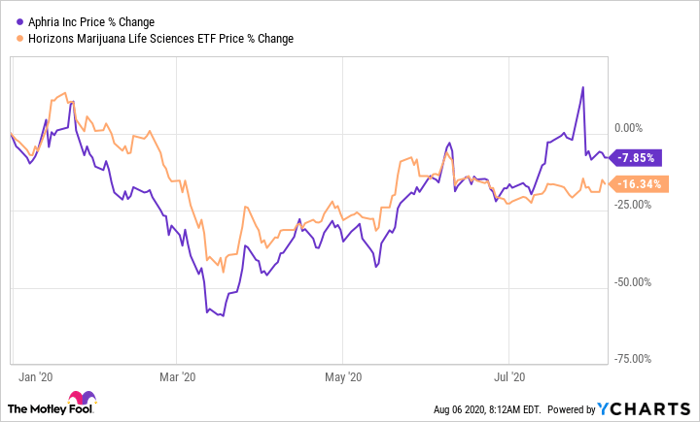

Aphria's stock was in positive territory this year prior to the recent sell-off:

The good news is that it's still doing better than the benchmark Horizons Marijuana Life Sciences ETF (OTC: HMLSF).

With Aphria's share price down as a result of its most recent quarterly results, now may be a great time for investors to buy the stock on the dip. Investors need to remember that this was just one quarter and the cannabis company still grew and posted positive (adjusted) earnings, indicating that it remains on the right track.

Although the quarter was a disappointment in some respects, that shouldn't affect investors' outlook on the company over the long term. Aphria's still a better buy than its peers, and these results don't change that.